Pitch Perfect – or Financial Own Goal?

On the eve of the biggest-ever football World Cup, we look at the parallels between the world’s most popular sport and investing. We also explore the thorny issue of football sponsorship and the further expansion of sports betting markets in the Middle East.

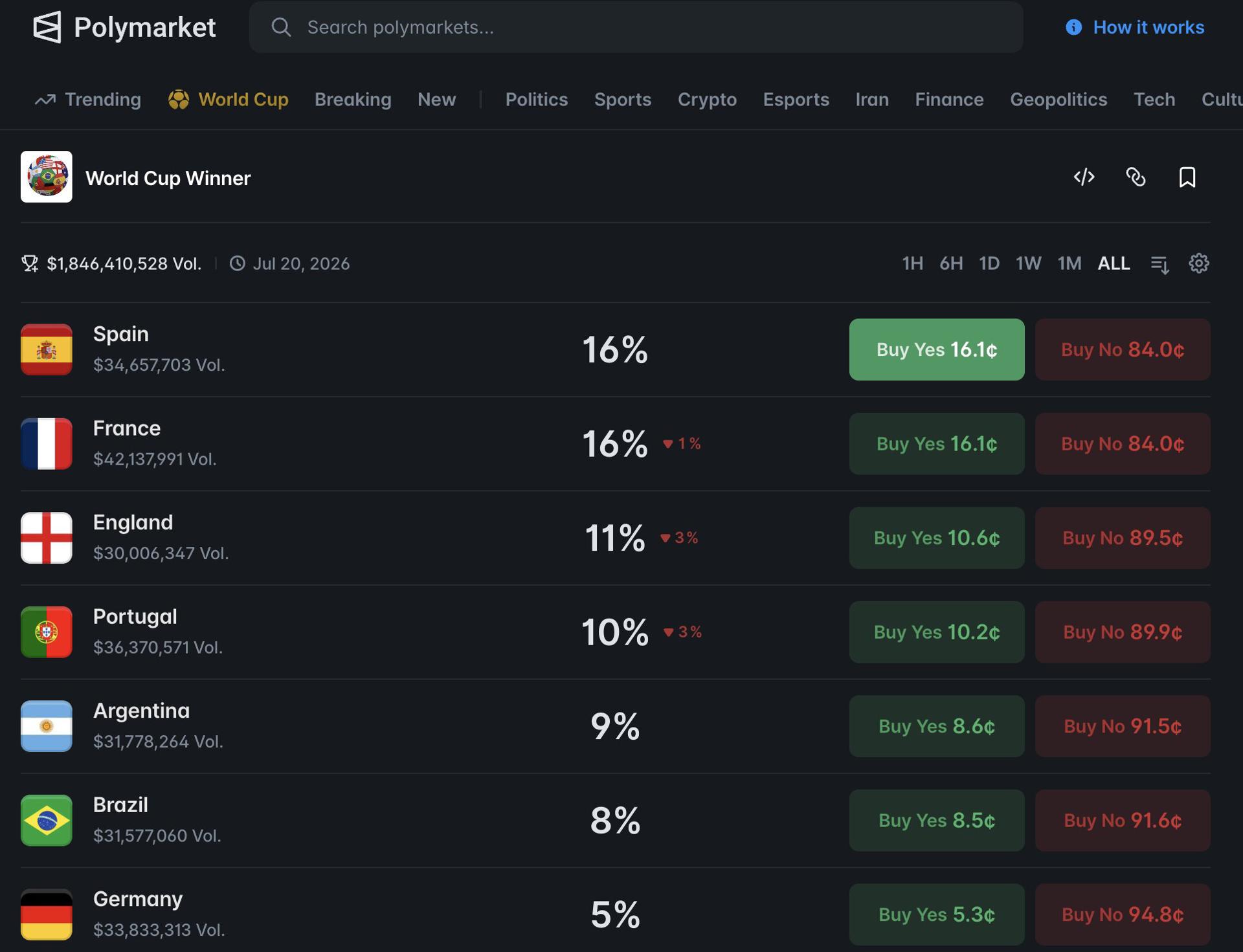

There are many reasons why this year’s World Cup will feature more countries than ever before, ranging from Trump’s desire to host the biggest-ever tournament to Gianni Infantino’s determination to strengthen his power base, fuelled by an equally voluminous ego.

From 13 teams in 1930 to 48 in 2026, impartial observers looking for an eye-catching jersey or funky anthem to latch onto for the next six weeks will be spoilt for choice.

But how does this relate to capital markets? Well, in the same way that a bigger pool of participants would, in theory, suggest a greater chance of a lesser nation lifting the trophy, but in practice, just means it will take longer for the usual suspects to come out on top, so access to a wider range of equities doesn’t make it more likely that an under-represented asset will surprise us all.

There are also flaws in the process by which teams qualify for the tournament in the same way that emerging economies are ranked by global markets.

World Cup qualification is designed to maximise the opportunity for the strongest nations to qualify by either keeping them apart in groups or increasing the number of qualifiers to the point where even a fallen footballing superpower can make it through (fans of the Azzurri, please look away now).

Similarly, less economically developed nations face additional hurdles in gaining access to international investors, with corporate credit quality yet to translate into valuations.

The ‘past performance is no guarantee of future results’ warning can also be applied. For example, Italy played in every World Cup between 1958 and 2014, winning two titles to add to the two it won in the 1930s - but its failure to qualify this time was its third failure in a row.

In market terms, listed companies in emerging economies with strong governance can represent a better investment than an established enterprise in a developed market. As one manager put it, it can take a long time for the true value of a formerly dominant business whose previous advantages are being undermined to become evident.

- How to Spot a Dividend Cut Before It Happens

- Prediction Markets Have a Young Men Problem

- Europe Looks Weak, but Is the Market Saying Otherwise?

Regulator Gets Shirty Over Sponsorship Deals

Last week, the FCA reported that a number of unauthorised firms - including crypto businesses and trading platforms - are using sponsorship to target unwitting football fans.

According to the regulator, these unauthorised firms may be breaching UK financial services laws by providing financial services without authorisation. It has been written directly to football clubs, mainly in the Premier League, to warn them about their relationships with these firms and remind them of their responsibilities to fans.

The FCA says it expects every UK football club to conduct proper due diligence on financial services sponsors before signing agreements and on an ongoing basis.

The reason why crypto companies have become so attractive to clubs in England is that the Premier League has imposed a ban on gambling companies as front-of-shirt sponsors from the start of next season.

Read more: Football Sponsorship Shake-Up: CFDs Brokers Could Score as Betting Brands Get Benched

But while this means Premier League teams will no longer wear betting logos on the front of their match kits, gambling companies are still permitted to sponsor shirt sleeves and appear on stadium advertising hoardings. In addition, the ban only applies to the Premier League - the English Football League has not banned front-of-shirt betting sponsors for its 72 clubs.

One commentator described the FCA’s move as a reminder that the regulatory risk of a crypto project increasingly extends beyond the project itself and that marketing partners, influencers, affiliates, event organisers and now sports clubs are all finding themselves within the compliance conversation.

They go on to draw a parallel with ESMA’s position on reverse solicitation under MiCA, whereby sponsorships are no longer viewed as purely marketing activities, as regulators increasingly see them as evidence of active client acquisition.

Shifting the Gaming Goalposts

On the subject of gambling, it emerged last week that a sports wagering and gaming platform was enabling customers over the age of 21 in the UAE to place bets on World Cup matches through a locally licensed operator for the first time.

Play971 was among a number of online gaming websites licensed by the General Commercial Gaming Regulatory Authority last December and represents a significant development in the country’s emerging regulated gaming sector.

There is considerable unmet demand for betting on sports events in the Middle East. A report from Cognitive Market Research suggests that although the region accounts for less than one per cent of global gambling revenues, the GCC market will expand by an average of 4.5% annually to 2031.

Read more: Prediction Markets Force Sportsbooks to Rethink Their World Cup Strategy

In a recent article on the legal implications of prediction markets in the UAE, global law firm Norton Rose Fulbright notes that the line between gambling and financial products is critically important because gambling is strictly prohibited under Islamic Sharia law due to the element of excessive uncertainty that causes one party to benefit from the other’s loss.

Gambling is also a punishable criminal offence under the current version of the UAE’s penal code, which defines gambling as ‘a game whereby each of the parties thereto agrees - in case of losing - to pay to the winner a certain sum of money or any other thing agreed upon’.

In light of the complex legal matrix that may apply to event contracts, it is, therefore, important to assess whether event contracts are a form of gambling or a qualified financial contract which falls outside the scope of the UAE gambling prohibitions.

According to the firm, the UAE’s matrix of gambling-related laws makes this assessment significantly more complicated than in other jurisdictions, and event contracts straddle the line between requiring a financial services licence and a gambling licence.