UBS, Citigroup, Barclays, Deutsche Bank, RBS, Société Générale, JPMorgan and RP Martin named in settlement with European Commission in rigging case about Yen and Euro Interest Rate Derivatives, enforced under anti-cartel rules.

In response to policing institutions in its jurisdiction within the European Economic Area (EEA), The European Commission has fined 8 international financial institutions a total of € 1,712,468,000 for participating in illegal cartels in markets for financial derivatives, according to an official press release today announced on the European Commission website, and as part of ongoing investigations that have reached a settlement.

The Eight Institutions Referenced Include (in no particular order):

UBS

Citigroup

Barclays,

Deutsche Bank

RBS

Société Générale

JPMorgan

RP Martin

Four of these institutions participated in a cartel relating to interest rate derivatives denominated in the euro currency, as per the press release. Six of them participated in one or more bilateral cartels relating to interest rate derivatives denominated in Japanese yen, and such collusion between competitors, in both cases, is prohibited by Article 101 of the Treaty on the Functioning of the European Union (TFEU) and Article 53 of the EEA Agreement, according to the announcement concerning the massive penalties.

The announcement further details that both decisions were adopted under the Commission's cartel settlement procedure and the companies' fines were reduced by 10% for agreeing to settle (See also MEMO/13/1090, from the European Commission).

Joaquín Almunia,Vice-President, European Commission, [Credit: European Union]

Commenting in the official press release, Joaquín Almunia, the Commission's Vice-President in charge of competition policy, said, “What is shocking about the LIBOR and EURIBOR scandals is not only the manipulation of benchmarks, which is being tackled by financial regulators worldwide, but also the collusion between banks who are supposed to be competing with each other. Today's decision sends a clear message that the Commission is determined to fight and sanction these cartels in the financial sector. Healthy competition and transparency are crucial for financial markets to work properly, at the service of the real economy rather than the interests of a few."

Interest rate derivatives, which include forward rate agreements, swaps, futures, options and other such instruments are financial products that are used by banks or companies for managing the risk of interest rate fluctuations and play a key role in the global economy, the European Union announcement explained today.

Benchmarks such as the EURIBOR or LIBOR reflect an average of the quotes submitted daily by a number of banks which are members of a panel (panel banks). These benchmarks are meant to reflect the cost of inter bank lending in a given currency, and serve as a basis for various financial derivatives.

As investment banks compete with each other in the trading of these derivatives, the levels of these benchmark rates may affect either the cash flows that a bank receives from a counter party, or the cash flow it needs to pay to the counter party under interest rate derivatives contracts. However, the potential conflict of interest exists as parties to the trade can collude to their benefit, via submitted daily fixing rates or other means resulting in unfair market participation or rate manipulation (whether be price rates or interest rates).

These products derive their value from the level of a benchmark interest rate, such as the London inter bank offered rate (LIBOR) – which is used for various currencies including the Japanese yen (JPY) - or the Euro Inter bank Offered Rate (EURIBOR), for the euro.

The Cartel in Euro Interest Rate Derivatives (EIRD)

The EIRD cartel operated between September 2005 and May 2008. The settling parties are Barclays, Deutsche Bank, RBS and Société Générale. The cartel aimed at distorting the normal course of pricing components for these derivatives. Traders of different banks discussed their bank's submissions for the calculation of the EURIBOR, as well as their trading and pricing strategies.

The Commission's investigation started with unannounced inspections in October 2011 (see MEMO/11/711). The Commission opened proceedings in March 2013. Barclays was not fined as it benefited from immunity under the Commission's 2006 Leniency Notice for revealing the existence of the cartel to the Commission. Deutsche Bank, RBS and Société Générale received a reduction of their fines for their cooperation in the investigation under the Commission's leniency program. These companies received a further fine reduction of 10% for agreeing to settle the case with the Commission.

In the context of the same investigation, proceedings were opened against Crédit Agricole, HSBC and JPMorgan, and the investigation will continue under the standard (non-settlement) cartel procedure.

The Cartels in Yen Interest Rate Derivatives (YIRD)

In the YIRD sector, the Commission uncovered 7 distinct bilateral infringements lasting between 1 and 10 months in the period from 2007 to 2010. The collusion included discussions between traders of the participating banks on certain JPY LIBOR submissions. The traders involved also exchanged, on occasions, commercially sensitive information relating either to trading positions or to future JPY LIBOR submissions (and in one of the infringements relating to certain future submissions for the Euroyen TIBOR – Tokyo inter bank offered rate). The banks involved in one or more of the infringements are UBS, RBS, Deutsche Bank, Citigroup and JPMorgan. The broker RP Martin facilitated one of the infringements by using its contacts with a number of JPY LIBOR panel banks that did not participate in the infringement, with the aim of influencing their JPY LIBOR submissions.

The Commission opened proceedings in February 2013. UBS received full immunity under the Commission's 2006 Leniency Notice for revealing to the Commission the existence of the infringements. Citigroup also benefited from full immunity for its participation in one bilateral infringement. For their cooperation with the investigation, the Commission granted fine reductions to Citigroup, Deutsche Bank, RBS and RP Martin, under the Commission's leniency program. The companies have also been granted a fine reduction of 10% for agreeing to settle the case with the Commission.

In the context of the same investigation, the Commission has also opened proceedings against the cash broker ICAP. This investigation continues under the standard (non-settlement) cartel procedure.

The Fines, UBS and Barclays get Full Immunity, Citigroup Partial Immunity

The fines were set on the basis of the Commission's 2006 Guidelines on fines (see IP/06/857 and MEMO/06/256).

In setting the level of fines, the Commission took into account the banks' value of sales for the products concerned within the EEA, the very serious nature of the infringements, their geographic scope and respective duration.

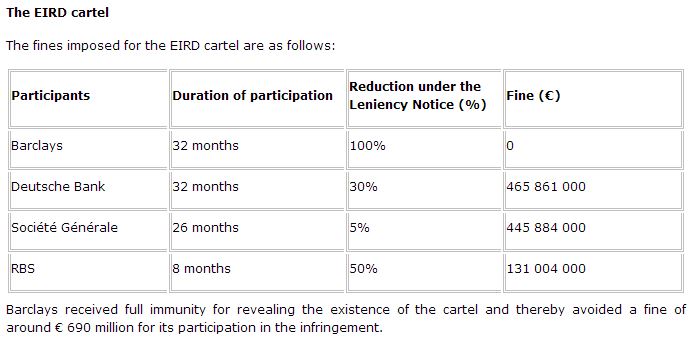

Excerpt of the EIRD Cartel Imposed Fines:

As shown above, Barclays received full immunity for revealing the existence of the cartel and thereby avoided a fine of around € 690 million for its participation in the infringement.

Excerpt of the YIRD Cartel Imposed Fines:

UBS, RBS, Deutsche Bank, JPMorgan, Citigroup and RP Martin were involved in one or several of the infringements of EU competition rules.

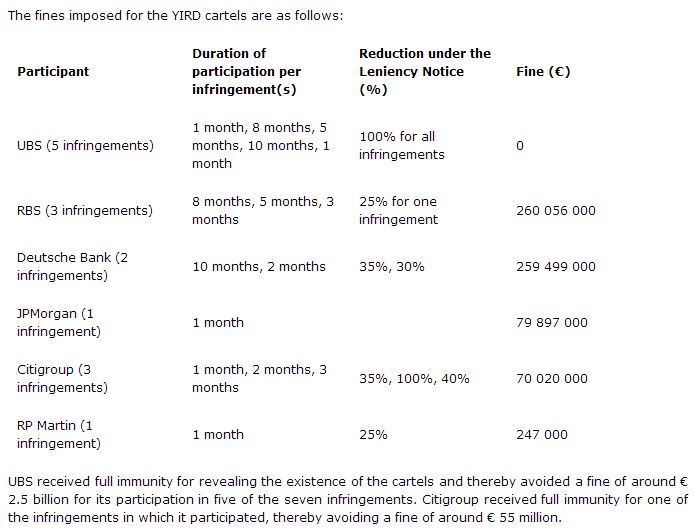

The fines imposed for the YIRD cartels can be seen in the excerpt below from the press release:

As shown in the bottom of the above excerpt, UBS received full immunity for revealing the existence of the cartels, and thereby avoided a fine of around € 2.5 billion for its participation in five of the seven infringements. Clearly, an effective cost-saving strategy as part of its cooperation on its own infringements in the investigation and that of others, thanks to the benefits afforded on the current legislations.

This immunity is like a hybrid cross between whistle-blowers blowing the whistle on themselves and plea-bargaining in response to a lessened degree of reprimanding, or in this case full immunity. On a lesser note, monetarily speaking, Citigroup received full immunity for one of the infringements in which it participated, thereby avoiding a fine of around € 55 million.

Derivatives and Benchmark Price Manipulations Under Review

Also described in the official European Commissions' press release today, was the most common basic interest rate derivatives including forward rate agreements, interest rate swaps, interest rate options, and interest rate futures. In addition, as interest rate derivatives may be traded over the counter (OTC) or, in the case of interest rate futures, exchange traded. Just like any synthetically priced derivative, they derive their value from a underlying benchmark -in this case interest rates.

The products handled by the EIRD cartel are Euro interest rate derivatives linked to the EURIBOR and/or the Euro Over-Night Index Average (EONIA). The products handled by the cartels are the Japanese yen interest rate derivatives linked to the JPY LIBOR (and in the case of one infringement also Euroyen TIBOR).

The EURIBOR, JPY LIBOR and Euroyen TIBOR are benchmark interest rates intended to reflect the cost of inter bank lending in euros or Japanese yen respectively. These benchmarks are widely used in the international money markets and they are based on the relevant panel banks' individual quotes submitted daily to the relevant calculation agent.

On 18 September, 2013, the Commission proposed a Regulation on indices used as benchmarks in financial instruments and financial contracts such as LIBOR or EURIBOR. See IP/13/841. The planned measures aim at helping restore confidence in the integrity of benchmarks following the LIBOR and EURIBOR scandals.

New Anti-Cartel Enforcement, a First in the Financial Sector

These are the first two decisions concerning cartels in the financial sector since the start of the financial crisis in 2008. Anti-cartel enforcement is a top priority for the Commission especially in the financial sector. The decisions adopted in the EIRD and YIRD cartels indicate the kinds of behavior banks should avoid if they wish to comply with EU competition rules.

Today's decisions are the eighth and ninth settlement decisions since the introduction of the settlement procedure for cartels in June 2008 (see IP/08/1056 and MEMO/08/458). They are one of the swiftest cartel settlements decided upon by the Commission, showing the full potential of the efficiencies offered by the settlement procedure.

Under a cartel settlement, companies that have participated in a cartel acknowledge their participation in the infringement and their liability for it. The cartel settlement procedure is based on the Antitrust Regulation 1/2003 and allows the Commission to apply a simplified procedure and thereby reduce the length of the investigation. This is good for consumers and for taxpayers as it reduces costs; good for antitrust enforcement as it frees up resources to tackle other suspected cases; and good for the companies themselves that benefit from quicker decisions and a 10% reduction in fines.

In a previous statement following the Competitiveness Council of 2 December, 2013, Joaquín Almunia,Vice-President of the European Commission, stated the following with regards to upcoming finalization of related legislative drafts:

Joaquín Almunia,Vice-President, European Commission

"I welcome the adoption by the Council of a general approach on the proposal for a Directive on Antitrust Damages Actions. This is a crucial step in the process. I now look forward to the European Parliament concluding its work in committees in January, so that the two legislative institutions can agree on the final text by the end of the legislature. The timely adoption of this legislative proposal is essential so that victims of infringements of the EU antitrust rules can obtain redress for the harm they suffered. The obstacles to effective compensation that they face today must be removed."

In response to policing institutions in its jurisdiction within the European Economic Area (EEA), The European Commission has fined 8 international financial institutions a total of € 1,712,468,000 for participating in illegal cartels in markets for financial derivatives, according to an official press release today announced on the European Commission website, and as part of ongoing investigations that have reached a settlement.

The Eight Institutions Referenced Include (in no particular order):

UBS

Citigroup

Barclays,

Deutsche Bank

RBS

Société Générale

JPMorgan

RP Martin

Four of these institutions participated in a cartel relating to interest rate derivatives denominated in the euro currency, as per the press release. Six of them participated in one or more bilateral cartels relating to interest rate derivatives denominated in Japanese yen, and such collusion between competitors, in both cases, is prohibited by Article 101 of the Treaty on the Functioning of the European Union (TFEU) and Article 53 of the EEA Agreement, according to the announcement concerning the massive penalties.

The announcement further details that both decisions were adopted under the Commission's cartel settlement procedure and the companies' fines were reduced by 10% for agreeing to settle (See also MEMO/13/1090, from the European Commission).

Joaquín Almunia,Vice-President, European Commission, [Credit: European Union]

Commenting in the official press release, Joaquín Almunia, the Commission's Vice-President in charge of competition policy, said, “What is shocking about the LIBOR and EURIBOR scandals is not only the manipulation of benchmarks, which is being tackled by financial regulators worldwide, but also the collusion between banks who are supposed to be competing with each other. Today's decision sends a clear message that the Commission is determined to fight and sanction these cartels in the financial sector. Healthy competition and transparency are crucial for financial markets to work properly, at the service of the real economy rather than the interests of a few."

Interest rate derivatives, which include forward rate agreements, swaps, futures, options and other such instruments are financial products that are used by banks or companies for managing the risk of interest rate fluctuations and play a key role in the global economy, the European Union announcement explained today.

Benchmarks such as the EURIBOR or LIBOR reflect an average of the quotes submitted daily by a number of banks which are members of a panel (panel banks). These benchmarks are meant to reflect the cost of inter bank lending in a given currency, and serve as a basis for various financial derivatives.

As investment banks compete with each other in the trading of these derivatives, the levels of these benchmark rates may affect either the cash flows that a bank receives from a counter party, or the cash flow it needs to pay to the counter party under interest rate derivatives contracts. However, the potential conflict of interest exists as parties to the trade can collude to their benefit, via submitted daily fixing rates or other means resulting in unfair market participation or rate manipulation (whether be price rates or interest rates).

These products derive their value from the level of a benchmark interest rate, such as the London inter bank offered rate (LIBOR) – which is used for various currencies including the Japanese yen (JPY) - or the Euro Inter bank Offered Rate (EURIBOR), for the euro.

The Cartel in Euro Interest Rate Derivatives (EIRD)

The EIRD cartel operated between September 2005 and May 2008. The settling parties are Barclays, Deutsche Bank, RBS and Société Générale. The cartel aimed at distorting the normal course of pricing components for these derivatives. Traders of different banks discussed their bank's submissions for the calculation of the EURIBOR, as well as their trading and pricing strategies.

The Commission's investigation started with unannounced inspections in October 2011 (see MEMO/11/711). The Commission opened proceedings in March 2013. Barclays was not fined as it benefited from immunity under the Commission's 2006 Leniency Notice for revealing the existence of the cartel to the Commission. Deutsche Bank, RBS and Société Générale received a reduction of their fines for their cooperation in the investigation under the Commission's leniency program. These companies received a further fine reduction of 10% for agreeing to settle the case with the Commission.

In the context of the same investigation, proceedings were opened against Crédit Agricole, HSBC and JPMorgan, and the investigation will continue under the standard (non-settlement) cartel procedure.

The Cartels in Yen Interest Rate Derivatives (YIRD)

In the YIRD sector, the Commission uncovered 7 distinct bilateral infringements lasting between 1 and 10 months in the period from 2007 to 2010. The collusion included discussions between traders of the participating banks on certain JPY LIBOR submissions. The traders involved also exchanged, on occasions, commercially sensitive information relating either to trading positions or to future JPY LIBOR submissions (and in one of the infringements relating to certain future submissions for the Euroyen TIBOR – Tokyo inter bank offered rate). The banks involved in one or more of the infringements are UBS, RBS, Deutsche Bank, Citigroup and JPMorgan. The broker RP Martin facilitated one of the infringements by using its contacts with a number of JPY LIBOR panel banks that did not participate in the infringement, with the aim of influencing their JPY LIBOR submissions.

The Commission opened proceedings in February 2013. UBS received full immunity under the Commission's 2006 Leniency Notice for revealing to the Commission the existence of the infringements. Citigroup also benefited from full immunity for its participation in one bilateral infringement. For their cooperation with the investigation, the Commission granted fine reductions to Citigroup, Deutsche Bank, RBS and RP Martin, under the Commission's leniency program. The companies have also been granted a fine reduction of 10% for agreeing to settle the case with the Commission.

In the context of the same investigation, the Commission has also opened proceedings against the cash broker ICAP. This investigation continues under the standard (non-settlement) cartel procedure.

The Fines, UBS and Barclays get Full Immunity, Citigroup Partial Immunity

The fines were set on the basis of the Commission's 2006 Guidelines on fines (see IP/06/857 and MEMO/06/256).

In setting the level of fines, the Commission took into account the banks' value of sales for the products concerned within the EEA, the very serious nature of the infringements, their geographic scope and respective duration.

Excerpt of the EIRD Cartel Imposed Fines:

As shown above, Barclays received full immunity for revealing the existence of the cartel and thereby avoided a fine of around € 690 million for its participation in the infringement.

Excerpt of the YIRD Cartel Imposed Fines:

UBS, RBS, Deutsche Bank, JPMorgan, Citigroup and RP Martin were involved in one or several of the infringements of EU competition rules.

The fines imposed for the YIRD cartels can be seen in the excerpt below from the press release:

As shown in the bottom of the above excerpt, UBS received full immunity for revealing the existence of the cartels, and thereby avoided a fine of around € 2.5 billion for its participation in five of the seven infringements. Clearly, an effective cost-saving strategy as part of its cooperation on its own infringements in the investigation and that of others, thanks to the benefits afforded on the current legislations.

This immunity is like a hybrid cross between whistle-blowers blowing the whistle on themselves and plea-bargaining in response to a lessened degree of reprimanding, or in this case full immunity. On a lesser note, monetarily speaking, Citigroup received full immunity for one of the infringements in which it participated, thereby avoiding a fine of around € 55 million.

Derivatives and Benchmark Price Manipulations Under Review

Also described in the official European Commissions' press release today, was the most common basic interest rate derivatives including forward rate agreements, interest rate swaps, interest rate options, and interest rate futures. In addition, as interest rate derivatives may be traded over the counter (OTC) or, in the case of interest rate futures, exchange traded. Just like any synthetically priced derivative, they derive their value from a underlying benchmark -in this case interest rates.

The products handled by the EIRD cartel are Euro interest rate derivatives linked to the EURIBOR and/or the Euro Over-Night Index Average (EONIA). The products handled by the cartels are the Japanese yen interest rate derivatives linked to the JPY LIBOR (and in the case of one infringement also Euroyen TIBOR).

The EURIBOR, JPY LIBOR and Euroyen TIBOR are benchmark interest rates intended to reflect the cost of inter bank lending in euros or Japanese yen respectively. These benchmarks are widely used in the international money markets and they are based on the relevant panel banks' individual quotes submitted daily to the relevant calculation agent.

On 18 September, 2013, the Commission proposed a Regulation on indices used as benchmarks in financial instruments and financial contracts such as LIBOR or EURIBOR. See IP/13/841. The planned measures aim at helping restore confidence in the integrity of benchmarks following the LIBOR and EURIBOR scandals.

New Anti-Cartel Enforcement, a First in the Financial Sector

These are the first two decisions concerning cartels in the financial sector since the start of the financial crisis in 2008. Anti-cartel enforcement is a top priority for the Commission especially in the financial sector. The decisions adopted in the EIRD and YIRD cartels indicate the kinds of behavior banks should avoid if they wish to comply with EU competition rules.

Today's decisions are the eighth and ninth settlement decisions since the introduction of the settlement procedure for cartels in June 2008 (see IP/08/1056 and MEMO/08/458). They are one of the swiftest cartel settlements decided upon by the Commission, showing the full potential of the efficiencies offered by the settlement procedure.

Under a cartel settlement, companies that have participated in a cartel acknowledge their participation in the infringement and their liability for it. The cartel settlement procedure is based on the Antitrust Regulation 1/2003 and allows the Commission to apply a simplified procedure and thereby reduce the length of the investigation. This is good for consumers and for taxpayers as it reduces costs; good for antitrust enforcement as it frees up resources to tackle other suspected cases; and good for the companies themselves that benefit from quicker decisions and a 10% reduction in fines.

In a previous statement following the Competitiveness Council of 2 December, 2013, Joaquín Almunia,Vice-President of the European Commission, stated the following with regards to upcoming finalization of related legislative drafts:

Joaquín Almunia,Vice-President, European Commission

"I welcome the adoption by the Council of a general approach on the proposal for a Directive on Antitrust Damages Actions. This is a crucial step in the process. I now look forward to the European Parliament concluding its work in committees in January, so that the two legislative institutions can agree on the final text by the end of the legislature. The timely adoption of this legislative proposal is essential so that victims of infringements of the EU antitrust rules can obtain redress for the harm they suffered. The obstacles to effective compensation that they face today must be removed."

Hirose Financial UK Costs Rise 40% as Revenue Growth Slows to 18% After Retail Exit

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

![Joaquín Almunia,Vice-President, European Commission, [Credit: European Union]](https://www.financemagnates.com/wp-content/uploads/fxmag/2013/12/Joaquin-Alumina_.jpg)