Paul Golden highlights Fundstrat findings linking government policy to extreme market swings since 1981.

He also dives into populism research showing long-term economic drag despite short-term political disruption benefits.

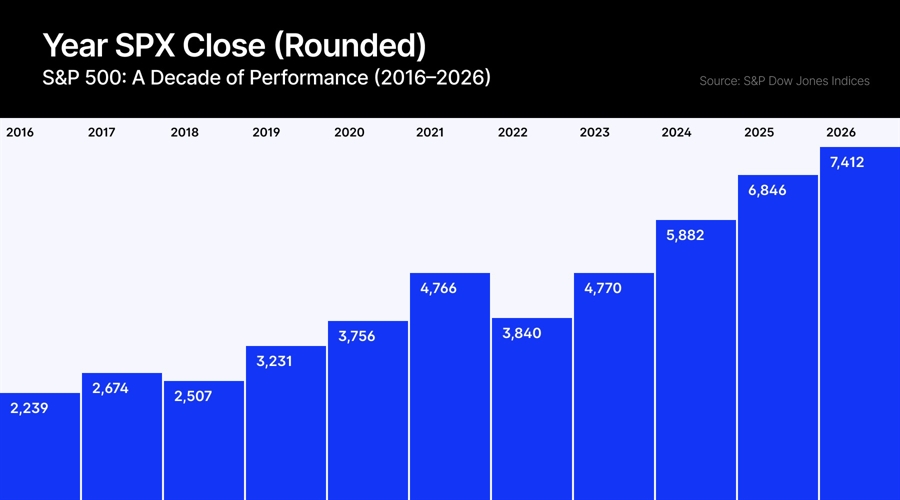

2026 figure reflects YTD performance as of May 13

Donald Trump’s Predecessors on Market Volatility

Market research firms generally fly under the radar until

they produce a piece of work that challenges deeply held beliefs. Fundstrat did

just that recently when macro data scientist Alex Wang analysed the causes of

the five best and worst market days during the last 12 US administrations

dating from Ronald Reagan in 1981.

The chart considers the impact of a range of factors from

corporate earnings and foreign events to economic data and interest rate

expectations. Unsurprisingly, government policy was the most common theme – but

the really interesting finding was how it dominated the peaks and troughs of

one president in particular.

The research indicates that the current presidency was

responsible for the five best and five worst market days since Trump took

office for the second time. According to the analysis, this was not the case for

any other president over the last 45 years.

White House spokesman Kush Desai told MarketWatch that since

president Trump took office, publicly listed companies have reported

blockbuster earnings reports and clocked multiple all-time high stock

valuations because of his pro-growth agenda of tax cuts, deregulation, energy

abundance and fair trade deals.

Hardika Singh, Economic Strategist at Fundstrat, Source: LinkedIn

The best market day was 9 April 2025, when the S&P

500 rose almost 10% after the suspension of the so-called ‘liberation day’

tariffs. However, the unpredictability of Trump’s pronouncements is highlighted

by the fact that one of the worst days came just 24 hours after these tariffs

were announced.

Indeed, all the sharpest stock market falls since January

2025 can be linked to tariff announcements, while the gains have been highly

concentrated.

Hardika Singh, an economic strategist at Fundstrat

suggests that if the five best market days of the current administration were

excluded, the S&P 500 would be down 2.7% since he took office instead of

showing an 18.5% increase.

Perhaps disappointingly for those who believe that

government policy should move markets, the research concluded that the losses

pretty much cancelled out the gains, suggesting that much of the noise that has

emanated from the White House over the last year-and-a-bit has been just that –

noise.

Turmoil at the Top as Starmer Teeters

There’s a saying in football that you become a better

player when you are out of the team – in other words, when those on the pitch are

messing up the alternative can only be better.

To carry on the footballing analogy, the UK Labour party

spent 14 years on the substitutes bench toning down some the messaging that has

traditionally alarmed financial markets in a bid to make it more appealing to

the business community, particularly in financial services.

Sadly for its supporters, since winning promotion to

Downing Street, Keir Starmer has turned into the Ali

Dia

of British politics.

A series of U-turns and poorly considered policies have

shaken confidence in his leadership and he now stands on the brink after poor

local election results prompted dozens of his members of parliament to call for

his departure.

David Morrison, Senior Market Analyst at Trade Nation, Source: LinkedIn

“Domestic political issues undermine sterling as Starmer

desperately attempts to cling on to his position, for some reason,” says

Morrison in a research note dated 12 May.

“Yet despite weakness across the

British pound and euro against the US dollar, both currencies found some

support due to the prospect of higher interest rates.”

Analysts currently expect the Bank of England to hike

rates by around 75 basis points each before the end of the year.

One market analyst suggested that the turmoil at the top

of the UK government would create more uncertainty in financial markets as

analysts consider the potential impact on fiscal policy of a change of prime

minister and perhaps more significantly, chancellor of exchequer.

Politics, Populism and Portfolios

Earlier this year, Capital Group published a paper exploring

the global rise of populism (defined as a political style that frames politics

as a struggle between the ‘people’ and the ‘elites’) and its impact on

financial markets.

The authors note that populism reshapes politics and that

its economic consequences are equally profound. They refer to research across

60 countries showing that after an initial wave of optimism, economic

performance deteriorates with real GDP per capita growth slowing by roughly one

percentage point per year in the first five years of populists taking power and

remaining below trend even after 15 years.

🚨 BREAKING:

🇺🇸🇨🇳 PRESIDENT TRUMP WILL FLY TO CHINA ON WEDNESDAY, MAY 13

SOURCES REPORT THAT TRUMP WILL PUT PRESSURE ON XI JINPING REGARDING THE WAR WITH IRAN

That said, the paper also acknowledges that the

alternative to populist governance is not necessarily inclusive growth. In many

countries, the pre-populist trajectory was already characterised by income

inequality, low productivity, demographic headwinds, political fragmentation

and difficulty delivering meaningful structural reform. Populism often emerges

as a break in this stagnation.

While evidence shows populist policies generally worsen

long-term outcomes, they can disrupt entrenched inertia and create space for

reform coalitions. This helps explain why some electorates view populism as a

corrective to an underperforming status quo despite its economic risks.

For investors, these political and economic dynamics

translate into tangible market risks and opportunities.

Historical trends and

recent market behaviour indicate that populist regimes often disrupt

traditional market dynamics, amplifying volatility and pressuring asset

performance.

While populism typically heightens uncertainty and risk

premia, periods of volatility can also create compelling entry points for long‑term investors, particularly

in markets with strong institutions or credible reform agendas.

Moreover, episodes of financial repression (a common

feature of populist policy frameworks, where interest rates are held below

inflation or directed toward government financing) can temporarily support

equity and realasset valuations by suppressing discount rates and

limiting safer yield alternatives.

Donald Trump’s Predecessors on Market Volatility

Market research firms generally fly under the radar until

they produce a piece of work that challenges deeply held beliefs. Fundstrat did

just that recently when macro data scientist Alex Wang analysed the causes of

the five best and worst market days during the last 12 US administrations

dating from Ronald Reagan in 1981.

The chart considers the impact of a range of factors from

corporate earnings and foreign events to economic data and interest rate

expectations. Unsurprisingly, government policy was the most common theme – but

the really interesting finding was how it dominated the peaks and troughs of

one president in particular.

The research indicates that the current presidency was

responsible for the five best and five worst market days since Trump took

office for the second time. According to the analysis, this was not the case for

any other president over the last 45 years.

White House spokesman Kush Desai told MarketWatch that since

president Trump took office, publicly listed companies have reported

blockbuster earnings reports and clocked multiple all-time high stock

valuations because of his pro-growth agenda of tax cuts, deregulation, energy

abundance and fair trade deals.

Hardika Singh, Economic Strategist at Fundstrat, Source: LinkedIn

The best market day was 9 April 2025, when the S&P

500 rose almost 10% after the suspension of the so-called ‘liberation day’

tariffs. However, the unpredictability of Trump’s pronouncements is highlighted

by the fact that one of the worst days came just 24 hours after these tariffs

were announced.

Indeed, all the sharpest stock market falls since January

2025 can be linked to tariff announcements, while the gains have been highly

concentrated.

Hardika Singh, an economic strategist at Fundstrat

suggests that if the five best market days of the current administration were

excluded, the S&P 500 would be down 2.7% since he took office instead of

showing an 18.5% increase.

Perhaps disappointingly for those who believe that

government policy should move markets, the research concluded that the losses

pretty much cancelled out the gains, suggesting that much of the noise that has

emanated from the White House over the last year-and-a-bit has been just that –

noise.

Turmoil at the Top as Starmer Teeters

There’s a saying in football that you become a better

player when you are out of the team – in other words, when those on the pitch are

messing up the alternative can only be better.

To carry on the footballing analogy, the UK Labour party

spent 14 years on the substitutes bench toning down some the messaging that has

traditionally alarmed financial markets in a bid to make it more appealing to

the business community, particularly in financial services.

Sadly for its supporters, since winning promotion to

Downing Street, Keir Starmer has turned into the Ali

Dia

of British politics.

A series of U-turns and poorly considered policies have

shaken confidence in his leadership and he now stands on the brink after poor

local election results prompted dozens of his members of parliament to call for

his departure.

David Morrison, Senior Market Analyst at Trade Nation, Source: LinkedIn

“Domestic political issues undermine sterling as Starmer

desperately attempts to cling on to his position, for some reason,” says

Morrison in a research note dated 12 May.

“Yet despite weakness across the

British pound and euro against the US dollar, both currencies found some

support due to the prospect of higher interest rates.”

Analysts currently expect the Bank of England to hike

rates by around 75 basis points each before the end of the year.

One market analyst suggested that the turmoil at the top

of the UK government would create more uncertainty in financial markets as

analysts consider the potential impact on fiscal policy of a change of prime

minister and perhaps more significantly, chancellor of exchequer.

Politics, Populism and Portfolios

Earlier this year, Capital Group published a paper exploring

the global rise of populism (defined as a political style that frames politics

as a struggle between the ‘people’ and the ‘elites’) and its impact on

financial markets.

The authors note that populism reshapes politics and that

its economic consequences are equally profound. They refer to research across

60 countries showing that after an initial wave of optimism, economic

performance deteriorates with real GDP per capita growth slowing by roughly one

percentage point per year in the first five years of populists taking power and

remaining below trend even after 15 years.

🚨 BREAKING:

🇺🇸🇨🇳 PRESIDENT TRUMP WILL FLY TO CHINA ON WEDNESDAY, MAY 13

SOURCES REPORT THAT TRUMP WILL PUT PRESSURE ON XI JINPING REGARDING THE WAR WITH IRAN

That said, the paper also acknowledges that the

alternative to populist governance is not necessarily inclusive growth. In many

countries, the pre-populist trajectory was already characterised by income

inequality, low productivity, demographic headwinds, political fragmentation

and difficulty delivering meaningful structural reform. Populism often emerges

as a break in this stagnation.

While evidence shows populist policies generally worsen

long-term outcomes, they can disrupt entrenched inertia and create space for

reform coalitions. This helps explain why some electorates view populism as a

corrective to an underperforming status quo despite its economic risks.

For investors, these political and economic dynamics

translate into tangible market risks and opportunities.

Historical trends and

recent market behaviour indicate that populist regimes often disrupt

traditional market dynamics, amplifying volatility and pressuring asset

performance.

While populism typically heightens uncertainty and risk

premia, periods of volatility can also create compelling entry points for long‑term investors, particularly

in markets with strong institutions or credible reform agendas.

Moreover, episodes of financial repression (a common

feature of populist policy frameworks, where interest rates are held below

inflation or directed toward government financing) can temporarily support

equity and realasset valuations by suppressing discount rates and

limiting safer yield alternatives.

Paul Golden is an experienced freelance financial journalist with a strong institutional background. Over the past two decades, he has written for globally recognised financial publications, covering topics such as market structure, regulation, trading behaviour, and economic policy.

Eightcap and TTTMarkets Executives Question Prop Consistency Rules Their Firms Use

Featured Videos

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.