However, throughout the 2000s, there was a different beast being developed. On August 18, 2008, Bitcoin.org was registered as a domain name. By October of the same year, a document entitled "Bitcoin: A Peer to Peer Electronic System" was published by an entity using the name ‘Satoshi Nakamoto.’ The network then came into being a reality on the January 3, 2009, when Satoshi Nakamoto mined the "genesis block" which was rewarded at 50 bitcoin.

Who is Satoshi Nakamoto?

The identity of the enigmatic Satoshi Nakamoto has long been a mystery in crypto circles and has caused much debate.

The name is obviously a pseudonym, but no one seems to quite know who the person behind the figure is. For example, Craig Steven Wright has come out and stated that he is the inventor of the currency, but there is quite a bit of skepticism about that claim. Wright is an Australian computer scientist and entrepreneur who has shown a keen interest and history of developing cryptocurrencies. Nick Szabo and Dorian Nakamoto have also been named as potential creators of the currency.

While the true identity of Satoshi is unknown, the most likely theory seems to be that that the currency was created by more than one individual and was the work of a team of people.

Bitcoin's network runs on a Proof-of-Work algorithm. This algorithm is the means by which new Bitcoins are produced, and transactions are confirmed, a process known as mining.

The blockchain is virtually impervious to cyber attacks that often affect centralized entities: denial of service, as well as spam and other potentially malicious attacks. It is also incredibly difficult to falsify transactions on the Bitcoin network.

A user needs to be able to understand what a hash function is in this context, given its complexity. In essence, this function makes it so any kind of data can be mapped in any amount for a specific type of reason. If secured properly, this function cannot be differentiated from a random function in a given situation.

how to get funding:

keep saying blockchain really fast until people in suits get confused and throw you money

— I Am Devloper (@iamdevloper) January 24, 2018

In Proof of Work, the individual who is chosen to confirm a transaction is usually the individual with the most "hash power" (computing power.) They use their hash power to solve complex equations; once an answer is discovered, a 'block' (a small group) of transactions are confirmed. This typically happens at a rate of 3-4 transactions per second. In return for their work, miners are given rewards in the form of BTC tokens.

If this is done properly, and the correct cryptographical aspects are applied, then the solution should only be found by applying the "brute force" method, which entails looking to try every single possible combination until the correct answer is found.

This system has been effective until the present time, but one must also note that it does consume a vast quantity of energy. To illustrate this point, the vast majority of countries in Africa use up less energy than the network for mining Bitcoin.

An alternative to Proof of Work, the Proof of Stake algorithm, limits the amount of currency one can utilize in the space of given time. This system is not used by Bitcoin, but is used for coins such as Blackcoin; This system allows an individual to bypass problems such as the vast energy consumption which comes with Proof-of-Work, and to create a greener and energy efficient method to mine Bitcoin. However, this algorithm is not quite as popular as Proof of Work.

Problems with the Bitcoin Network

The Bitcoin Network, despite its numerous strengths, has some issues which need addressing about how the currency should work. The two primary problems associated with Bitcoin’s high fees and scalability.

The Bitcoin network has seen an increased number of transactions in the past few years, which has caused the network to come under strain. In other words, there are simply too many transactions for the networks to process in a reasonable amount of time. On a practical level, this means that transactions can take hours to complete and be extremely expensive.

Bitcoin is slow and unusable for transactions. Get over it. ?

While banks and PayPal also at times charge high fees for the processing of a transaction, these pale in comparison to how much the Bitcoin system charges. Over the years, the fees have continued to increase which has made the network less effective for users and has led to many problems.

It is also evident that the fees vary depending on the size of a transaction which means that users can never be sure of what they're actually paying; the size of the fee also varies based on the exchange which is used in a particular scenario. The varying fees can also be applied to varying terms which continues to create a degree of uncertainty given a situation and how a particular aspect may work.

This also means that transactions cannot be confirmed in any short amount of time, especially when compared to services such as Visa and PayPal. It takes a long time to complete a transaction which is frustrating for users and makes the whole network rather impractical for everyday use. Confirming a single transaction can take anywhere from a few minutes to a few hours (or even longer, in some extreme cases.)

Furthermore, if one decides to mine the currency (which is how transactions are confirmed and new Bitcoins come into existence), then the person is faced with a wide array of problems that can occur. It takes a long time and a lot of energy to mine the coin, and mining is really only profitable if you own a roomful of expensive equipment. This is because Bitcoin’s mining difficulty was designed to increase over time; transactions take an increasing amount of energy and hashpower (computing power) to be confirmed.

The Bitcoin network has also struggled in terms of easy access for users who want to use their Bitcoins to pay for things. There are not a great number of methods for paying which are ready for the currency, leaving users limited to what they can do with their coins. The currency itself is not accepted by many places and those that do place restrictions on how it can be used. This means that the primary purpose of Bitcoin, which is a currency, is severely undermined by logistics. Effectively it cannot be said to function as the ‘digital cash’ that it was originally intended to be.

These limitations need to be addressed in the long-run if the currency is to ensure that it continues its growth and evolves into something which can be considered a serious contender for financial transactions in the future. If these problems are not alleviated, then it would make little sense for anyone to use Bitcoin as anything other than a long-term store of value, and even that could be a risky practice.

The Value of Bitcoin

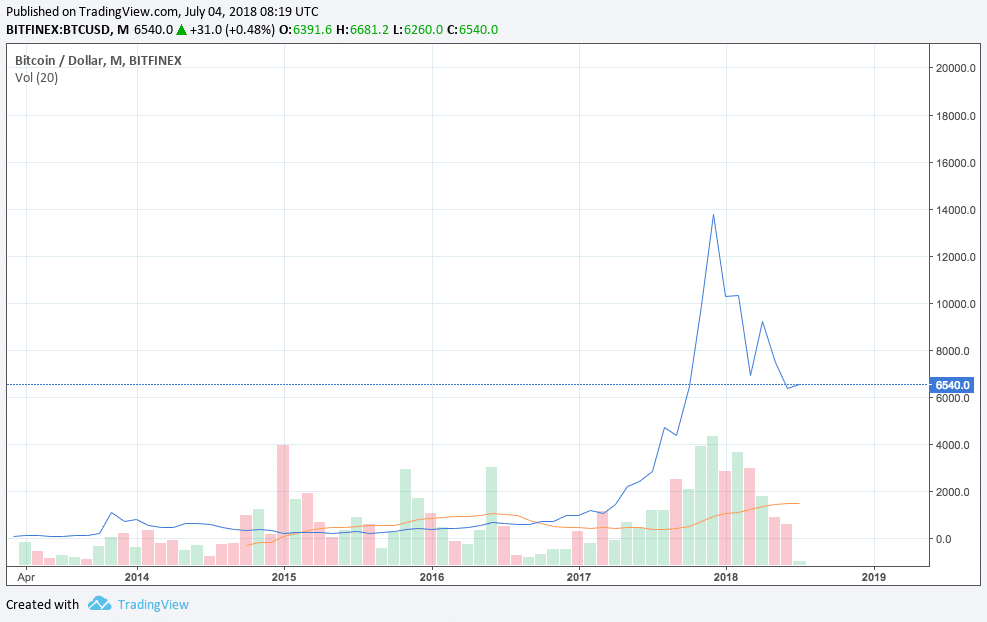

A major feature of Bitcoin over the course of its existence has been the wild fluctuations in its price. It has seen an astronomical rise in value since its inception, but it has also experienced major losses in recent months.

At the time of writing Bitcoin's value is at around $6700 which is far less than it was in November of 2017 when it broke the $10,000 barrier for the first time. The fall in the value of the coin occurred due to various pieces of news over the year, such as the fact that 80 percent of the Bitcoin in existence has already been mined, or the hack of the Coincheck Exchange. As such it is clear that the value of the coin is something which fluctuates wildly.

This affects other cryptocurrencies as well, as the price of Bitcoin tends to influence how well other coins perform. Bitcoin's epic fall was felt in shockwaves throughout the cryptocurrency markets.

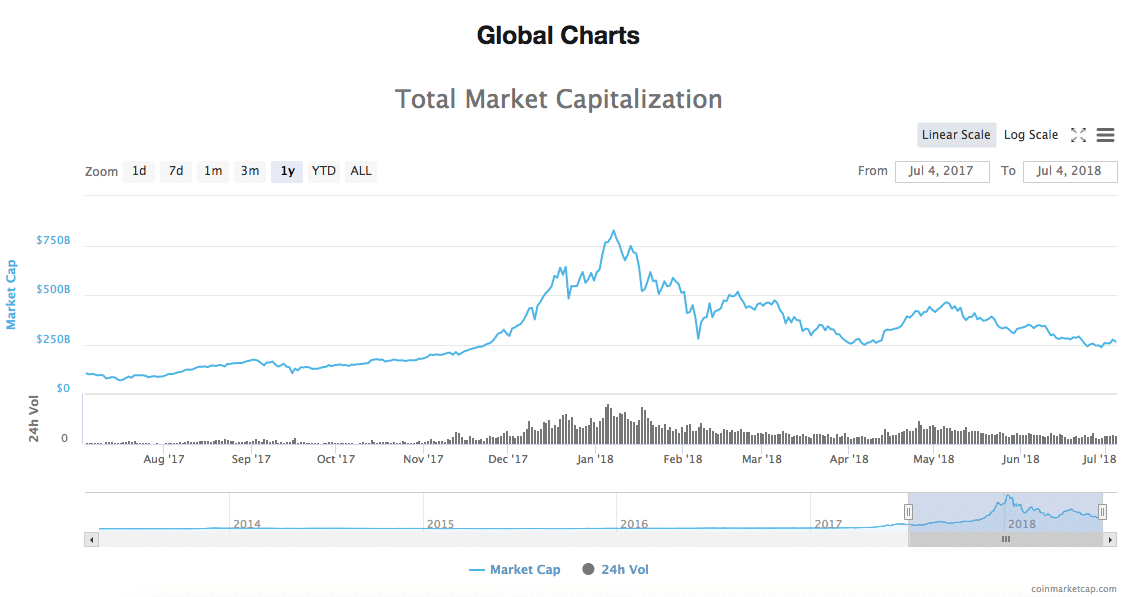

The total market capitalization of all cryptocurrencies fell along with Bitcoin's.

Where Can I Use My Bitcoins?

Bitcoins can be used in numerous places and have a wide array of uses for many an individual. In recent times, the desire to use Bitcoin as a form of digital cash has reduced in many ways and does not have the same pull as it perhaps used to. That being said, there are still numerous ways that one can use their Bitcoins in the everyday world which can be found below.

Bitcoin can be used for gift cards from various places such as Gyft or eGyfter; some merchants offer users who use these gift cards certain discounts.

Websites such as Expedia also utilize the currency for travel which is particularly useful for those looking to plan their travel arrangements. Given the size of the company, this option, in particular, is rather impressive. The Microsoft, App Store is another major place which accepts Bitcoins, pushing the legitimacy of the coin even further.

There are numerous other ways the coin can be used, and there are likely to be more in the future. A key aspect of the coin also lies in the trade of this coin for other important currencies such as Ethereum which allow for the coin to be able to grow in size and make the vast amount of trade in the crypto world. To fully utilize this, however, one would need to look at markets and ensure that they can make the most money possible with the maximum knowledge.

However, throughout the 2000s, there was a different beast being developed. On August 18, 2008, Bitcoin.org was registered as a domain name. By October of the same year, a document entitled "Bitcoin: A Peer to Peer Electronic System" was published by an entity using the name ‘Satoshi Nakamoto.’ The network then came into being a reality on the January 3, 2009, when Satoshi Nakamoto mined the "genesis block" which was rewarded at 50 bitcoin.

Who is Satoshi Nakamoto?

The identity of the enigmatic Satoshi Nakamoto has long been a mystery in crypto circles and has caused much debate.

The name is obviously a pseudonym, but no one seems to quite know who the person behind the figure is. For example, Craig Steven Wright has come out and stated that he is the inventor of the currency, but there is quite a bit of skepticism about that claim. Wright is an Australian computer scientist and entrepreneur who has shown a keen interest and history of developing cryptocurrencies. Nick Szabo and Dorian Nakamoto have also been named as potential creators of the currency.

While the true identity of Satoshi is unknown, the most likely theory seems to be that that the currency was created by more than one individual and was the work of a team of people.

Bitcoin's network runs on a Proof-of-Work algorithm. This algorithm is the means by which new Bitcoins are produced, and transactions are confirmed, a process known as mining.

The blockchain is virtually impervious to cyber attacks that often affect centralized entities: denial of service, as well as spam and other potentially malicious attacks. It is also incredibly difficult to falsify transactions on the Bitcoin network.

A user needs to be able to understand what a hash function is in this context, given its complexity. In essence, this function makes it so any kind of data can be mapped in any amount for a specific type of reason. If secured properly, this function cannot be differentiated from a random function in a given situation.

how to get funding:

keep saying blockchain really fast until people in suits get confused and throw you money

— I Am Devloper (@iamdevloper) January 24, 2018

In Proof of Work, the individual who is chosen to confirm a transaction is usually the individual with the most "hash power" (computing power.) They use their hash power to solve complex equations; once an answer is discovered, a 'block' (a small group) of transactions are confirmed. This typically happens at a rate of 3-4 transactions per second. In return for their work, miners are given rewards in the form of BTC tokens.

If this is done properly, and the correct cryptographical aspects are applied, then the solution should only be found by applying the "brute force" method, which entails looking to try every single possible combination until the correct answer is found.

This system has been effective until the present time, but one must also note that it does consume a vast quantity of energy. To illustrate this point, the vast majority of countries in Africa use up less energy than the network for mining Bitcoin.

An alternative to Proof of Work, the Proof of Stake algorithm, limits the amount of currency one can utilize in the space of given time. This system is not used by Bitcoin, but is used for coins such as Blackcoin; This system allows an individual to bypass problems such as the vast energy consumption which comes with Proof-of-Work, and to create a greener and energy efficient method to mine Bitcoin. However, this algorithm is not quite as popular as Proof of Work.

Problems with the Bitcoin Network

The Bitcoin Network, despite its numerous strengths, has some issues which need addressing about how the currency should work. The two primary problems associated with Bitcoin’s high fees and scalability.

The Bitcoin network has seen an increased number of transactions in the past few years, which has caused the network to come under strain. In other words, there are simply too many transactions for the networks to process in a reasonable amount of time. On a practical level, this means that transactions can take hours to complete and be extremely expensive.

Bitcoin is slow and unusable for transactions. Get over it. ?

While banks and PayPal also at times charge high fees for the processing of a transaction, these pale in comparison to how much the Bitcoin system charges. Over the years, the fees have continued to increase which has made the network less effective for users and has led to many problems.

It is also evident that the fees vary depending on the size of a transaction which means that users can never be sure of what they're actually paying; the size of the fee also varies based on the exchange which is used in a particular scenario. The varying fees can also be applied to varying terms which continues to create a degree of uncertainty given a situation and how a particular aspect may work.

This also means that transactions cannot be confirmed in any short amount of time, especially when compared to services such as Visa and PayPal. It takes a long time to complete a transaction which is frustrating for users and makes the whole network rather impractical for everyday use. Confirming a single transaction can take anywhere from a few minutes to a few hours (or even longer, in some extreme cases.)

Furthermore, if one decides to mine the currency (which is how transactions are confirmed and new Bitcoins come into existence), then the person is faced with a wide array of problems that can occur. It takes a long time and a lot of energy to mine the coin, and mining is really only profitable if you own a roomful of expensive equipment. This is because Bitcoin’s mining difficulty was designed to increase over time; transactions take an increasing amount of energy and hashpower (computing power) to be confirmed.

The Bitcoin network has also struggled in terms of easy access for users who want to use their Bitcoins to pay for things. There are not a great number of methods for paying which are ready for the currency, leaving users limited to what they can do with their coins. The currency itself is not accepted by many places and those that do place restrictions on how it can be used. This means that the primary purpose of Bitcoin, which is a currency, is severely undermined by logistics. Effectively it cannot be said to function as the ‘digital cash’ that it was originally intended to be.

These limitations need to be addressed in the long-run if the currency is to ensure that it continues its growth and evolves into something which can be considered a serious contender for financial transactions in the future. If these problems are not alleviated, then it would make little sense for anyone to use Bitcoin as anything other than a long-term store of value, and even that could be a risky practice.

The Value of Bitcoin

A major feature of Bitcoin over the course of its existence has been the wild fluctuations in its price. It has seen an astronomical rise in value since its inception, but it has also experienced major losses in recent months.

At the time of writing Bitcoin's value is at around $6700 which is far less than it was in November of 2017 when it broke the $10,000 barrier for the first time. The fall in the value of the coin occurred due to various pieces of news over the year, such as the fact that 80 percent of the Bitcoin in existence has already been mined, or the hack of the Coincheck Exchange. As such it is clear that the value of the coin is something which fluctuates wildly.

This affects other cryptocurrencies as well, as the price of Bitcoin tends to influence how well other coins perform. Bitcoin's epic fall was felt in shockwaves throughout the cryptocurrency markets.

The total market capitalization of all cryptocurrencies fell along with Bitcoin's.

Where Can I Use My Bitcoins?

Bitcoins can be used in numerous places and have a wide array of uses for many an individual. In recent times, the desire to use Bitcoin as a form of digital cash has reduced in many ways and does not have the same pull as it perhaps used to. That being said, there are still numerous ways that one can use their Bitcoins in the everyday world which can be found below.

Bitcoin can be used for gift cards from various places such as Gyft or eGyfter; some merchants offer users who use these gift cards certain discounts.

Websites such as Expedia also utilize the currency for travel which is particularly useful for those looking to plan their travel arrangements. Given the size of the company, this option, in particular, is rather impressive. The Microsoft, App Store is another major place which accepts Bitcoins, pushing the legitimacy of the coin even further.

There are numerous other ways the coin can be used, and there are likely to be more in the future. A key aspect of the coin also lies in the trade of this coin for other important currencies such as Ethereum which allow for the coin to be able to grow in size and make the vast amount of trade in the crypto world. To fully utilize this, however, one would need to look at markets and ensure that they can make the most money possible with the maximum knowledge.

Malta Regulator Flags Surge in Crypto Scams Exploiting MiCA Transition

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.