Britain's financial markets regulator has today released a consultation paper which outlines the proposed management expenses levy limit (MELL) for the FSCS for 2014 and 2015.

As the Financial Conduct Authority (FCA) enters its second year in existence following its assumption of duties from its long-standing predecessor, the Financial Services Authority, proposals are contained within today's consultation paper which the regulatory authority advises that all registered financial services companies should read.

FCA Considers Implementing £80 Million MELL

The FCA stipulates that under the Financial Services and Markets Act 2000 (FSMA), both the FCA which oversees the conduct of financial services firms as well as being responsible for customer protection, and Prudential Regulation Authority (PRA), which is responsible for ensuring the appropriate conduct of banks in Britain, must set a limit on the total management expenses levied, that gives the Financial Services Compensation Scheme (FSCS) adequate resources to perform its functions efficiently and economically and provide a responsive and well-understood compensation service for financial services consumers.

On this basis, the FCA has proposed in its consultation paper on the matter that this should be set at £80 million for the years 2014 and 2015.

Additionally, the consultation paper aims this proposal squarely at companies which operate in the UK's financial sector solely, therefore being applicable to companies in this sector rather than bearing any relevance whatsoever to consumers or consumer groups.

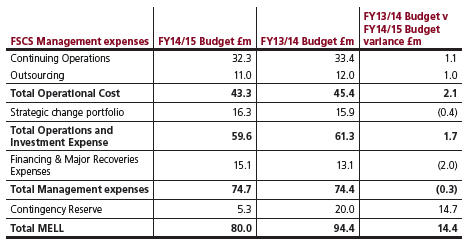

The proposed structure which the MELL could be scheduled to take comprises of FSCS management expenses of £74.7m, which is the minimum amount that will be levied for 2014 and 2015.

A contingency reserve of £5.3m should make up the difference, which allows the FSCS to levy additional funds without formal consultation by the FCA and PRA, in order to meet contingencies that were not expected when the annual levy was raised.

This, according to the FCA, would most probably be at relatively short notice, and would not be levied unless required by the FSCS.

Time is most certainly of the essence in responding to this proposal, with the FCA having stipulated that comments from regulated entities on the proposed MELLs must be sent to the regulatory authority by February 17, just less than one month from now.

After reviewing consultation responses, and subject to approval in March 2014 by the FCA Board and the PRA Board, both regulators will finalize the proposal in this CP to take effect on 1 April, 2014, with invoices due to be sent out from July 2014.

What Purpose Does The Limit Perform?

The FCA has detailed that the amount levied to pay compensation claims is determined by the FSCS and is not consulted on. There are limits under the FEES rules on how much firms can be levied each year. The FSCS indicates its current estimated compensation figures and its related funding and levies in its Plan and Budget. The FSCS states that it is to confirm its actual levy requirements in early April 2014.

The management expenses levy is made up of a specific cost element, which comprises costs attributable to a particular funding class and allocated to that class 8 January, 2014 FCA and PRA.

The PRA's Financial Services Compensation Scheme is scheduled to contain a management expenses levy limit for 2014 and 2015, consisting of a base cost element, relating to the general costs of the FSCS (which is not dependent on the level of claims received).

Base costs are divided equally between the PRA and FCA regulatory fee classes, and then distributed in proportion to regulatory fees.

The benefits from the FSCS are to improve consumer confidence, increase consumer protection and financial stability. The main consumer protection benefit is the reduced financial loss to consumers in the event of firm failure, a matter which regulatory authorities have begun to look at very closely since the demise of MF Global and Peregrine Financial Group in North America, a jurisdiction which raised capital adequacy requirements for retail firms to $20 million in order to mitigate the occurrence of such incidents.

Cost Advantage

It is difficult to estimate the number of potential instances of firm failure which may occur during 2014 and 2015, along with the subsequent reduction in financial losses to consumers due to FSCS compensation. However, to illustrate the potential scale of the benefits to consumers, the average annual value of compensation paid out over the past three years is £400 million.

The FCA expects that the contingency reserve of £5.3m will give the FSCS some margin to meet costs that exceed its budgeted expenses and need to be funded at short notice. The FCA and PRA recognise that the FSCS needs to be able to respond quickly and efficiently to firm failures. If a particular failure or series of failures meant that the MELL needed to be increased, the FCA and PRA intend, under this proposal, to take the necessary steps to enable the FSCS to meet its Obligations in a timely way.

Overview of FSCS Budget Information

Source: Financial Conduct Authority