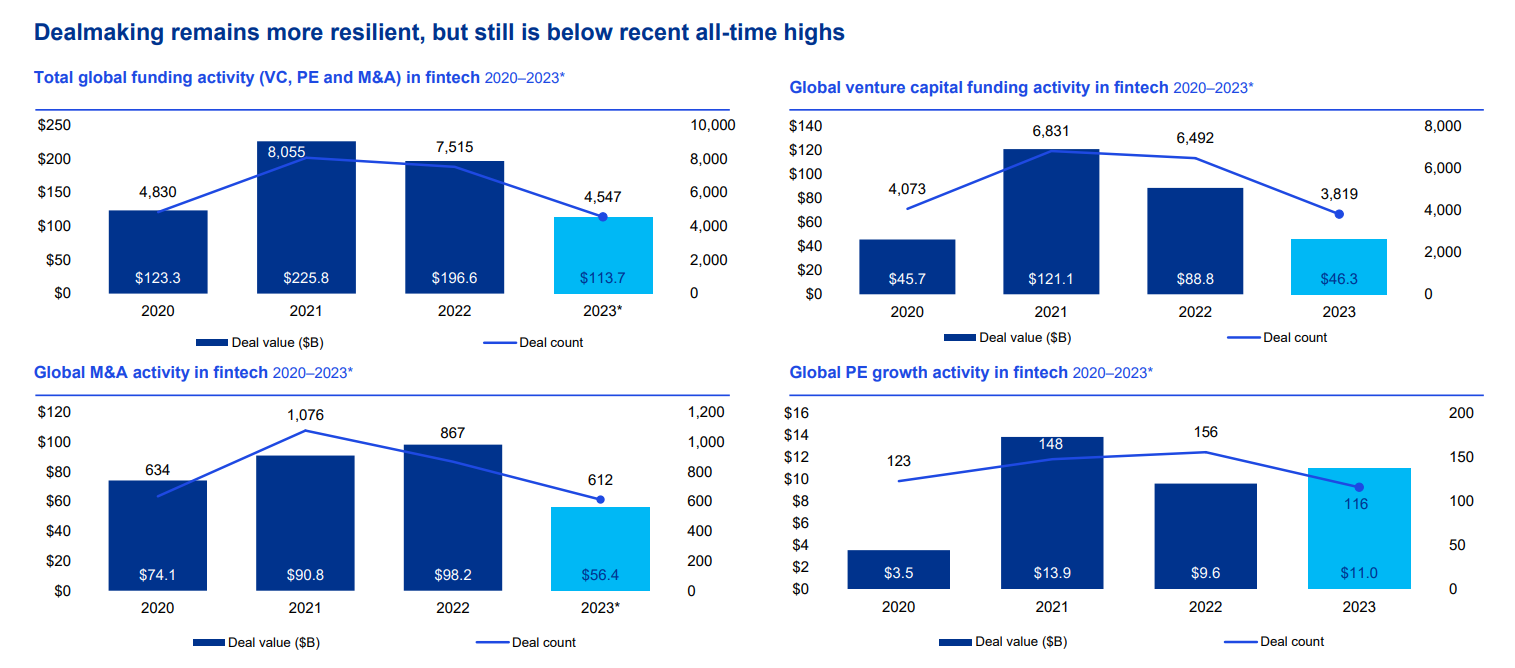

The latest Pulse of Fintech report by KPMG highlighted a notable downturn in fintech investment in 2023. Global fintech investment fell to $113.7 billion in 2023, a significant drop from $196.3 billion in 2022. The number of fintech deals also declined to 4,547, marking the lowest level since 2017.

Fintech Investment Drops in 2023 amid Global Challenges

As investment sentiment cooled significantly, global funding for fintech reached its lowest point in five years, totaling $113.7 billion through 4,547 transactions in 2023. This pullback was influenced by concerns over high interest rates that persisted, geopolitical tensions in Ukraine and the Middle East, declining fintech valuations, and a challenging exit landscape.

“2023 was a difficult year for the fintech market globally, with both total fintech investments,” commented Anton Ruddenklau, the Global Head of Fintech and Innovation at KPMG. “The year-over-year decline in fintech investment occurred across all key regions.”

Global fintech investment experienced a slight uptick between the first and second halves of the year, climbing from $55.5 billion in H1 2023 to $58.2 billion in H2. This increase was fueled by six blockbuster deals exceeding $1 billion each.

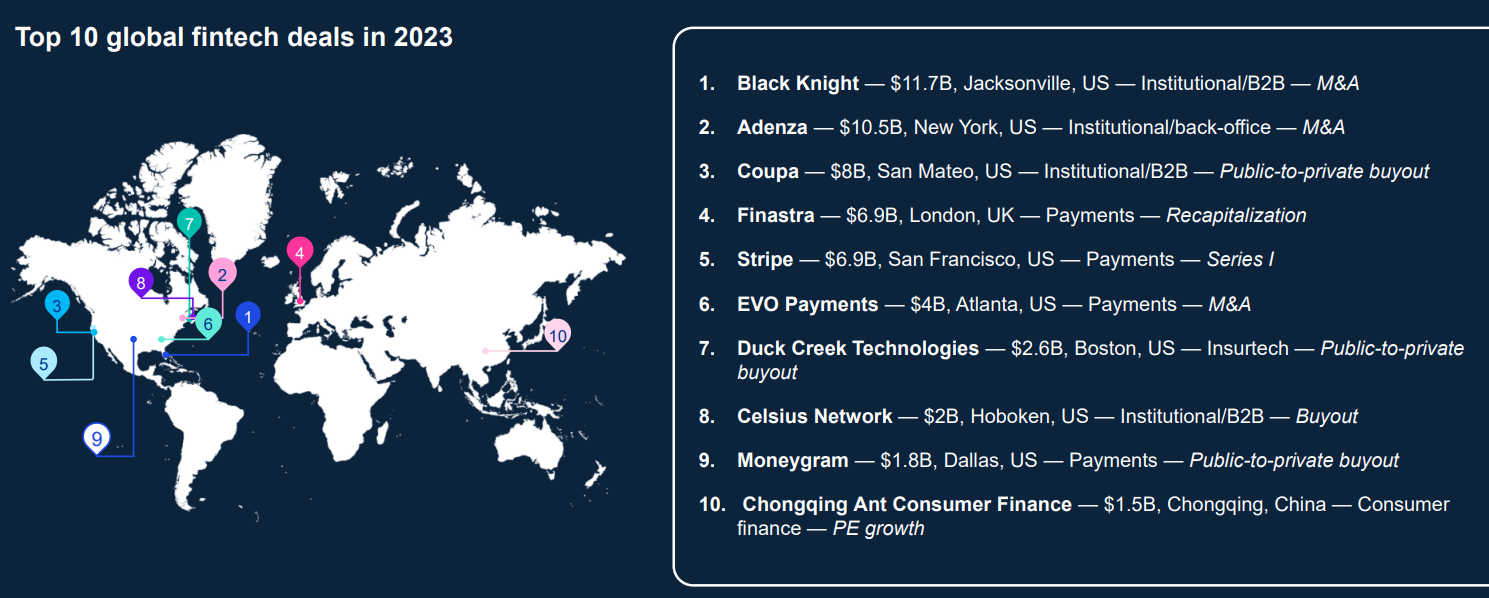

Notable transactions included the acquisition of US-based Black Knight by Intercontinental Exchange for $11.7 billion, the acquisition of US-based Adenza by Nasdaq for $10.5 billion, a private equity raise of $6.9 billion by UK-based Finastra, the buyout of US-based Avantax by Cetera for $1.2 billion, the venture capital raise by California-based Generate for $1 billion, and the acquisition of Brazil-based Pismo by Visa for $1 billion.

Regional and Sector Trends

This drop occurred across all major regions, with the steepest declines in Asia-Pacific and Europe. Investment in the Americas showed the most resilience but still fell 18% year-over-year. The US continued to lead, accounting for nearly two-thirds of all fintech funding, securing $78.3 billion over 2,136 transactions.

These figures are confirmed by a separate report from Innovate Finance, which was presented earlier this year. It claims that the United Arab Emirates has managed to break free from the negative trend, with fintech funding nearly doubling, growing 92%.

Payments remained the top sector by deal volume, despite funding falling 64% to $20.7 billion. Proptech and insurtech were rare bright spots, being the only subsectors seeing rising investment.

“While the investment numbers are soft now — due to broader market conditions — the next year could be quite exciting for innovation in the fintech space,” added Karim Haji, the Global Head of Financial Services at KPMG.

However, global venture capital (VC) investment in fintech witnessed a significant decline year-over-year and between the first and second halves of 2023. The total VC investment plummeted from $88.8 billion in 2022 to $46.3 billion in 2023, marking a substantial decrease. Similarly, the VC investment between H1 ($27.5 billion) and H2 ($18.8 billion) also experienced a sharp drop. Notably, investment in later-stage deals decreased drastically from $37.4 billion in 2022 to $14.1 billion in 2023.

Fintech investors grew more cautious amidst global instability, inflation concerns, and doubts about valuations and exit opportunities. They increasingly focused on profitability and sustainability, shunning risky bets. Partnerships and B2B solutions attracted interest as did AI and embedded finance.

Murky Forecasts

Investment is expected to stay soft in early 2024 before recovering later in the year as rates potentially fall. M&A activity may also pick up as investors buy distressed assets.

The report highlighted one outlier to the trends: seed and early-stage funding hit record highs in terms of deal numbers, indicating investors are still keen to test new fintech models. Additionally, the report mentioned that AI would play an increasingly significant role in the fintech industry. This was also the topic of one of the recent panels during the Finance Magnates London Summit.

As the report concluded, enhancing profitability and sustainability will be key for fintech firms to thrive long-term amidst the current challenges.