ASEAN stocks are distributing massive dividends to the investors. But investors must be cautious, as some dividend basket strategies can be risky. Paul Golden weighs in.

He also explores the frustration of UK investors with share buybacks and the increased interest in defence stocks.

Flags of ASEAN country members

It’s Payback Time for Asian Stockholders…

For years, ASEAN has been framed almost exclusively as a growth story. Favourable demographics, rising consumption and the relocation of manufacturing have positioned Southeast Asia as one of the most dynamic emerging regions in the world.

But as the region’s economy matures, a new narrative is taking shape. ASEAN is no longer just about growth; it is increasingly becoming a compelling destination for dividend seekers.

Miko Huang, Senior Manager, Equity Index Product Management APAC at London Stock Exchange Group

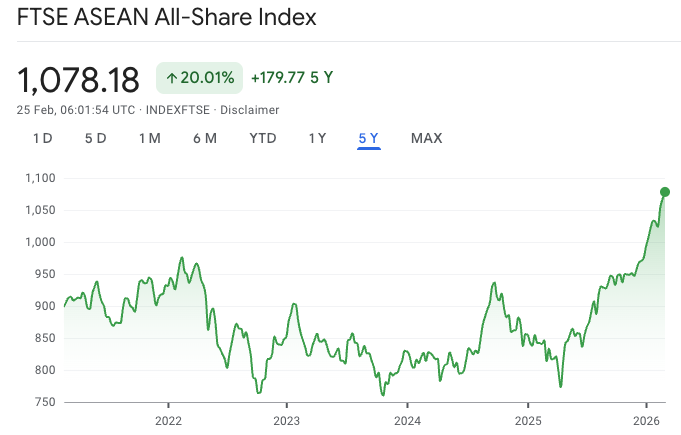

That is the view of Miko Huang, Senior Manager, Equity Index Product Management APAC at London Stock Exchange Group, who notes that the FTSE ASEAN Index, which captures the large- and mid-cap companies listed in the five ASEAN markets (Singapore, Malaysia, Indonesia, Thailand and the Philippines), has delivered a 10-year average dividend yield of 3.57%.

This exceeds the yields of many major global benchmarks, including the FTSE Asia Pacific ex Japan Australia and New Zealand Index (2.49%), the FTSE USA Index (1.68%), the FTSE Developed Europe Index (3.18%) and the FTSE Emerging Index (2.9%).

Over the last five years, the FTSE ASEAN Index has recorded steady growth in cash flow per share, and the region’s average dividend payout ratio during this period also stands out relative to global peers. The forward 12-month dividend yield remains attractive compared with other major markets worldwide, highlighting the region’s appeal for income-oriented investors.

FTSE ASEAN Index (Source: Google Finance)

As of the end of last year, more than 60% of the large- and mid-cap companies in the FTSE ASEAN Index offered dividend yields above 3%, reflecting a management culture that focuses on shareholder returns.

However, Huang cautions that not all dividend strategies are created equal. Traditional dividend approaches often focus on the highest-yielding stocks, which can lead to excessive portfolio concentration and above-average exposure to smaller companies or businesses with weakening fundamentals.

“Many dividend indices simply rank stocks by yield and pick the companies at the top of the ranking,” she says. “The problem with that approach is that very high yields are often a warning sign. They can come from smaller or distressed companies where the share price has already fallen sharply, creating what we call a ‘yield trap’. While the yield may appear attractive, it is often unsustainable, as the share price fall is an early indicator of a future dividend cut.”

…While Their UK Counterparts Are Frustrated by Buybacks

According to Computershare’s Q4 2025 UK Dividend Monitor, UK dividends fell 0.9% to £87.5 billion on a headline basis in 2025, while one-off special dividends of £2.9 billion were half the 10-year average.

Share buybacks reached a provisional £63.6 billion in 2025, more than double the 2019 level, while dividends have fallen by 13% over the same period. Share buybacks have slowed dividend growth by 3% per annum since 2019 by diverting cash to repurchases rather than distributions.

Mark Cleland, CEO of Governance Services at Computershare

Mark Cleland, CEO of Governance Services at Computershare, observes that for 2026 there are relatively few major growth drivers to push dividends higher. Declines in mining payouts are likely to slow further or stop altogether, banks are likely to continue to deliver modest growth, and energy payouts are likely to be flat.

Across the wider market, Computershare projects steady, low single-digit growth. Meanwhile, the dampening effect of share buybacks and the strong pound is set to continue (if sterling maintains its current rate), though the exchange rate effect will weaken as the year progresses.

“For Q1 2026, Next has already declared a very large payment of £3.60 per share, reflecting both very strong trading and associated cash generation, as well as some land disposals,” says Cleland. “This will ensure the Q1 2026 special dividend total easily exceeds Q1 2025, though we assume for now that the full year will be roughly flat, given the unpredictable nature of this form of payout.”

No Time to Be Squeamish About Defence Stocks

The phrase “buy when there is blood in the streets, even if the blood is your own” is a contrarian investment maxim frequently attributed to Baron Rothschild, who allegedly made a fortune buying during the panic following the Battle of Waterloo.

It means buying assets when market fear is at its highest, others are panic-selling, and prices are falling, even if your own investments are losing value.

Sadly, there has been blood in the streets in too many parts of the world recently. In particular, the conflict in Ukraine (and criticism of Europe’s commitment to its armed forces from members of the Trump administration) has focused attention on Europe’s ability to defend its borders.

Until relatively recently, investors were reluctant to buy defence stocks in large volumes, partly due to ethical concerns. But inflows rose significantly following Russia’s invasion of its south-west neighbour in 2022 and, after a brief lull, rose again when the US President made it clear that he expected NATO countries to make a more substantial contribution to the defence of the continent.

Hargreaves Lansdown’s December 2025 Sustainable Investor Survey recorded a sharp fall in the number of investors who excluded weapons from their allocations. Many European investors have re-evaluated how investing in defence stocks aligns with ESG commitments, leading defence sector-focused funds to reach an all-time high.

The European Commission’s ReArm Europe Plan/Readiness 2030, presented in March 2025, proposes leveraging over €800 billion in defence spending through national fiscal flexibility, a new €150 billion loan instrument (SAFE) for joint procurement, potential redirection of cohesion funds, and expanded European Investment Bank support.

Thematic European ETFs have also benefited, with $6.3 billion in positive net flows into global defence last year, accounting for 40% of all new money that moved into this sector in 2025. European defence was the next highest contributor to new flows, representing an additional 30%.

It’s Payback Time for Asian Stockholders…

For years, ASEAN has been framed almost exclusively as a growth story. Favourable demographics, rising consumption and the relocation of manufacturing have positioned Southeast Asia as one of the most dynamic emerging regions in the world.

But as the region’s economy matures, a new narrative is taking shape. ASEAN is no longer just about growth; it is increasingly becoming a compelling destination for dividend seekers.

Miko Huang, Senior Manager, Equity Index Product Management APAC at London Stock Exchange Group

That is the view of Miko Huang, Senior Manager, Equity Index Product Management APAC at London Stock Exchange Group, who notes that the FTSE ASEAN Index, which captures the large- and mid-cap companies listed in the five ASEAN markets (Singapore, Malaysia, Indonesia, Thailand and the Philippines), has delivered a 10-year average dividend yield of 3.57%.

This exceeds the yields of many major global benchmarks, including the FTSE Asia Pacific ex Japan Australia and New Zealand Index (2.49%), the FTSE USA Index (1.68%), the FTSE Developed Europe Index (3.18%) and the FTSE Emerging Index (2.9%).

Over the last five years, the FTSE ASEAN Index has recorded steady growth in cash flow per share, and the region’s average dividend payout ratio during this period also stands out relative to global peers. The forward 12-month dividend yield remains attractive compared with other major markets worldwide, highlighting the region’s appeal for income-oriented investors.

FTSE ASEAN Index (Source: Google Finance)

As of the end of last year, more than 60% of the large- and mid-cap companies in the FTSE ASEAN Index offered dividend yields above 3%, reflecting a management culture that focuses on shareholder returns.

However, Huang cautions that not all dividend strategies are created equal. Traditional dividend approaches often focus on the highest-yielding stocks, which can lead to excessive portfolio concentration and above-average exposure to smaller companies or businesses with weakening fundamentals.

“Many dividend indices simply rank stocks by yield and pick the companies at the top of the ranking,” she says. “The problem with that approach is that very high yields are often a warning sign. They can come from smaller or distressed companies where the share price has already fallen sharply, creating what we call a ‘yield trap’. While the yield may appear attractive, it is often unsustainable, as the share price fall is an early indicator of a future dividend cut.”

…While Their UK Counterparts Are Frustrated by Buybacks

According to Computershare’s Q4 2025 UK Dividend Monitor, UK dividends fell 0.9% to £87.5 billion on a headline basis in 2025, while one-off special dividends of £2.9 billion were half the 10-year average.

Share buybacks reached a provisional £63.6 billion in 2025, more than double the 2019 level, while dividends have fallen by 13% over the same period. Share buybacks have slowed dividend growth by 3% per annum since 2019 by diverting cash to repurchases rather than distributions.

Mark Cleland, CEO of Governance Services at Computershare

Mark Cleland, CEO of Governance Services at Computershare, observes that for 2026 there are relatively few major growth drivers to push dividends higher. Declines in mining payouts are likely to slow further or stop altogether, banks are likely to continue to deliver modest growth, and energy payouts are likely to be flat.

Across the wider market, Computershare projects steady, low single-digit growth. Meanwhile, the dampening effect of share buybacks and the strong pound is set to continue (if sterling maintains its current rate), though the exchange rate effect will weaken as the year progresses.

“For Q1 2026, Next has already declared a very large payment of £3.60 per share, reflecting both very strong trading and associated cash generation, as well as some land disposals,” says Cleland. “This will ensure the Q1 2026 special dividend total easily exceeds Q1 2025, though we assume for now that the full year will be roughly flat, given the unpredictable nature of this form of payout.”

No Time to Be Squeamish About Defence Stocks

The phrase “buy when there is blood in the streets, even if the blood is your own” is a contrarian investment maxim frequently attributed to Baron Rothschild, who allegedly made a fortune buying during the panic following the Battle of Waterloo.

It means buying assets when market fear is at its highest, others are panic-selling, and prices are falling, even if your own investments are losing value.

Sadly, there has been blood in the streets in too many parts of the world recently. In particular, the conflict in Ukraine (and criticism of Europe’s commitment to its armed forces from members of the Trump administration) has focused attention on Europe’s ability to defend its borders.

Until relatively recently, investors were reluctant to buy defence stocks in large volumes, partly due to ethical concerns. But inflows rose significantly following Russia’s invasion of its south-west neighbour in 2022 and, after a brief lull, rose again when the US President made it clear that he expected NATO countries to make a more substantial contribution to the defence of the continent.

Hargreaves Lansdown’s December 2025 Sustainable Investor Survey recorded a sharp fall in the number of investors who excluded weapons from their allocations. Many European investors have re-evaluated how investing in defence stocks aligns with ESG commitments, leading defence sector-focused funds to reach an all-time high.

The European Commission’s ReArm Europe Plan/Readiness 2030, presented in March 2025, proposes leveraging over €800 billion in defence spending through national fiscal flexibility, a new €150 billion loan instrument (SAFE) for joint procurement, potential redirection of cohesion funds, and expanded European Investment Bank support.

Thematic European ETFs have also benefited, with $6.3 billion in positive net flows into global defence last year, accounting for 40% of all new money that moved into this sector in 2025. European defence was the next highest contributor to new flows, representing an additional 30%.

Paul Golden is an experienced freelance financial journalist with a strong institutional background. Over the past two decades, he has written for globally recognised financial publications, covering topics such as market structure, regulation, trading behaviour, and economic policy.

iFOREX Adds 19% More Clients in H1, Shekel Takes $1.8M Bite

Featured Videos

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Friday, the 24th of July 2026, and these are our main stories: the FCA finds major gaps in anti-money laundering controls at alternative asset managers, Wise shares tumble after a US banking licence setback, and Google's EU fines could benefit fintech apps.

Today's Friday, the 24th of July 2026, and these are our main stories: the FCA finds major gaps in anti-money laundering controls at alternative asset managers, Wise shares tumble after a US banking licence setback, and Google's EU fines could benefit fintech apps.

Today's Friday, the 24th of July 2026, and these are our main stories: the FCA finds major gaps in anti-money laundering controls at alternative asset managers, Wise shares tumble after a US banking licence setback, and Google's EU fines could benefit fintech apps.

Today's Friday, the 24th of July 2026, and these are our main stories: the FCA finds major gaps in anti-money laundering controls at alternative asset managers, Wise shares tumble after a US banking licence setback, and Google's EU fines could benefit fintech apps.

Today's Friday, the 24th of July 2026, and these are our main stories: the FCA finds major gaps in anti-money laundering controls at alternative asset managers, Wise shares tumble after a US banking licence setback, and Google's EU fines could benefit fintech apps.

Today's Friday, the 24th of July 2026, and these are our main stories: the FCA finds major gaps in anti-money laundering controls at alternative asset managers, Wise shares tumble after a US banking licence setback, and Google's EU fines could benefit fintech apps.

FM Daily Brief – 23 July 2026

FM Daily Brief – 23 July 2026

FM Daily Brief – 23 July 2026

FM Daily Brief – 23 July 2026

FM Daily Brief – 23 July 2026

FM Daily Brief – 23 July 2026

Today's Thursday, the 23rd of July 2026, and these are our main stories: BitMEX announces it will shut down its crypto trading platform, the Financial Commission launches a certification programme for prop firms, and the SEC settles a records lawsuit with Coinbase.

Today's Thursday, the 23rd of July 2026, and these are our main stories: BitMEX announces it will shut down its crypto trading platform, the Financial Commission launches a certification programme for prop firms, and the SEC settles a records lawsuit with Coinbase.

Today's Thursday, the 23rd of July 2026, and these are our main stories: BitMEX announces it will shut down its crypto trading platform, the Financial Commission launches a certification programme for prop firms, and the SEC settles a records lawsuit with Coinbase.

Today's Thursday, the 23rd of July 2026, and these are our main stories: BitMEX announces it will shut down its crypto trading platform, the Financial Commission launches a certification programme for prop firms, and the SEC settles a records lawsuit with Coinbase.

Today's Thursday, the 23rd of July 2026, and these are our main stories: BitMEX announces it will shut down its crypto trading platform, the Financial Commission launches a certification programme for prop firms, and the SEC settles a records lawsuit with Coinbase.

Today's Thursday, the 23rd of July 2026, and these are our main stories: BitMEX announces it will shut down its crypto trading platform, the Financial Commission launches a certification programme for prop firms, and the SEC settles a records lawsuit with Coinbase.

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

FM Daily Brief – 21 July 2026

FM Daily Brief – 21 July 2026

FM Daily Brief – 21 July 2026

FM Daily Brief – 21 July 2026

FM Daily Brief – 21 July 2026

FM Daily Brief – 21 July 2026

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.