The Financial Conduct Authority (FCA) has released its consumer investments data review for the duration between April 2022 and March 2023, highlighting 1,716 warnings issued against unauthorized individuals and companies by the regulator.

During this period, the regulator barred one in every five new consumer investment firms that applied to enter the market. Besides that, the UK's watchdog secured £4.9m in consumer redress from unauthorized investment businesses.

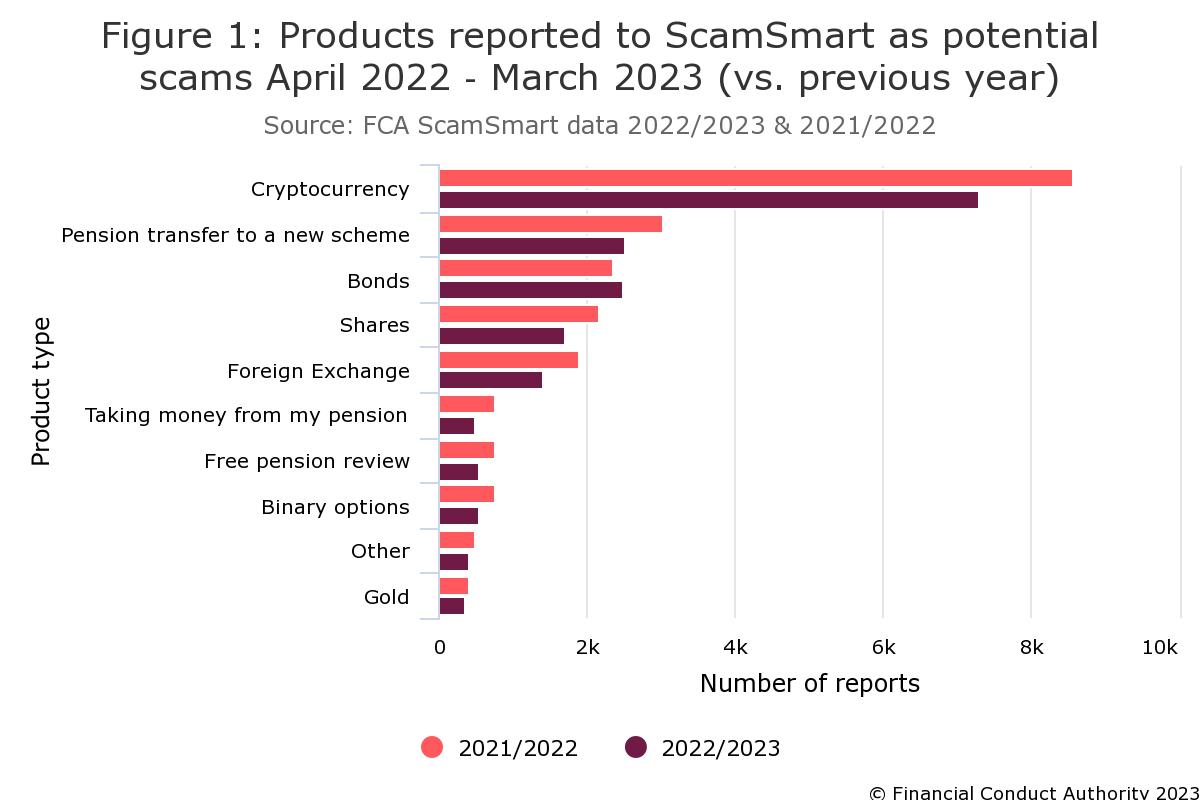

However, amidst these proactive measures, the report disclosed some of the regulatory challenges in the UK. There was a notable surge of helpline inquiries regarding potential scams, which jumped 12% since 2020, signaling persistent threats faced by investors.

Specific scams, including recovery room scams (21%), FCA impersonation scams (38%), and cryptocurrency scams (17%), have seen a notable uptick in inquiries. A staggering 80% of inquiries regarding potential cryptocurrency scams were made by investors after they had already invested.

FCA Combats Unauthorized Activities under New Regulations

According to the report, the regulator focused on curtailing unauthorized activities. The reports on potential unauthorized businesses exceeded 25,000, prompting investigations and enforcement actions against 212 firms and individuals, the FCA mentioned.

The FCA took a significant step in August 2022 by bolstering its financial promotion regulations for high-risk investments. These reforms aim to enhance consumer awareness and raise standards for firms and individuals involved in unauthorized financial promotions. By December 2022, the initial set of regulatory changes was enacted, mandating improved risk warnings in high-risk investment promotions.

However, shortly after the enactment of the regulations, a review of 67 crowdfunding and peer-to-peer firms revealed that 60% of the firms under assessment were non-compliant with the updated standards. Inquiries about scams surged while investment product-related inquiries decreased.

Recently, the FCA introduced temporary measures enabling investment companies to offer clearer cost disclosures. These measures allow consumers to make informed investment choices. This move is in response to concerns that existing disclosure rules generate ambiguous cost information.

FCA's Measures in Financial Obligations

The FCA's introduced measures empower funds to offer additional context in their cost disclosures. Additionally, the agency has encouraged firms to incorporate additional information into their broader disclosure documents while evaluating their obligations under the consumer duty.

Earlier proposals by the FCA mandated personal investment firms to maintain adequate capital reserves for compensating consumers affected by inadequate financial advice. This initiative implements a "polluter pays" principle, ensuring firms take responsibility for the financial advice they offer.

Under the proposals, investment advisors must assess potential liabilities, guaranteeing sufficient capital for compensation. This measure aims to curb substantial compensations disbursed by the Financial Services Compensation Scheme due to substandard advice.