For some, it is the future of finance; for others, it is a volatile fad too closely associated with criminal activity on the dark web. Those that are curious about acquiring bitcoin, however, can have a difficult time understanding the practical aspects of sending and receiving Bitcoin. That's what we'll cover in this article.

Two primary variables affect the transaction time for Bitcoin. The first is the amount of activity going on in the network.

Ultimately, if there is high network density (meaning that there are a lot of transactions to process), the transaction time will be far longer. The Bitcoin network processes an average of 3-4 transactions per second; if there are tens of thousands of transactions in the queue, it's going to take a long time.

Miners need to process each block, and it takes time for them to do that. If transaction fees are higher, however, miners are more likely to process the transaction quicker. Due to the volatile nature of the network, this means transactions can take anywhere from a few minutes to more than 12 hours to process, depending on network conditions.

Bloomberg

How do Bitcoin Transactions Work?

If someone wants to send bitcoin, their intention is logged when they commence the transaction. Then, the nodes scan the whole bitcoin network to confirm that the bitcoin is there to send and that it hasn’t already been sent to someone else.

Once this information is verified, the transaction gets included in a "block" which is attached to the previous block - hence the name: blockchain. Transactions cannot be canceled or manipulated, because this would mean altering all the blocks that came after, a virtually impossible task.

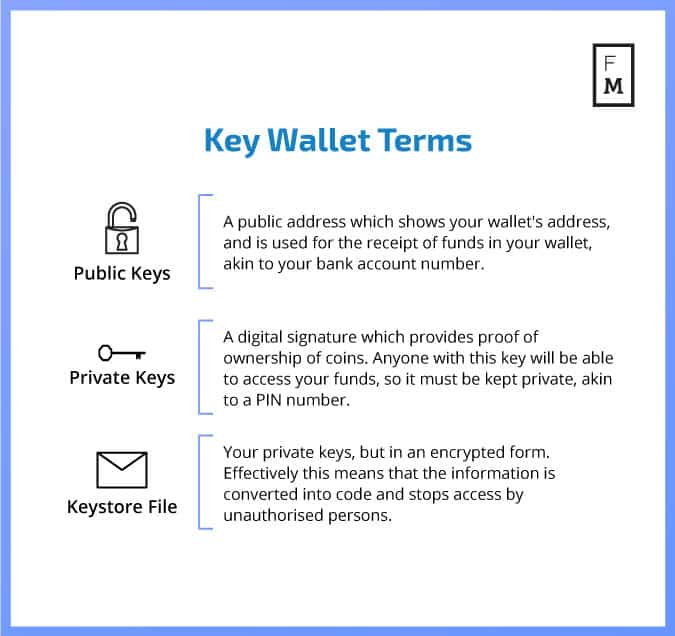

The bitcoin wallet does not hold bitcoin. Instead, it does is holds the bitcoin's private key and public address. This 'public address' - a long string of 34 letters and numbers - is also referred to as the "public key." Private keys are strings of characters that control coins--this is what is stored in a crypto wallet. The signature from the private key is what validates the transaction and allows it to go through.

As mentioned, there are two key factors to consider when making a Bitcoin transaction. You need a private key and a public address to send the coins to. Coinbase does, however, hold your private key, so it is not entirely within your control.

This is just something to consider from a security perspective; if you find Coinbase to be a trustworthy entity, then allowing them to keep your private keys in storage shouldn't be an issue. If this is a problem, however, you may want to consider storing your crypto in a way that allows you to have total control over your private keys.

Steps for Sending Funds:

Step 1: Open your software wallet and press the "Send" tab, or use the "Trade|Send Bitcoin" which can be found on your wallet menu.

Step 2: Enter the destination address for your recipient's wallet. This is the public address, add it by copy and pasting it, QR code, or writing it out by hand.

Step 3: Select a label to track your transaction.

Step 4: Enter the amount you’d like transferred in the BTC box.

Step 5: Review the details and make sure the info you entered is correct, as the transaction cannot be reversed.

Step 6: Press "Send" to finalize the transfer.

How to Receive Bitcoin

To receive Bitcoin, you only need your wallet and your public address (as well as your security features to access the wallet obviously).

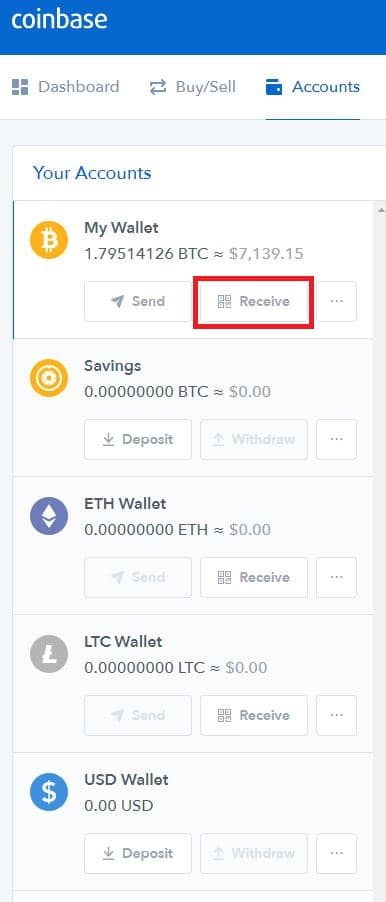

Step 1: Once you’ve set up your Coinbase account, click the “Accounts” tab. Here and you will find your wallets. Click the “Receive” button on your Bitcoin wallet.

Step 2: The address for your Bitcoin will be displayed. Share this address with anyone who would like to send you Bitcoin.

This occurs due to web trackers and cookies which are pieces of code that track the way sites are used and passed on to third parties. This info can be sent to Google, Facebook, etc. so they can analyze trends. In the same way, governments, law enforcement agencies, and hackers can just as easily gain access to this information.

For this to occur, an eavesdropper or a leaker is required. However, according to a study by Goldfeder, 53/140 Bitcoin merchants have leaked info to a vast number of third parties. This is primarily done for adverts and analytics but is still something to be aware of.

For some, it is the future of finance; for others, it is a volatile fad too closely associated with criminal activity on the dark web. Those that are curious about acquiring bitcoin, however, can have a difficult time understanding the practical aspects of sending and receiving Bitcoin. That's what we'll cover in this article.

Two primary variables affect the transaction time for Bitcoin. The first is the amount of activity going on in the network.

Ultimately, if there is high network density (meaning that there are a lot of transactions to process), the transaction time will be far longer. The Bitcoin network processes an average of 3-4 transactions per second; if there are tens of thousands of transactions in the queue, it's going to take a long time.

Miners need to process each block, and it takes time for them to do that. If transaction fees are higher, however, miners are more likely to process the transaction quicker. Due to the volatile nature of the network, this means transactions can take anywhere from a few minutes to more than 12 hours to process, depending on network conditions.

Bloomberg

How do Bitcoin Transactions Work?

If someone wants to send bitcoin, their intention is logged when they commence the transaction. Then, the nodes scan the whole bitcoin network to confirm that the bitcoin is there to send and that it hasn’t already been sent to someone else.

Once this information is verified, the transaction gets included in a "block" which is attached to the previous block - hence the name: blockchain. Transactions cannot be canceled or manipulated, because this would mean altering all the blocks that came after, a virtually impossible task.

The bitcoin wallet does not hold bitcoin. Instead, it does is holds the bitcoin's private key and public address. This 'public address' - a long string of 34 letters and numbers - is also referred to as the "public key." Private keys are strings of characters that control coins--this is what is stored in a crypto wallet. The signature from the private key is what validates the transaction and allows it to go through.

As mentioned, there are two key factors to consider when making a Bitcoin transaction. You need a private key and a public address to send the coins to. Coinbase does, however, hold your private key, so it is not entirely within your control.

This is just something to consider from a security perspective; if you find Coinbase to be a trustworthy entity, then allowing them to keep your private keys in storage shouldn't be an issue. If this is a problem, however, you may want to consider storing your crypto in a way that allows you to have total control over your private keys.

Steps for Sending Funds:

Step 1: Open your software wallet and press the "Send" tab, or use the "Trade|Send Bitcoin" which can be found on your wallet menu.

Step 2: Enter the destination address for your recipient's wallet. This is the public address, add it by copy and pasting it, QR code, or writing it out by hand.

Step 3: Select a label to track your transaction.

Step 4: Enter the amount you’d like transferred in the BTC box.

Step 5: Review the details and make sure the info you entered is correct, as the transaction cannot be reversed.

Step 6: Press "Send" to finalize the transfer.

How to Receive Bitcoin

To receive Bitcoin, you only need your wallet and your public address (as well as your security features to access the wallet obviously).

Step 1: Once you’ve set up your Coinbase account, click the “Accounts” tab. Here and you will find your wallets. Click the “Receive” button on your Bitcoin wallet.

Step 2: The address for your Bitcoin will be displayed. Share this address with anyone who would like to send you Bitcoin.

This occurs due to web trackers and cookies which are pieces of code that track the way sites are used and passed on to third parties. This info can be sent to Google, Facebook, etc. so they can analyze trends. In the same way, governments, law enforcement agencies, and hackers can just as easily gain access to this information.

For this to occur, an eavesdropper or a leaker is required. However, according to a study by Goldfeder, 53/140 Bitcoin merchants have leaked info to a vast number of third parties. This is primarily done for adverts and analytics but is still something to be aware of.

Bybit Uses Tokenised Equities as Underlyings for Structured Yield

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.