Nearly 160 pages detail the FCA's outlook and proposed fee revisions.

Bloomberg

A strategic outlook for the current and following year has been released by the United Kingdom’s Financial Conduct Authority (FCA) today. In the detailed report for 2016/2017, the outlook included an accompanying fee proposal to revise membership-related costs and fees as the regulator is entirely funded via such proceeds from its members including penalties and other member-levied capital.

The two papers, totaling nearly 160 pages, provide an in-depth and highly articulated view of all the key challenges facing the FCA, as well as its current year and 2017 outlook and areas of focus - as it plans to reach its targets during this year and beyond.

Global FX code in development

The outlook noted how the FCA is working with international counterparts to improve conduct in wholesale financial markets at the global level, including how they are structured and operated, as well as supporting the Bank of England and other central banks in their work to develop a global FX code. Finance Magnates reported as that development unfolded last year, and the effort is nearing, but may still be years away from finalization.

...finances and financial literacy have become more varied and complex...

Outlook and fee proposals

FCA acting CEO Tracey McDermott commenting in the press release said: "It is our job to make markets work well. Ensuring effective and proportionate regulation which tackles the problems of the past without inhibiting developments of the future is at the heart of what we do. Over the next year we will continue to embed this sustainable approach to regulation in everything we do.”

Mrs. McDermott added: “The majority of our resources remain devoted to our core business and today we have set out the outcomes we want our work to achieve. Transparency is important to us, and this plan will give all stakeholders an understanding of our focus for the year ahead.”

The regulator said that its operating costs of £502.9 million for 2016/2017 for its ongoing regulatory activities (ORA) had increased by £23.9 million due to the introduction of Consumer Credit into its budget, excluding which would have had reduced its ORA budget to £471.4 million.

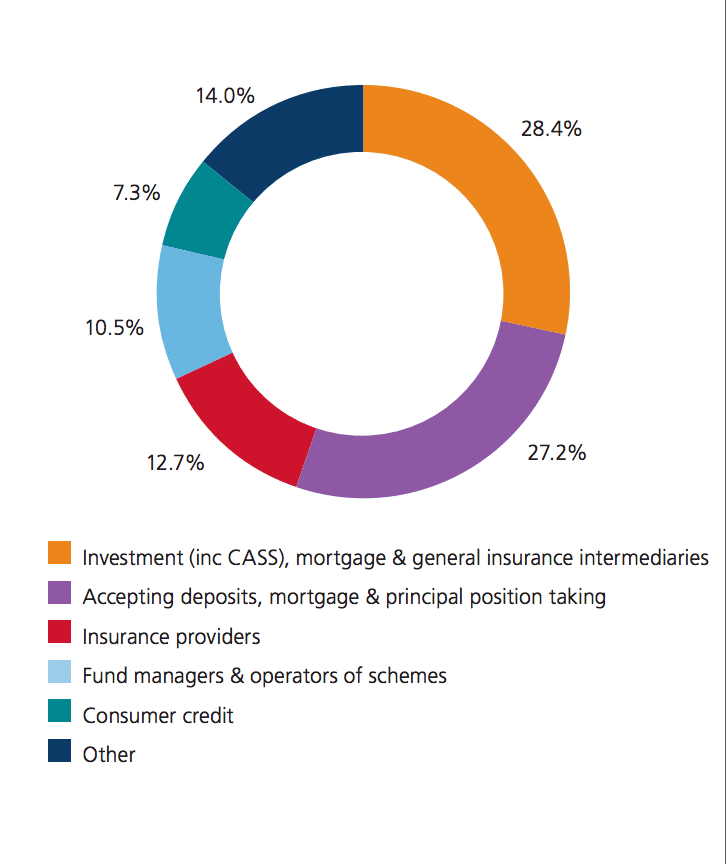

Regarding the fee consultation paper, the pie chart below from the report shows the breakdown of funding by industry.

Source: FCA

The regulator believes that because many providers and companies rely on complex IT infrastructure, a widespread adoption of FinTech solutions would be limited by inherent vulnerabilities in the design and management of new (and existing) systems, unless proper long-term planning is undertaken during the early phases.

FCA added that many providers rely on complex IT systems and infrastructure that make it difficult for them to provide payments or other key services while citing challenges that it anticipates in the future from within FinTech.

FinTech initiatives

The FCA said that it helped 177 companies during the first year of its Project Innovate initiative, and added that its support of RegTech enables more efficient and effective regulation and compliance.

With regard to retail investments, the FCA said that it will complete its thematic review of 'inducements and con flicts of interest' by the end of the second quarter, and that an 'advice' unit will be created to deal with the emergence of robo-advisors or automated advice services.

Data security was an area of focus where the FCA noted how legacy systems had become more complex over time, and the need to balance investment in innovation with maintaining existing systems, as well as lack of IT expertise at the board level, all contributed to the challenge of keeping data secure.

In terms of customer support, the FCA said that finances and financial literacy have become more varied and complex, and the need for appropriate, accessible advice and products is growing, despite the advances in financial technology.

Conflicts of interest and suitability

The FCA explains that in some cases where there is a potential over-reliance on a small number of large clients, or on clients who have a dominant market share, firms could hesitate to report suspicious activity or even misconduct. It also contrasted similar potential conflicts with money managers or investment management firms where conflicts could occur when firms don't prioritize their clients' interests, and added that controls of how client funds are spent may need improvement.

The FCA also expanded on the subject of suitability and referenced how the manner in which client choices are ‘framed’ highly influenced their behavior with choosing services, and cited a 2014 study that it had conducted in this finding.

For example, the FCA observed during an experiment that when an annuity product was framed as an 'investment' (i.e. how much it would cost) rather than from a context of 'consumption' (i.e. how much the investment will return), how investors tended to consistently choose the investment framed products even when the products framed by consumption made better sense financially.

Company culture and market abuse

The FCA is looking at company culture for clues as to firms' practices, as it believes that where there is a strong tradition of standards ingrained within a firm's workforce, such practices trickle down to clients and across product development and administrative responsibilities and other areas that affect clients.

Conversely, firms that have poor culture or governance arrangements that are not aligned with their apparent values or mission statements may have poor customer support and weaker offerings, or even worse potential violations. FCA noted that culture is still a key driver of significant risks in every sector and described it as the root cause of high profile and significant failings.

The Market Abuse Regulation (MAR) was also noted, as the FCA plans on implementing the EU directive during 2016, and expects it to help strengthen the existing UK market abuse framework by including additional markets, and noted the upcoming MiFIR regulation planned for January 2018 that would help aid the MAR implementation.

Fee reductions proposed

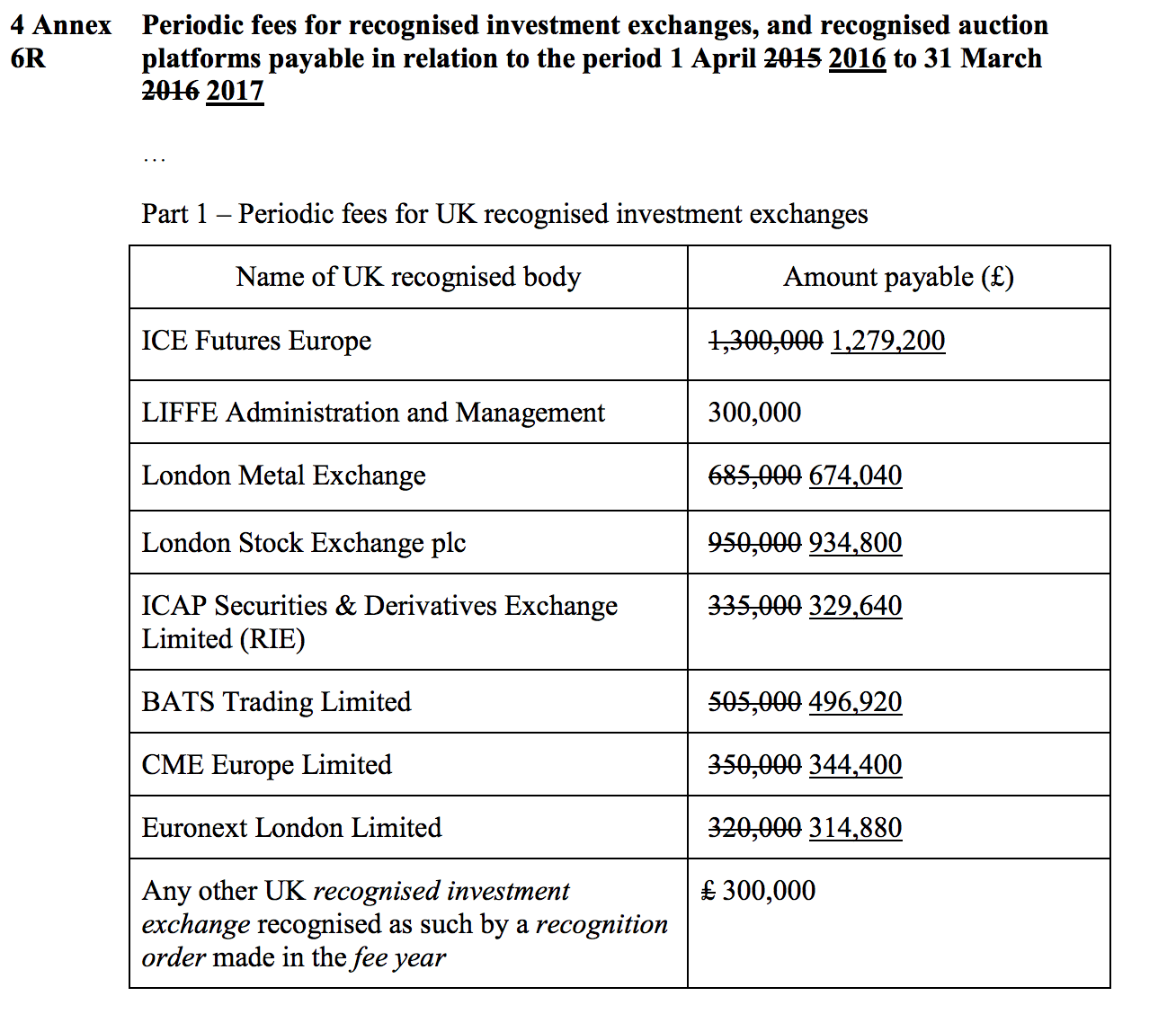

An example of the fee amount that was revised for a number of overseas-based members, such as the Chicago Board of Trade (CBOT), EUREX, Nasdaq, New York Mercantile Exchange (NYMEX), the Swiss Stock Exchange, Sydney Futures Exchange limited, ICE Futures US Inc, and any other over overseas investment exchange registered with the FCA, was lowered by 992 GBP to 61,008 GBP.

Other categories such as the UK-recognized domestic investment exchanges, saw various price reductions depending on the company, as seen in the excerpt from the report below.

Source: FCA

A strategic outlook for the current and following year has been released by the United Kingdom’s Financial Conduct Authority (FCA) today. In the detailed report for 2016/2017, the outlook included an accompanying fee proposal to revise membership-related costs and fees as the regulator is entirely funded via such proceeds from its members including penalties and other member-levied capital.

The two papers, totaling nearly 160 pages, provide an in-depth and highly articulated view of all the key challenges facing the FCA, as well as its current year and 2017 outlook and areas of focus - as it plans to reach its targets during this year and beyond.

Global FX code in development

The outlook noted how the FCA is working with international counterparts to improve conduct in wholesale financial markets at the global level, including how they are structured and operated, as well as supporting the Bank of England and other central banks in their work to develop a global FX code. Finance Magnates reported as that development unfolded last year, and the effort is nearing, but may still be years away from finalization.

...finances and financial literacy have become more varied and complex...

Outlook and fee proposals

FCA acting CEO Tracey McDermott commenting in the press release said: "It is our job to make markets work well. Ensuring effective and proportionate regulation which tackles the problems of the past without inhibiting developments of the future is at the heart of what we do. Over the next year we will continue to embed this sustainable approach to regulation in everything we do.”

Mrs. McDermott added: “The majority of our resources remain devoted to our core business and today we have set out the outcomes we want our work to achieve. Transparency is important to us, and this plan will give all stakeholders an understanding of our focus for the year ahead.”

The regulator said that its operating costs of £502.9 million for 2016/2017 for its ongoing regulatory activities (ORA) had increased by £23.9 million due to the introduction of Consumer Credit into its budget, excluding which would have had reduced its ORA budget to £471.4 million.

Regarding the fee consultation paper, the pie chart below from the report shows the breakdown of funding by industry.

Source: FCA

The regulator believes that because many providers and companies rely on complex IT infrastructure, a widespread adoption of FinTech solutions would be limited by inherent vulnerabilities in the design and management of new (and existing) systems, unless proper long-term planning is undertaken during the early phases.

FCA added that many providers rely on complex IT systems and infrastructure that make it difficult for them to provide payments or other key services while citing challenges that it anticipates in the future from within FinTech.

FinTech initiatives

The FCA said that it helped 177 companies during the first year of its Project Innovate initiative, and added that its support of RegTech enables more efficient and effective regulation and compliance.

With regard to retail investments, the FCA said that it will complete its thematic review of 'inducements and con flicts of interest' by the end of the second quarter, and that an 'advice' unit will be created to deal with the emergence of robo-advisors or automated advice services.

Data security was an area of focus where the FCA noted how legacy systems had become more complex over time, and the need to balance investment in innovation with maintaining existing systems, as well as lack of IT expertise at the board level, all contributed to the challenge of keeping data secure.

In terms of customer support, the FCA said that finances and financial literacy have become more varied and complex, and the need for appropriate, accessible advice and products is growing, despite the advances in financial technology.

Conflicts of interest and suitability

The FCA explains that in some cases where there is a potential over-reliance on a small number of large clients, or on clients who have a dominant market share, firms could hesitate to report suspicious activity or even misconduct. It also contrasted similar potential conflicts with money managers or investment management firms where conflicts could occur when firms don't prioritize their clients' interests, and added that controls of how client funds are spent may need improvement.

The FCA also expanded on the subject of suitability and referenced how the manner in which client choices are ‘framed’ highly influenced their behavior with choosing services, and cited a 2014 study that it had conducted in this finding.

For example, the FCA observed during an experiment that when an annuity product was framed as an 'investment' (i.e. how much it would cost) rather than from a context of 'consumption' (i.e. how much the investment will return), how investors tended to consistently choose the investment framed products even when the products framed by consumption made better sense financially.

Company culture and market abuse

The FCA is looking at company culture for clues as to firms' practices, as it believes that where there is a strong tradition of standards ingrained within a firm's workforce, such practices trickle down to clients and across product development and administrative responsibilities and other areas that affect clients.

Conversely, firms that have poor culture or governance arrangements that are not aligned with their apparent values or mission statements may have poor customer support and weaker offerings, or even worse potential violations. FCA noted that culture is still a key driver of significant risks in every sector and described it as the root cause of high profile and significant failings.

The Market Abuse Regulation (MAR) was also noted, as the FCA plans on implementing the EU directive during 2016, and expects it to help strengthen the existing UK market abuse framework by including additional markets, and noted the upcoming MiFIR regulation planned for January 2018 that would help aid the MAR implementation.

Fee reductions proposed

An example of the fee amount that was revised for a number of overseas-based members, such as the Chicago Board of Trade (CBOT), EUREX, Nasdaq, New York Mercantile Exchange (NYMEX), the Swiss Stock Exchange, Sydney Futures Exchange limited, ICE Futures US Inc, and any other over overseas investment exchange registered with the FCA, was lowered by 992 GBP to 61,008 GBP.

Other categories such as the UK-recognized domestic investment exchanges, saw various price reductions depending on the company, as seen in the excerpt from the report below.

Standard Chartered Executes First Digital Asset Prime Brokerage Trades with LMAX

Featured Videos

Swyft Markets CEO Janeal Delport on Trust, Regulation & Growth in Africa

Swyft Markets CEO Janeal Delport on Trust, Regulation & Growth in Africa

Swyft Markets CEO Janeal Delport on Trust, Regulation & Growth in Africa

Swyft Markets CEO Janeal Delport on Trust, Regulation & Growth in Africa

How do you build a trusted brokerage in one of the world's fastest-growing trading markets?

In this Finance Magnates Executive Interview, Adam Button speaks with Janeal Delport, Chief Executive Officer of Swyft Markets, during the Finance Magnates Africa Summit in Cape Town.

Janeal shares how Swyft Markets is using years of industry experience to build a client-first brokerage, the role of regulation in South Africa's trading industry, and why technology and strong partnerships are key to the company's future.

Topics covered:

- Building trust in the online trading industry

- Swyft Markets' vision and growth strategy

- Regulation and compliance in South Africa

- Technology and trading platform strategy

- The value of partnerships and industry events

- Expansion plans across Africa and international markets

If you're interested in online trading, fintech, brokerage growth, or financial regulation, this interview offers valuable insights from one of the industry's emerging leaders.

📍 Recorded at the Finance Magnates Africa Summit 2026

#FinanceMagnates #SwyftMarkets #OnlineTrading #Forex #CFDTrading #Fintech #Brokerage #SouthAfrica #Trading #FinanceMagnatesAfricaSummit #ExecutiveInterview

How do you build a trusted brokerage in one of the world's fastest-growing trading markets?

In this Finance Magnates Executive Interview, Adam Button speaks with Janeal Delport, Chief Executive Officer of Swyft Markets, during the Finance Magnates Africa Summit in Cape Town.

Janeal shares how Swyft Markets is using years of industry experience to build a client-first brokerage, the role of regulation in South Africa's trading industry, and why technology and strong partnerships are key to the company's future.

Topics covered:

- Building trust in the online trading industry

- Swyft Markets' vision and growth strategy

- Regulation and compliance in South Africa

- Technology and trading platform strategy

- The value of partnerships and industry events

- Expansion plans across Africa and international markets

If you're interested in online trading, fintech, brokerage growth, or financial regulation, this interview offers valuable insights from one of the industry's emerging leaders.

📍 Recorded at the Finance Magnates Africa Summit 2026

#FinanceMagnates #SwyftMarkets #OnlineTrading #Forex #CFDTrading #Fintech #Brokerage #SouthAfrica #Trading #FinanceMagnatesAfricaSummit #ExecutiveInterview

How do you build a trusted brokerage in one of the world's fastest-growing trading markets?

In this Finance Magnates Executive Interview, Adam Button speaks with Janeal Delport, Chief Executive Officer of Swyft Markets, during the Finance Magnates Africa Summit in Cape Town.

Janeal shares how Swyft Markets is using years of industry experience to build a client-first brokerage, the role of regulation in South Africa's trading industry, and why technology and strong partnerships are key to the company's future.

Topics covered:

- Building trust in the online trading industry

- Swyft Markets' vision and growth strategy

- Regulation and compliance in South Africa

- Technology and trading platform strategy

- The value of partnerships and industry events

- Expansion plans across Africa and international markets

If you're interested in online trading, fintech, brokerage growth, or financial regulation, this interview offers valuable insights from one of the industry's emerging leaders.

📍 Recorded at the Finance Magnates Africa Summit 2026

#FinanceMagnates #SwyftMarkets #OnlineTrading #Forex #CFDTrading #Fintech #Brokerage #SouthAfrica #Trading #FinanceMagnatesAfricaSummit #ExecutiveInterview

How do you build a trusted brokerage in one of the world's fastest-growing trading markets?

In this Finance Magnates Executive Interview, Adam Button speaks with Janeal Delport, Chief Executive Officer of Swyft Markets, during the Finance Magnates Africa Summit in Cape Town.

Janeal shares how Swyft Markets is using years of industry experience to build a client-first brokerage, the role of regulation in South Africa's trading industry, and why technology and strong partnerships are key to the company's future.

Topics covered:

- Building trust in the online trading industry

- Swyft Markets' vision and growth strategy

- Regulation and compliance in South Africa

- Technology and trading platform strategy

- The value of partnerships and industry events

- Expansion plans across Africa and international markets

If you're interested in online trading, fintech, brokerage growth, or financial regulation, this interview offers valuable insights from one of the industry's emerging leaders.

📍 Recorded at the Finance Magnates Africa Summit 2026

#FinanceMagnates #SwyftMarkets #OnlineTrading #Forex #CFDTrading #Fintech #Brokerage #SouthAfrica #Trading #FinanceMagnatesAfricaSummit #ExecutiveInterview

Today’s Monday, the 6th of July 2026, and these are our main stories: Vantage launches round-the-clock gold CFD trading, RoboForex brings full trading into Telegram, and Europe is tightening its stance on perpetual futures.

Today’s Monday, the 6th of July 2026, and these are our main stories: Vantage launches round-the-clock gold CFD trading, RoboForex brings full trading into Telegram, and Europe is tightening its stance on perpetual futures.

Today’s Monday, the 6th of July 2026, and these are our main stories: Vantage launches round-the-clock gold CFD trading, RoboForex brings full trading into Telegram, and Europe is tightening its stance on perpetual futures.

Today’s Monday, the 6th of July 2026, and these are our main stories: Vantage launches round-the-clock gold CFD trading, RoboForex brings full trading into Telegram, and Europe is tightening its stance on perpetual futures.

Today’s Monday, the 6th of July 2026, and these are our main stories: Vantage launches round-the-clock gold CFD trading, RoboForex brings full trading into Telegram, and Europe is tightening its stance on perpetual futures.

Today’s Monday, the 6th of July 2026, and these are our main stories: Vantage launches round-the-clock gold CFD trading, RoboForex brings full trading into Telegram, and Europe is tightening its stance on perpetual futures.

The Future of Brokerage Technology: Quadcode on AI, SaaS & Online Trading | Demetris Makrides

The Future of Brokerage Technology: Quadcode on AI, SaaS & Online Trading | Demetris Makrides

The Future of Brokerage Technology: Quadcode on AI, SaaS & Online Trading | Demetris Makrides

The Future of Brokerage Technology: Quadcode on AI, SaaS & Online Trading | Demetris Makrides

The Future of Brokerage Technology: Quadcode on AI, SaaS & Online Trading | Demetris Makrides

The Future of Brokerage Technology: Quadcode on AI, SaaS & Online Trading | Demetris Makrides

How are AI and Software-as-a-Service (SaaS) changing the future of online trading?

In this exclusive Finance Magnates interview, Adonis Adonis, News Editor at Finance Magnates, speaks with Demetris Makrides, Head of Business Development at Quadcode, about the trends shaping the brokerage industry in 2026 and beyond.

They discuss why more brokers are choosing turnkey solutions over building their own technology, how AI is improving trading platforms, and what brokers need to stay competitive in an increasingly crowded market.

In this interview:

✅ What makes Quadcode's brokerage solution different

✅ Why SaaS is becoming the preferred model for brokers

✅ The growing role of AI in online trading

✅ Why user experience is now a competitive advantage

✅ How brokers can launch faster and scale more efficiently

✅ The biggest challenges facing the online trading industry

✅ Quadcode's growth plans and product roadmap

Whether you're launching a brokerage, growing an existing business, or following the latest fintech trends, this interview offers valuable insights into where the industry is heading.

#FinanceMagnates #Quadcode #OnlineTrading #BrokerTechnology #Fintech #CFD #Forex #TradingPlatform #AI #SaaS #Brokerage #BusinessDevelopment

How are AI and Software-as-a-Service (SaaS) changing the future of online trading?

In this exclusive Finance Magnates interview, Adonis Adonis, News Editor at Finance Magnates, speaks with Demetris Makrides, Head of Business Development at Quadcode, about the trends shaping the brokerage industry in 2026 and beyond.

They discuss why more brokers are choosing turnkey solutions over building their own technology, how AI is improving trading platforms, and what brokers need to stay competitive in an increasingly crowded market.

In this interview:

✅ What makes Quadcode's brokerage solution different

✅ Why SaaS is becoming the preferred model for brokers

✅ The growing role of AI in online trading

✅ Why user experience is now a competitive advantage

✅ How brokers can launch faster and scale more efficiently

✅ The biggest challenges facing the online trading industry

✅ Quadcode's growth plans and product roadmap

Whether you're launching a brokerage, growing an existing business, or following the latest fintech trends, this interview offers valuable insights into where the industry is heading.

#FinanceMagnates #Quadcode #OnlineTrading #BrokerTechnology #Fintech #CFD #Forex #TradingPlatform #AI #SaaS #Brokerage #BusinessDevelopment

How are AI and Software-as-a-Service (SaaS) changing the future of online trading?

In this exclusive Finance Magnates interview, Adonis Adonis, News Editor at Finance Magnates, speaks with Demetris Makrides, Head of Business Development at Quadcode, about the trends shaping the brokerage industry in 2026 and beyond.

They discuss why more brokers are choosing turnkey solutions over building their own technology, how AI is improving trading platforms, and what brokers need to stay competitive in an increasingly crowded market.

In this interview:

✅ What makes Quadcode's brokerage solution different

✅ Why SaaS is becoming the preferred model for brokers

✅ The growing role of AI in online trading

✅ Why user experience is now a competitive advantage

✅ How brokers can launch faster and scale more efficiently

✅ The biggest challenges facing the online trading industry

✅ Quadcode's growth plans and product roadmap

Whether you're launching a brokerage, growing an existing business, or following the latest fintech trends, this interview offers valuable insights into where the industry is heading.

#FinanceMagnates #Quadcode #OnlineTrading #BrokerTechnology #Fintech #CFD #Forex #TradingPlatform #AI #SaaS #Brokerage #BusinessDevelopment

How are AI and Software-as-a-Service (SaaS) changing the future of online trading?

In this exclusive Finance Magnates interview, Adonis Adonis, News Editor at Finance Magnates, speaks with Demetris Makrides, Head of Business Development at Quadcode, about the trends shaping the brokerage industry in 2026 and beyond.

They discuss why more brokers are choosing turnkey solutions over building their own technology, how AI is improving trading platforms, and what brokers need to stay competitive in an increasingly crowded market.

In this interview:

✅ What makes Quadcode's brokerage solution different

✅ Why SaaS is becoming the preferred model for brokers

✅ The growing role of AI in online trading

✅ Why user experience is now a competitive advantage

✅ How brokers can launch faster and scale more efficiently

✅ The biggest challenges facing the online trading industry

✅ Quadcode's growth plans and product roadmap

Whether you're launching a brokerage, growing an existing business, or following the latest fintech trends, this interview offers valuable insights into where the industry is heading.

#FinanceMagnates #Quadcode #OnlineTrading #BrokerTechnology #Fintech #CFD #Forex #TradingPlatform #AI #SaaS #Brokerage #BusinessDevelopment

How are AI and Software-as-a-Service (SaaS) changing the future of online trading?

In this exclusive Finance Magnates interview, Adonis Adonis, News Editor at Finance Magnates, speaks with Demetris Makrides, Head of Business Development at Quadcode, about the trends shaping the brokerage industry in 2026 and beyond.

They discuss why more brokers are choosing turnkey solutions over building their own technology, how AI is improving trading platforms, and what brokers need to stay competitive in an increasingly crowded market.

In this interview:

✅ What makes Quadcode's brokerage solution different

✅ Why SaaS is becoming the preferred model for brokers

✅ The growing role of AI in online trading

✅ Why user experience is now a competitive advantage

✅ How brokers can launch faster and scale more efficiently

✅ The biggest challenges facing the online trading industry

✅ Quadcode's growth plans and product roadmap

Whether you're launching a brokerage, growing an existing business, or following the latest fintech trends, this interview offers valuable insights into where the industry is heading.

#FinanceMagnates #Quadcode #OnlineTrading #BrokerTechnology #Fintech #CFD #Forex #TradingPlatform #AI #SaaS #Brokerage #BusinessDevelopment

How are AI and Software-as-a-Service (SaaS) changing the future of online trading?

In this exclusive Finance Magnates interview, Adonis Adonis, News Editor at Finance Magnates, speaks with Demetris Makrides, Head of Business Development at Quadcode, about the trends shaping the brokerage industry in 2026 and beyond.

They discuss why more brokers are choosing turnkey solutions over building their own technology, how AI is improving trading platforms, and what brokers need to stay competitive in an increasingly crowded market.

In this interview:

✅ What makes Quadcode's brokerage solution different

✅ Why SaaS is becoming the preferred model for brokers

✅ The growing role of AI in online trading

✅ Why user experience is now a competitive advantage

✅ How brokers can launch faster and scale more efficiently

✅ The biggest challenges facing the online trading industry

✅ Quadcode's growth plans and product roadmap

Whether you're launching a brokerage, growing an existing business, or following the latest fintech trends, this interview offers valuable insights into where the industry is heading.

#FinanceMagnates #Quadcode #OnlineTrading #BrokerTechnology #Fintech #CFD #Forex #TradingPlatform #AI #SaaS #Brokerage #BusinessDevelopment

FM Daily Brief – 3 July 2026

FM Daily Brief – 3 July 2026

FM Daily Brief – 3 July 2026

FM Daily Brief – 3 July 2026

FM Daily Brief – 3 July 2026

FM Daily Brief – 3 July 2026

Today’s Friday, the 3rd of July 2026, and these are our main stories: Esma warns that prediction markets may still fall under the EU’s binary options ban, prediction markets surpass 50 billion dollars in monthly trading volume and brokers rethink client engagement in a tougher regulatory landscape.

Today’s Friday, the 3rd of July 2026, and these are our main stories: Esma warns that prediction markets may still fall under the EU’s binary options ban, prediction markets surpass 50 billion dollars in monthly trading volume and brokers rethink client engagement in a tougher regulatory landscape.

Today’s Friday, the 3rd of July 2026, and these are our main stories: Esma warns that prediction markets may still fall under the EU’s binary options ban, prediction markets surpass 50 billion dollars in monthly trading volume and brokers rethink client engagement in a tougher regulatory landscape.

Today’s Friday, the 3rd of July 2026, and these are our main stories: Esma warns that prediction markets may still fall under the EU’s binary options ban, prediction markets surpass 50 billion dollars in monthly trading volume and brokers rethink client engagement in a tougher regulatory landscape.

Today’s Friday, the 3rd of July 2026, and these are our main stories: Esma warns that prediction markets may still fall under the EU’s binary options ban, prediction markets surpass 50 billion dollars in monthly trading volume and brokers rethink client engagement in a tougher regulatory landscape.

Today’s Friday, the 3rd of July 2026, and these are our main stories: Esma warns that prediction markets may still fall under the EU’s binary options ban, prediction markets surpass 50 billion dollars in monthly trading volume and brokers rethink client engagement in a tougher regulatory landscape.

Why FX Brokers Lose Deposits: SPAYZ.io CCO on Payments, Conversion & Emerging Markets

Why FX Brokers Lose Deposits: SPAYZ.io CCO on Payments, Conversion & Emerging Markets

Why FX Brokers Lose Deposits: SPAYZ.io CCO on Payments, Conversion & Emerging Markets

Why FX Brokers Lose Deposits: SPAYZ.io CCO on Payments, Conversion & Emerging Markets

Why FX Brokers Lose Deposits: SPAYZ.io CCO on Payments, Conversion & Emerging Markets

Why FX Brokers Lose Deposits: SPAYZ.io CCO on Payments, Conversion & Emerging Markets

Are your payment flows costing you clients?

At iFX EXPO International, Finance Magnates' Editor-in-Chief Yam Yehoshua speaks with Tatjana Meluskane, Chief Commercial Officer at SPAYZ.io, about why payment strategy has become one of the biggest drivers of broker growth.

In this interview, Tatjana explains why local payment methods, regional expertise, and close cooperation between brokers and payment providers are essential for improving deposit conversion rates and expanding into emerging markets.

In this interview:

- Why brokers lose deposits before clients even start trading

- The importance of local payment methods and local currencies

- Why card payments often fail in emerging markets

- Mobile money, QR payments, and regional payment preferences

- How brokers can improve payment conversion rates

- The role of analytics in payment optimisation

- Why payment success is a shared responsibility between brokers and PSPs

- The value of long-term partnerships in global payments

Key Quote:

"Everything starts with partnership... We are focusing on growth through partnerships, close cooperation, fast reaction, improvements and developments." — Tatjana Meluskane, Chief Commercial Officer, SPAYZ.io

If you're a broker, fintech company, payment provider, or industry professional looking to improve client deposits and payment performance, this interview is packed with practical insights.

#FinanceMagnates #iFXEXPO #Forex #Payments #Fintech #Brokers #PSP #PaymentGateway #Trading #FX #EmergingMarkets #SPAYZ #ConversionRate #PaymentMethods

Are your payment flows costing you clients?

At iFX EXPO International, Finance Magnates' Editor-in-Chief Yam Yehoshua speaks with Tatjana Meluskane, Chief Commercial Officer at SPAYZ.io, about why payment strategy has become one of the biggest drivers of broker growth.

In this interview, Tatjana explains why local payment methods, regional expertise, and close cooperation between brokers and payment providers are essential for improving deposit conversion rates and expanding into emerging markets.

In this interview:

- Why brokers lose deposits before clients even start trading

- The importance of local payment methods and local currencies

- Why card payments often fail in emerging markets

- Mobile money, QR payments, and regional payment preferences

- How brokers can improve payment conversion rates

- The role of analytics in payment optimisation

- Why payment success is a shared responsibility between brokers and PSPs

- The value of long-term partnerships in global payments

Key Quote:

"Everything starts with partnership... We are focusing on growth through partnerships, close cooperation, fast reaction, improvements and developments." — Tatjana Meluskane, Chief Commercial Officer, SPAYZ.io

If you're a broker, fintech company, payment provider, or industry professional looking to improve client deposits and payment performance, this interview is packed with practical insights.

#FinanceMagnates #iFXEXPO #Forex #Payments #Fintech #Brokers #PSP #PaymentGateway #Trading #FX #EmergingMarkets #SPAYZ #ConversionRate #PaymentMethods

Are your payment flows costing you clients?

At iFX EXPO International, Finance Magnates' Editor-in-Chief Yam Yehoshua speaks with Tatjana Meluskane, Chief Commercial Officer at SPAYZ.io, about why payment strategy has become one of the biggest drivers of broker growth.

In this interview, Tatjana explains why local payment methods, regional expertise, and close cooperation between brokers and payment providers are essential for improving deposit conversion rates and expanding into emerging markets.

In this interview:

- Why brokers lose deposits before clients even start trading

- The importance of local payment methods and local currencies

- Why card payments often fail in emerging markets

- Mobile money, QR payments, and regional payment preferences

- How brokers can improve payment conversion rates

- The role of analytics in payment optimisation

- Why payment success is a shared responsibility between brokers and PSPs

- The value of long-term partnerships in global payments

Key Quote:

"Everything starts with partnership... We are focusing on growth through partnerships, close cooperation, fast reaction, improvements and developments." — Tatjana Meluskane, Chief Commercial Officer, SPAYZ.io

If you're a broker, fintech company, payment provider, or industry professional looking to improve client deposits and payment performance, this interview is packed with practical insights.

#FinanceMagnates #iFXEXPO #Forex #Payments #Fintech #Brokers #PSP #PaymentGateway #Trading #FX #EmergingMarkets #SPAYZ #ConversionRate #PaymentMethods

Are your payment flows costing you clients?

At iFX EXPO International, Finance Magnates' Editor-in-Chief Yam Yehoshua speaks with Tatjana Meluskane, Chief Commercial Officer at SPAYZ.io, about why payment strategy has become one of the biggest drivers of broker growth.

In this interview, Tatjana explains why local payment methods, regional expertise, and close cooperation between brokers and payment providers are essential for improving deposit conversion rates and expanding into emerging markets.

In this interview:

- Why brokers lose deposits before clients even start trading

- The importance of local payment methods and local currencies

- Why card payments often fail in emerging markets

- Mobile money, QR payments, and regional payment preferences

- How brokers can improve payment conversion rates

- The role of analytics in payment optimisation

- Why payment success is a shared responsibility between brokers and PSPs

- The value of long-term partnerships in global payments

Key Quote:

"Everything starts with partnership... We are focusing on growth through partnerships, close cooperation, fast reaction, improvements and developments." — Tatjana Meluskane, Chief Commercial Officer, SPAYZ.io

If you're a broker, fintech company, payment provider, or industry professional looking to improve client deposits and payment performance, this interview is packed with practical insights.

#FinanceMagnates #iFXEXPO #Forex #Payments #Fintech #Brokers #PSP #PaymentGateway #Trading #FX #EmergingMarkets #SPAYZ #ConversionRate #PaymentMethods

Are your payment flows costing you clients?

At iFX EXPO International, Finance Magnates' Editor-in-Chief Yam Yehoshua speaks with Tatjana Meluskane, Chief Commercial Officer at SPAYZ.io, about why payment strategy has become one of the biggest drivers of broker growth.

In this interview, Tatjana explains why local payment methods, regional expertise, and close cooperation between brokers and payment providers are essential for improving deposit conversion rates and expanding into emerging markets.

In this interview:

- Why brokers lose deposits before clients even start trading

- The importance of local payment methods and local currencies

- Why card payments often fail in emerging markets

- Mobile money, QR payments, and regional payment preferences

- How brokers can improve payment conversion rates

- The role of analytics in payment optimisation

- Why payment success is a shared responsibility between brokers and PSPs

- The value of long-term partnerships in global payments

Key Quote:

"Everything starts with partnership... We are focusing on growth through partnerships, close cooperation, fast reaction, improvements and developments." — Tatjana Meluskane, Chief Commercial Officer, SPAYZ.io

If you're a broker, fintech company, payment provider, or industry professional looking to improve client deposits and payment performance, this interview is packed with practical insights.

#FinanceMagnates #iFXEXPO #Forex #Payments #Fintech #Brokers #PSP #PaymentGateway #Trading #FX #EmergingMarkets #SPAYZ #ConversionRate #PaymentMethods

Are your payment flows costing you clients?

At iFX EXPO International, Finance Magnates' Editor-in-Chief Yam Yehoshua speaks with Tatjana Meluskane, Chief Commercial Officer at SPAYZ.io, about why payment strategy has become one of the biggest drivers of broker growth.

In this interview, Tatjana explains why local payment methods, regional expertise, and close cooperation between brokers and payment providers are essential for improving deposit conversion rates and expanding into emerging markets.

In this interview:

- Why brokers lose deposits before clients even start trading

- The importance of local payment methods and local currencies

- Why card payments often fail in emerging markets

- Mobile money, QR payments, and regional payment preferences

- How brokers can improve payment conversion rates

- The role of analytics in payment optimisation

- Why payment success is a shared responsibility between brokers and PSPs

- The value of long-term partnerships in global payments

Key Quote:

"Everything starts with partnership... We are focusing on growth through partnerships, close cooperation, fast reaction, improvements and developments." — Tatjana Meluskane, Chief Commercial Officer, SPAYZ.io

If you're a broker, fintech company, payment provider, or industry professional looking to improve client deposits and payment performance, this interview is packed with practical insights.

#FinanceMagnates #iFXEXPO #Forex #Payments #Fintech #Brokers #PSP #PaymentGateway #Trading #FX #EmergingMarkets #SPAYZ #ConversionRate #PaymentMethods