CLS Bank has posted March trading data of trades submitted to the bank for settlement. During the month, average trading volumes (ADV) was $5.16 trillion, down 0.2% from February’s $5.17 trillion level. The ADV of trades sent to the bank were 1,217,817, nearly 10.0% below February’s figures, signaling larger average trade sizes.

(Total volumes include FX Spot, Forwards, Swaps , and NDF trades. In addition, CLS Bank figures reflect reporting of both sides of a trade. Therefore, volume figures need to be divided by two to equate with the BIS’s trade calculations.)

The figures contrast well with those of EBS which showed a 19% decline in month over month trading. Looking ahead, we should soon see volume numbers from Thomson Reuters, FXall, and Hotspot FX, which will provide a better glimpse of whether the CLS data represented an outperformance of single dealer platform trading versus activity on ECNs.

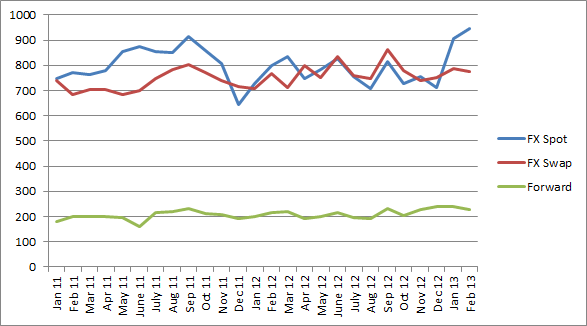

In their more in-depth analysis (available through February 2013’s volume), CLS bank reports show that FX Spot trading has been outperforming FX Swap volumes during 2013 (see chart below). Similar to activity that took place in 2011, Spot trading is benefitting from an increase in volatilities, while Swap activity has more or less remained stable since January 2011. (For more information on the CLS Bank, Forex Magnates will be publishing an in-depth look at the groups activities and their role in FX trading in our upcoming Forex Industry Quarterly Report due out later this month)

CLS ADV Since January 2011 (According to BIS accounting)