Two regulated stock exchanges with a combined market-share of nearly 20% of the US stock market volumes got regulatory approval from the Securities and Exchange Commission to merge, deal is expected to close within days.

Further exchange consolidation underway with the latest approval announced for two leading US stock market operators including BATS Global Markets Inc, and Direct Edge Holdings LLC to merge, with a green light from the Securities and Exchange Commission (SEC).

The two exchange operators each had a respective market share greater than 10% of daily trading volumes in the US Stock Markets as of December 2013. The deal now approved by the SEC is set to close within days, according to the company’s latest press release, and will result in a total of four stock exchanges under the new emerging group entity.

The Kansas City-based operator of two exchanges including BZX and BZY, and the Market Participant Identifiers (MPID) BATS, BATY and BATM, as a destination venue for exchange-traded order-flow, run by BATS Global Markets, announced the planned merger last August with Direct Edge -the indirect parent company of Direct Edge ECN, under the MPIDs EDGE, EDGA and EDGX, that will now combine to account for some 20% of total market share of US stock market traded volumes -across a total of the four nationally regulated securities exchanges.

According to recent regulatory filings with the SEC in December, upon completion of the merger, BATS Global Markets, Inc. and Direct Edge Holdings will each become intermediate holding companies, held under a single new holding company. The new holding company, currently named “BATS Global Markets Holdings, Inc.” at the time of the merger closing will change its name to “BATS Global Markets."

Merger Creates Leading Market Share Position for New Group Emerging

Joe Ratterman, CEO of BATS Global Markets

Commenting in the official press release, jointly released, Joe Ratterman, CEO of BATS Global Markets said, “With the final regulatory approval received, we are focused on closing the merger during the current quarter and beginning the integration of our two highly complementary companies.”

Considering the firms have only been registered as national securities exchanges for barely more than a few years for the securities and options designations, when compared to for example to the NYSE which is one of the largest stock exchange globally and founded nearly 200 years ago, it's amazing how quickly these alternative venues have become such a primary option for much of the entire market's trading flows.

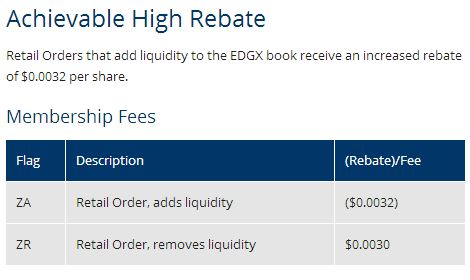

Rebates a Key Differentiator of Exchange Destination Choice for Brokers

The subject of the exchange fee model and 4 different market-making and agency model types have been under the microscope by global regulators, according to a recent IOSCO report that aimed to compare the various pricing models surrounding price discovery/execution and any affect it had on market participants as well as market prices.

Excerpt of Rebate example from Direct Edge

While the report concluded with mix views, the benefits and/or challenges resulting from the current market infrastructure's stage of evolution (in terms of the execution space), is an inevitable result of a multitude of drivers in its natural progression, using for example the current state of the U.S. Stock Markets execution space.

The microstructure of the exchange-traded securities market in the US, as well as the dark pool or off-exchange transactions that get printed to consolidated exchange tapes, have all been the subject of debate, and the US remains one of the most sophisticated market places when it comes to the executing broker space, whether firms are proprietary trading for their own account or as principal to their clients' trades as a broker-dealer, or when acting as an Agent in an agency model or in the case of when firms can do both.

Exchange fees are considered pass-through costs, as when broker-dealers route flow these fees are applied whether a net-credit or net-debit, the fees are either passed through to end-brokerage firms originating the flow, or are something the broker-dealer realizes depending on the execution agreement and cost structure. Accordingly, the routing of flow will not only depend (primarily and most importantly) on best price (under NBBO) but also taking into considerations costs/savings via various exchange fee structures.

Internalizing and Facilitating Order Flow Under Best Execution

The FX space is far more simple in this regard, and that could change in the distant future as FX becomes more centralized or at least –in the shorter-term – if the processes surrounding price discovery and order execution change as a result of new rules imposed after regulator's investigation of major cases of FX rate manipulation.

In the case of the US stock markets, the question of best execution is one element under debate along with the effects of algorithmic trading, whether it creates an unfair advantage or if an algo-gone-wild could wreak havoc on an orderly functioning marketplace.

As trading models become more sophisticated, and order flow routed intelligently to the venue that can provide the best price under NBBO along with an incentive inducing rebate or lower cost of fees to be paid, a process that was once manual is not almost entirely program driven or automated.

Competing Prices Driving Down Costs

When an online broker signs an execution agreement with a broker-dealer and clearing and settlement routes are arranged (with proper clearing agreements in place), whether domestic or internationally (including any delivery versus payment -DVP - used for non-local transaction), orders can be routed electronically via FIX API and/or through a 3rd party OMS/EMS (like Bloomberg EMSx, Sungard, Fidessa,etc.) and the executing broker can decide where to send the flow unless the venue has already been directed by the online broker in advance.

In the end, execution costs have come down considerably as the competition across venues with regards to rebates/fee schedules have competed fiercely on price – down even a hundred of a penny or less – in order to attract significant flows, and this has resulted in lower costs passed on to from executing brokers to the online firms, and in some cases the online brokerages to their end-user traders.

For BATS and Direct Edge this model appears to have worked well, and other such exchanges have also shifted to adjust their respective fee schedules in recent years and this pricing model emerged.

William O’Brien, CEO of Direct Edge

Commenting in the official press release, William O’Brien, CEO of Direct Edge, said, “We are pleased to reach this important milestone and look forward to leveraging the best-in-class offerings and unique resources from both organizations as we continue to work in partnership with our customers.”

According to the deal, upon closing Mr. Ratterman will continue in his role as CEO of BATS Global Markets and Mr. O’Brien will be President. The combined company will remain headquartered in the Kansas City, Mo., area and continue to operate all four existing U.S. equities markets currently run by BATS and Direct Edge -- the BATS’ BZX and BYX Exchanges and Direct Edge’s EDGX and EDGA Exchanges, as per the press release. The technology integration will include the transition of the Direct Edge equities exchanges to the proprietary BATS technology platform.

The BATS exchanges are each Delaware corporations that are national securities exchanges registered with the SEC pursuant to Section 6(a) of section 15 U.S.C. 78f(a).

In reviewing the details of the merger the SEC considered the owners and shareholders of the entities involved including the size of their interests and connections to affiliate companies in the securities space, as well as any undue burden to competition that could result.

SEC Looks at Exchange Ownership/ Relation to Brokerage Affiliates

According to the December SEC rule filing request, each BATS Exchange is a direct, wholly owned subsidiary of Current BGM, a Delaware corporation. Current BGM also owns 100 percent of the equity interest in BATS Trading, Inc., a Delaware corporation (“BATS Trading”) that is a broker-dealer registered with the Commission that provides routing services outbound from and, in certain instances inbound to, each BATS Exchange.

BGM was noted as then currently beneficially owned primarily by a consortium of several unaffiliated firms, including Members or affiliates of Members of the Exchange. No firm beneficially owns 20 percent or greater of Current BGM, and the only firms beneficially owning ten percent or greater of Current BGM are GETCO Investments, LLC, an affiliate of KCG Holdings, Inc., BGM Holding, L.P., a holding company itself owned by entities affiliated with the Spectrum Equity Investors and TA Associates Management private investment funds, and Strategic Investments I, Inc., an affiliate of Morgan Stanley, according to the filing. Seven other firms each beneficially own five percent or greater but less than ten percent of Current BGM, noted the filings, while seven other firms as well as various individuals each beneficially own less than five percent of Current BGM.

Direct Edge Holdings, a Delaware limited liability company, owns 100 percent of the equity interest in Direct Edge, Inc., a Delaware corporation (“DEI”). DEI, in turn, owns 100 percent of the equity interest in two registered national securities exchanges, EDGX and EDGA, each a Delaware corporation (together, the “DE Exchanges”). In addition, DE Holdings owns 100 percent of the equity interest in Direct Edge ECN LLC d/b/a DE Route, a Delaware limited liability company and the routing broker-dealer for the DE Exchanges (“DE Route”), described in an excerpt of the filing. The full copy is available on the SEC website.

SEC Gets Quantitative with Data

The SEC recently rolled out Market Information Data Analytic System (MIDAS), following events such as the flash-crash, in order to better understand the multitude of steps and events that take place in very small fractions of a second, where so many transactions take place day-to-day.

The merger approval is a significant milestone for the alternative market trading space, and indicative of the current stage of the evolution of the execution space and exchange micro-structure being embraced from an important side of the industry (The regulatory side).

A chart excerpt below compares certain trade ratios provided by the SEC MIDAS tools, with the four exchanges mentioned in the above merger deal, as a comparison, one of several available data set the cancel to trade is made up of the # of cancels divided by the # of trades:

CTT Ratio example from SEC MIDAS tool [source: SEC]

In the SEC latest annual report, it said it continued to work with exchanges and FINRA as they developed the market-wide consolidated audit trail required by Commission rules, which will significantly enhance their collective ability to monitor and analyze trading activity, according to SEC published document.

Separately, the agency noted that it brought MIDAS on line, providing the SEC with immediate new capabilities based on access to all of the real-time data feeds made available to market participants by the exchanges, and said it developed an initial set of data analysis that directly informs on market structure policy questions. Finally, the tool was said to have generated data that led to a number of investigations, exams and analyses, that had been launched, as the regulator got quantitative with the market data of trade executions.

A full copy of the press release regarding the merger approval can be found on the BATS and Direct Edge corporate websites.

Further exchange consolidation underway with the latest approval announced for two leading US stock market operators including BATS Global Markets Inc, and Direct Edge Holdings LLC to merge, with a green light from the Securities and Exchange Commission (SEC).

The two exchange operators each had a respective market share greater than 10% of daily trading volumes in the US Stock Markets as of December 2013. The deal now approved by the SEC is set to close within days, according to the company’s latest press release, and will result in a total of four stock exchanges under the new emerging group entity.

The Kansas City-based operator of two exchanges including BZX and BZY, and the Market Participant Identifiers (MPID) BATS, BATY and BATM, as a destination venue for exchange-traded order-flow, run by BATS Global Markets, announced the planned merger last August with Direct Edge -the indirect parent company of Direct Edge ECN, under the MPIDs EDGE, EDGA and EDGX, that will now combine to account for some 20% of total market share of US stock market traded volumes -across a total of the four nationally regulated securities exchanges.

According to recent regulatory filings with the SEC in December, upon completion of the merger, BATS Global Markets, Inc. and Direct Edge Holdings will each become intermediate holding companies, held under a single new holding company. The new holding company, currently named “BATS Global Markets Holdings, Inc.” at the time of the merger closing will change its name to “BATS Global Markets."

Merger Creates Leading Market Share Position for New Group Emerging

Joe Ratterman, CEO of BATS Global Markets

Commenting in the official press release, jointly released, Joe Ratterman, CEO of BATS Global Markets said, “With the final regulatory approval received, we are focused on closing the merger during the current quarter and beginning the integration of our two highly complementary companies.”

Considering the firms have only been registered as national securities exchanges for barely more than a few years for the securities and options designations, when compared to for example to the NYSE which is one of the largest stock exchange globally and founded nearly 200 years ago, it's amazing how quickly these alternative venues have become such a primary option for much of the entire market's trading flows.

Rebates a Key Differentiator of Exchange Destination Choice for Brokers

The subject of the exchange fee model and 4 different market-making and agency model types have been under the microscope by global regulators, according to a recent IOSCO report that aimed to compare the various pricing models surrounding price discovery/execution and any affect it had on market participants as well as market prices.

Excerpt of Rebate example from Direct Edge

While the report concluded with mix views, the benefits and/or challenges resulting from the current market infrastructure's stage of evolution (in terms of the execution space), is an inevitable result of a multitude of drivers in its natural progression, using for example the current state of the U.S. Stock Markets execution space.

The microstructure of the exchange-traded securities market in the US, as well as the dark pool or off-exchange transactions that get printed to consolidated exchange tapes, have all been the subject of debate, and the US remains one of the most sophisticated market places when it comes to the executing broker space, whether firms are proprietary trading for their own account or as principal to their clients' trades as a broker-dealer, or when acting as an Agent in an agency model or in the case of when firms can do both.

Exchange fees are considered pass-through costs, as when broker-dealers route flow these fees are applied whether a net-credit or net-debit, the fees are either passed through to end-brokerage firms originating the flow, or are something the broker-dealer realizes depending on the execution agreement and cost structure. Accordingly, the routing of flow will not only depend (primarily and most importantly) on best price (under NBBO) but also taking into considerations costs/savings via various exchange fee structures.

Internalizing and Facilitating Order Flow Under Best Execution

The FX space is far more simple in this regard, and that could change in the distant future as FX becomes more centralized or at least –in the shorter-term – if the processes surrounding price discovery and order execution change as a result of new rules imposed after regulator's investigation of major cases of FX rate manipulation.

In the case of the US stock markets, the question of best execution is one element under debate along with the effects of algorithmic trading, whether it creates an unfair advantage or if an algo-gone-wild could wreak havoc on an orderly functioning marketplace.

As trading models become more sophisticated, and order flow routed intelligently to the venue that can provide the best price under NBBO along with an incentive inducing rebate or lower cost of fees to be paid, a process that was once manual is not almost entirely program driven or automated.

Competing Prices Driving Down Costs

When an online broker signs an execution agreement with a broker-dealer and clearing and settlement routes are arranged (with proper clearing agreements in place), whether domestic or internationally (including any delivery versus payment -DVP - used for non-local transaction), orders can be routed electronically via FIX API and/or through a 3rd party OMS/EMS (like Bloomberg EMSx, Sungard, Fidessa,etc.) and the executing broker can decide where to send the flow unless the venue has already been directed by the online broker in advance.

In the end, execution costs have come down considerably as the competition across venues with regards to rebates/fee schedules have competed fiercely on price – down even a hundred of a penny or less – in order to attract significant flows, and this has resulted in lower costs passed on to from executing brokers to the online firms, and in some cases the online brokerages to their end-user traders.

For BATS and Direct Edge this model appears to have worked well, and other such exchanges have also shifted to adjust their respective fee schedules in recent years and this pricing model emerged.

William O’Brien, CEO of Direct Edge

Commenting in the official press release, William O’Brien, CEO of Direct Edge, said, “We are pleased to reach this important milestone and look forward to leveraging the best-in-class offerings and unique resources from both organizations as we continue to work in partnership with our customers.”

According to the deal, upon closing Mr. Ratterman will continue in his role as CEO of BATS Global Markets and Mr. O’Brien will be President. The combined company will remain headquartered in the Kansas City, Mo., area and continue to operate all four existing U.S. equities markets currently run by BATS and Direct Edge -- the BATS’ BZX and BYX Exchanges and Direct Edge’s EDGX and EDGA Exchanges, as per the press release. The technology integration will include the transition of the Direct Edge equities exchanges to the proprietary BATS technology platform.

The BATS exchanges are each Delaware corporations that are national securities exchanges registered with the SEC pursuant to Section 6(a) of section 15 U.S.C. 78f(a).

In reviewing the details of the merger the SEC considered the owners and shareholders of the entities involved including the size of their interests and connections to affiliate companies in the securities space, as well as any undue burden to competition that could result.

SEC Looks at Exchange Ownership/ Relation to Brokerage Affiliates

According to the December SEC rule filing request, each BATS Exchange is a direct, wholly owned subsidiary of Current BGM, a Delaware corporation. Current BGM also owns 100 percent of the equity interest in BATS Trading, Inc., a Delaware corporation (“BATS Trading”) that is a broker-dealer registered with the Commission that provides routing services outbound from and, in certain instances inbound to, each BATS Exchange.

BGM was noted as then currently beneficially owned primarily by a consortium of several unaffiliated firms, including Members or affiliates of Members of the Exchange. No firm beneficially owns 20 percent or greater of Current BGM, and the only firms beneficially owning ten percent or greater of Current BGM are GETCO Investments, LLC, an affiliate of KCG Holdings, Inc., BGM Holding, L.P., a holding company itself owned by entities affiliated with the Spectrum Equity Investors and TA Associates Management private investment funds, and Strategic Investments I, Inc., an affiliate of Morgan Stanley, according to the filing. Seven other firms each beneficially own five percent or greater but less than ten percent of Current BGM, noted the filings, while seven other firms as well as various individuals each beneficially own less than five percent of Current BGM.

Direct Edge Holdings, a Delaware limited liability company, owns 100 percent of the equity interest in Direct Edge, Inc., a Delaware corporation (“DEI”). DEI, in turn, owns 100 percent of the equity interest in two registered national securities exchanges, EDGX and EDGA, each a Delaware corporation (together, the “DE Exchanges”). In addition, DE Holdings owns 100 percent of the equity interest in Direct Edge ECN LLC d/b/a DE Route, a Delaware limited liability company and the routing broker-dealer for the DE Exchanges (“DE Route”), described in an excerpt of the filing. The full copy is available on the SEC website.

SEC Gets Quantitative with Data

The SEC recently rolled out Market Information Data Analytic System (MIDAS), following events such as the flash-crash, in order to better understand the multitude of steps and events that take place in very small fractions of a second, where so many transactions take place day-to-day.

The merger approval is a significant milestone for the alternative market trading space, and indicative of the current stage of the evolution of the execution space and exchange micro-structure being embraced from an important side of the industry (The regulatory side).

A chart excerpt below compares certain trade ratios provided by the SEC MIDAS tools, with the four exchanges mentioned in the above merger deal, as a comparison, one of several available data set the cancel to trade is made up of the # of cancels divided by the # of trades:

CTT Ratio example from SEC MIDAS tool [source: SEC]

In the SEC latest annual report, it said it continued to work with exchanges and FINRA as they developed the market-wide consolidated audit trail required by Commission rules, which will significantly enhance their collective ability to monitor and analyze trading activity, according to SEC published document.

Separately, the agency noted that it brought MIDAS on line, providing the SEC with immediate new capabilities based on access to all of the real-time data feeds made available to market participants by the exchanges, and said it developed an initial set of data analysis that directly informs on market structure policy questions. Finally, the tool was said to have generated data that led to a number of investigations, exams and analyses, that had been launched, as the regulator got quantitative with the market data of trade executions.

A full copy of the press release regarding the merger approval can be found on the BATS and Direct Edge corporate websites.

Wintermute Wins U.S. Broker-Dealer Approval, Expanding Its Wall Street Ambitions

Featured Videos

CFD Activity Falls; MetaQuotes 1 Trillion AI Token Use

CFD Activity Falls; MetaQuotes 1 Trillion AI Token Use

CFD Activity Falls; MetaQuotes 1 Trillion AI Token Use

CFD Activity Falls; MetaQuotes 1 Trillion AI Token Use

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

![CTT Ratio example from SEC MIDAS tool [source: SEC]](https://www.financemagnates.com/wp-content/uploads/fxmag/2014/02/CTT-Ratio-example-SEC.jpg)