The Perils of Predictions

It didn’t take Nostradamus to work out that sooner or later, prediction markets would be beset by allegations of trading on insider or privileged information.

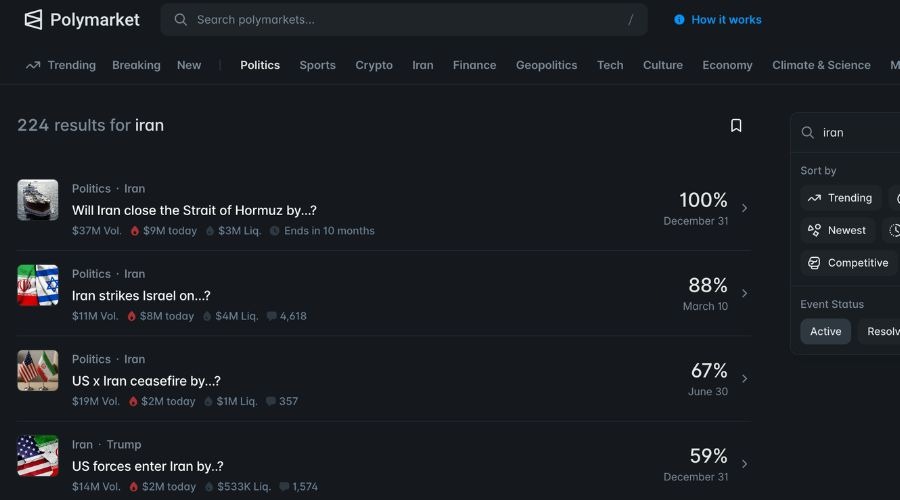

These concerns have come to a head since the US attacked Iran in late February, with users of these platforms staking hundreds of millions of dollars on events ranging from the date of the first attack to the date of a nuclear detonation.

Analytics platform Bubblemaps stated that half a dozen suspected ‘insiders’ had bet more than one million dollars on the timing of the strike on Iran, and other research firms have suggested that wagers placed on the fate of Iran’s supreme leader shared patterns with insider trading activity.

A statement issued by the Israeli government in mid-February confirmed that an undisclosed number of individuals had been arrested for placing bets based on classified information.

It seems strange that prediction market firms would allow themselves to be embroiled in such controversy for relatively little return at a time when regulators are taking a close look at their activities.

Read more: "We just launched our non-custodial crypto wallet, which also includes prediction markets," said eToro CEO

Just over a week before the first US missiles landed in Iran, the Commodity Futures Trading Commission (CFTC) filed a legal document in the case of North American Derivatives Exchange v. State of Nevada. The CFTC has long held the view that it has sole jurisdiction over prediction market regulation in the US, despite the efforts of various state bodies to impose their own rules.

“This power grab ignores the law and decades of precedent,” said CFTC chairman Michael Selig.

“Event contracts allow businesses and individuals to hedge event-driven risks, enable investors to manage portfolio exposure, and provide the public with information about the outcome of future events. These products are commodity derivatives and squarely within the CFTC’s regulatory remit.”

The founder and CEO of Polymarkets, one of the leading providers of prediction markets, has suggested that prediction markets serve a powerful informational function and value proposition, including in war zones.

“There is still a lot of resistance to innovation that kind of seems jarring to begin with,” he said in an interview at the MIT Sloan Sports Analytics Conference. “That is what makes it innovative and disruptive.”

Don’t Ignore This Side of the Pond

The phrase ‘Britain and America are two countries divided by a common language’, attributed to either George Bernard Shaw or Oscar Wilde (both of whom were Irish, by the way), is used to describe the cultural, vocabulary, and spelling differences between British and American English.

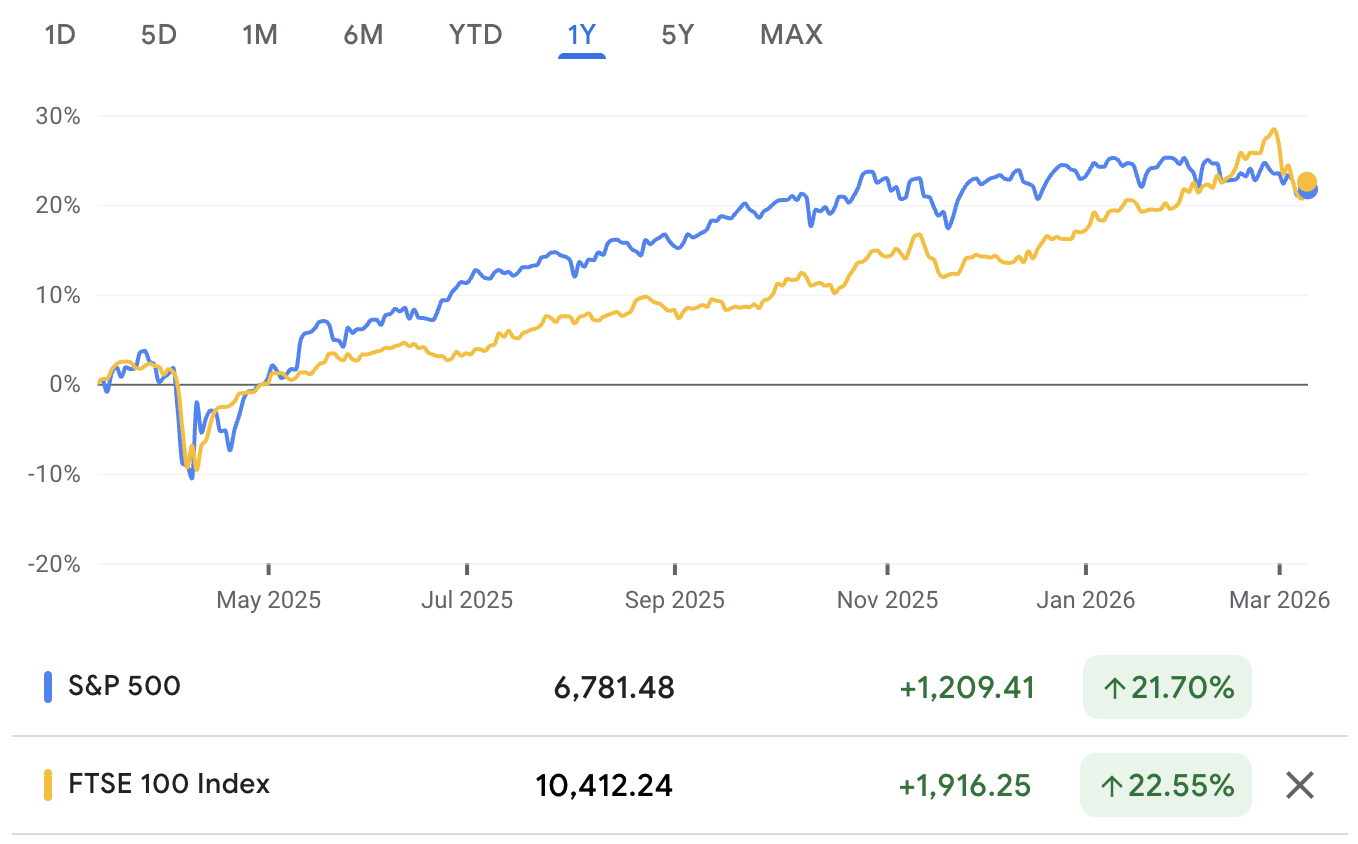

A similar divide has built up in equities in recent years as investors have focused on the US market amid perceptions of the UK as an ‘old world’ economy. But it would be a mistake to assume there is no value in Blighty.

Since the middle of the last decade, fund providers have been reducing their allocations to domestic stocks for UK investors, meaning that in some cases these investors have as little as 4% of their allocation in UK stocks.

Meanwhile, the tech-fuelled market boom in the US has led some investors to believe that, while America has embraced digital, the UK remains analogue. But the reality is rather different – since the start of this decade, the UK stock market has delivered higher returns and lower volatility.

One investment manager suggests that UK value should be a cause for celebration for the country’s domestic capital base and says the fact that it is rarely treated as such (or even acknowledged) shows the extent of the lack of alignment within that capital base.

He adds that regional valuation charts suggest it would be more than reasonable for that outperformance to continue, and that in some cases, underlying clients don’t realise the extent to which these changes have taken place. In other words, they think they own more UK stocks than they actually do and, even allowing for that, would like to own more.

No one is suggesting that just because an investor is based in the UK, they should allocate the majority of their investments to domestic stocks. However, there is a case to be made that current allocations are too low and that some adjustment to reflect actual market returns would be a prudent move.

- More Crypto, Fewer Cops

- From Growth Story to Income Play: ASEAN’s Dividend Shift

- IG Looks to Put the (Fat) Cat Among the Pigeons

Private Markets Attract Public Warnings

Allocations to private markets continue to reach new heights. Assets under management now stand at $6.5 trillion, and private markets account for one in every eight dollars allocated to portfolios globally.

As geopolitical tensions contribute to fluctuations in public markets, investors are turning to private markets to diversify their portfolios, manage risk, and pursue greater returns.

But as numerous market observers have noted, as private markets expand, the associated transparency challenges will also increase. Inconsistent and unclear data result in inaccurate valuations and delayed decision-making, made worse by manual procedures.

Related: Retail Investors Get Private Company Investment Access via Trade Republic

An experienced adviser suggests many investors in private credit, in particular, are suffering from buyer's remorse at the moment as they find themselves locked into positions, watching risks accumulate in slow motion.

His view is that recent developments at Blue Owl Capital (where the firm’s share value fell below its listing price amid investor concerns over redemptions and exposure to companies vulnerable to AI disruption) and the business development companies sector – specialised, publicly traded investment firms that provide debt and equity financing to small- and mid-sized private companies, often operating in a similar way to private equity – are reminiscent of the early stages of the collateralised debt obligation market meltdown in 2007.

Of more concern than volatility, which offers the prospect of upside, is the danger of permanent loss of capital. Downside volatility allows investors to enter positions cheaply and increase their returns.

Another potential issue is that when the big push for retail comes, which is already evident in the rising share of ETFs in collateralised loan obligation products, many retail investors will lose money.