A federal judge has ordered Stephen Ehrlich to pay $750,000 to defrauded customers of Voyager Digital, the cryptocurrency lending platform he once led before its spectacular collapse.

The consent order, entered yesterday (Monday) in Manhattan federal court, settles fraud charges the Commodity Futures Trading Commission (CFTC ) brought against Ehrlich in October 2023. The former CEO must funnel the money directly to Voyager customers through the company's ongoing bankruptcy liquidation.

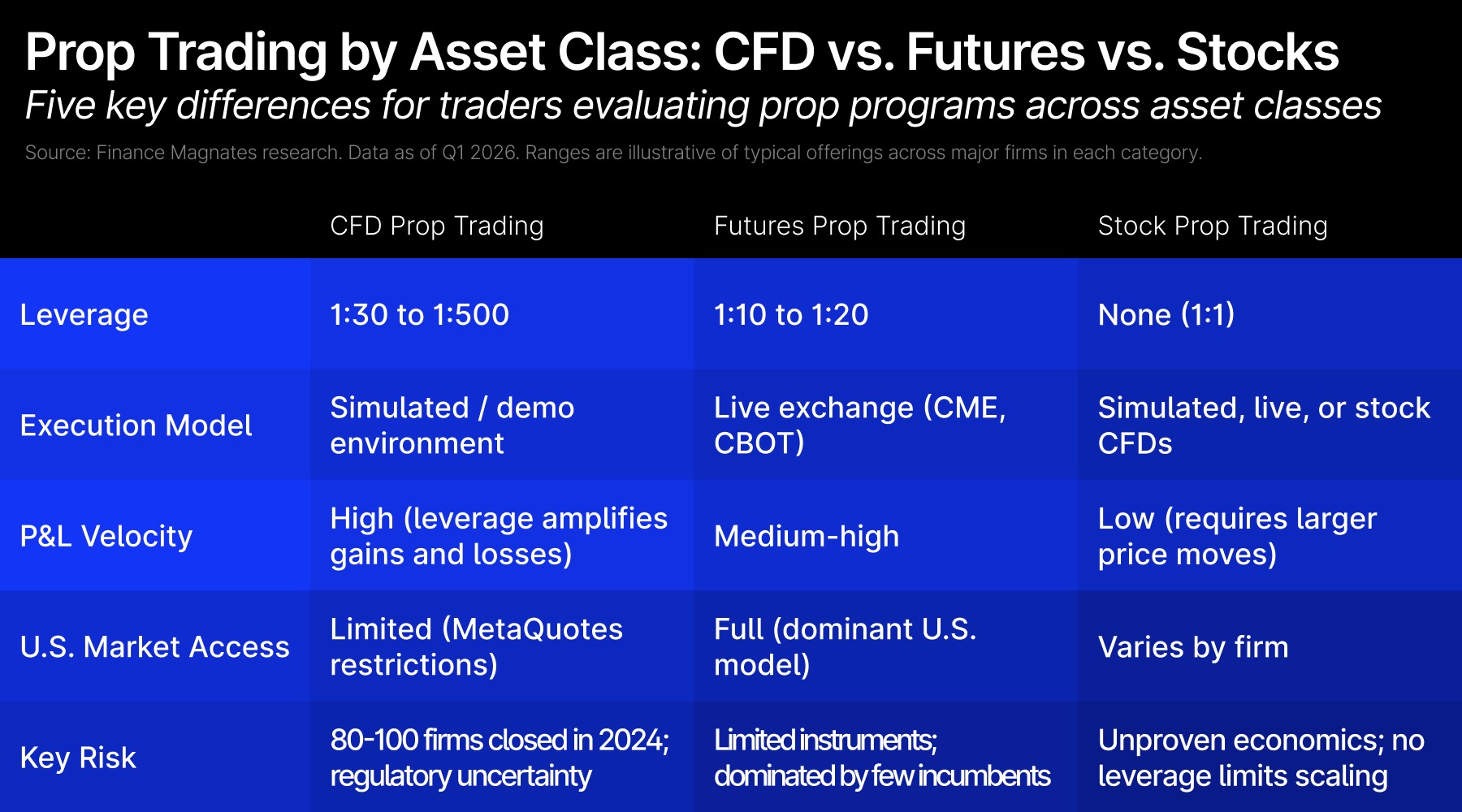

Digital assets meet tradfi in London at the fmls25

Former Voyager CEO Agrees to $750,000 Settlement in CFTC Fraud Case

Beyond the financial penalty, Ehrlich faces a comprehensive three-year ban from commodity trading activities. The restrictions block him from trading on registered exchanges, managing accounts containing commodity interests, or working for firms requiring CFTC registration.

The order also permanently bars Ehrlich from violating anti-fraud provisions of the Commodity Exchange Act. He neither admitted nor denied wrongdoing as part of the settlement.

“This resolution once again highlights the CFTC's important role in the digital asset space,” said Charles Marvine, acting chief of the Division of Enforcement's Retail Fraud and General Enforcement Task Force. “Compensating victims and limiting a defendant's ability to cause future harm are squarely within the CFTC's core mission.”

Platform Promised Safety, Delivered Losses

The CFTC's original lawsuit accused Ehrlich and Voyager of marketing their platform as a “safe haven” for digital assets while secretly transferring customer funds to high-risk borrowers. The company promised returns as high as 12% on certain cryptocurrencies stored on its platform.

To generate those returns, Ehrlich and Voyager pooled customer assets and transferred over $650 million to a hedge fund without proper due diligence, according to regulators. When that borrower defaulted in June 2022, Voyager faced immediate liquidity problems.

Ehrlich continued publicly claiming customer assets remained safe even as the company's finances deteriorated. Voyager filed for bankruptcy in July 2022, owing U.S. customers more than $1.7 billion.

For a time, the collapsed crypto lending platform was set to be acquired by Binance.US. However, just a few months after the announcement, the exchange withdrew from the $1 billion asset purchase deal.

Multiple Regulatory Actions

The CFTC settlement marks the latest penalty for Ehrlich, who has faced scrutiny from multiple federal agencies. In June, he agreed to pay $2.8 million to resolve Federal Trade Commission (FTC) charges over similar misleading claims about deposit insurance and asset safety.

The FTC accused Ehrlich of falsely telling customers their deposits carried FDIC insurance protection, making them “as safe with us as at a bank.” Most customer funds lacked such insurance coverage when Voyager collapsed.

Voyager customers have recovered roughly 35% of their cryptocurrency deposits through the bankruptcy process. Recovery rates could increase depending on ongoing litigation outcomes, including a dispute with failed exchange FTX over asset transfers.

The case reflects broader regulatory efforts to hold crypto executives accountable following the industry's dramatic downturn in 2022. Multiple digital asset lending platforms collapsed during that period, including Celsius Network and BlockFi, leaving customers with billions in losses.