Speculators trade on hope, fear and greed, but the fundamentals always win.

Bloomberg

This guest article was written by James Hyerczyk, financial analyst at FX Empire.

A change in the fundamental outlook and a potentially bearish weekly chart pattern are two strong indications that the speculative rally by October NYMEX Platinum and September NYMEX Palladium may be over for now.

After surging to a 15-month high at $1199.50 on August 10, platinum futures plunged $28 an ounce on August 11, a decline of 2.4%. Palladium futures lost 4.8%, falling below $700 an ounce after reaching its highest level the day before at $747.50 on August 10.

Both moves were strong enough to take platinum and palladium lower for the week. October Platinum finished the week at $1129.30, down $22.20 or 1.93%. September Palladium closed at $690.80, down $5.50 or 0.79%.

Fundamental Situation

While the sudden price spike higher last week may have been fueled by excessive speculation and traders taking advantage of thin-trading conditions, the violent sell-off was not without merit. A jump in supply was behind Thursday’s sharp pullback in platinum and palladium after data from South Africa showed increased output from mines.

According to sources, production of platinum and palladium fell by 12.4% in June compared to the prior month. But May output was the second highest on record and production is still rising on a year-on-year basis.

Based on this data, the early portion of the rally was justified. During last week’s trading sessions, however, speculators overdid the upside, setting up platinum and palladium for potential corrections into more reasonable price levels.

This should be considered normal price action. Speculators trade on hope, fear and greed, but the fundamentals always win especially since not all of the supply can be accounted for at times. Sometimes, companies hold on to inventory then bring it all to market when prices get high enough. This is similar to what happened last week.

From a fundamental standpoint, the supply/demand situation doesn’t appear to be out of control like copper. Production is rising, but so is demand from the automotive industry so conditions may be right for the rally to continue, especially if the Fed continues to pass on rate hikes and the U.S. dollar trades in a range or lower. Platinum and palladium are dollar-denominated commodities so they tend to be supported by increased foreign demand when the dollar weakens.

Technical Outlook

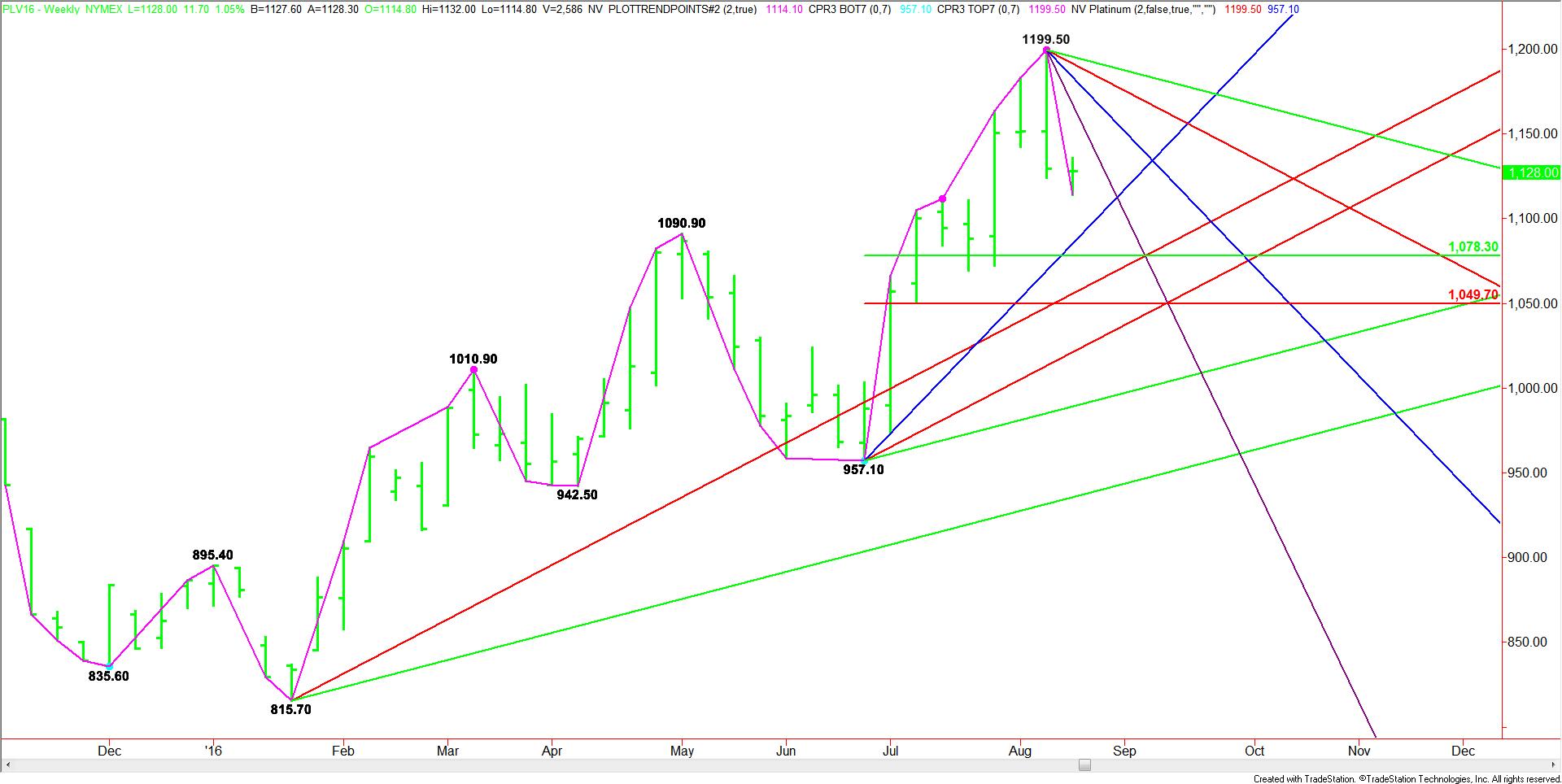

PLATINUM

The main trend is up according to the weekly swing chart. However, the higher-high, lower-close or closing price reversal top indicates that momentum has shifted to the downside. So far, the chart pattern only indicates the market is in position to post a 2 to 3 week correction into a retracement zone. There are no indications the trend is changing to down, but this may develop over the longer-term.

The short-term range is $957.10 to $1199.50. Its retracement zone at $1078.30 to $1049.70 is the primary downside target. The next decision for buyers will come following a test of this zone.

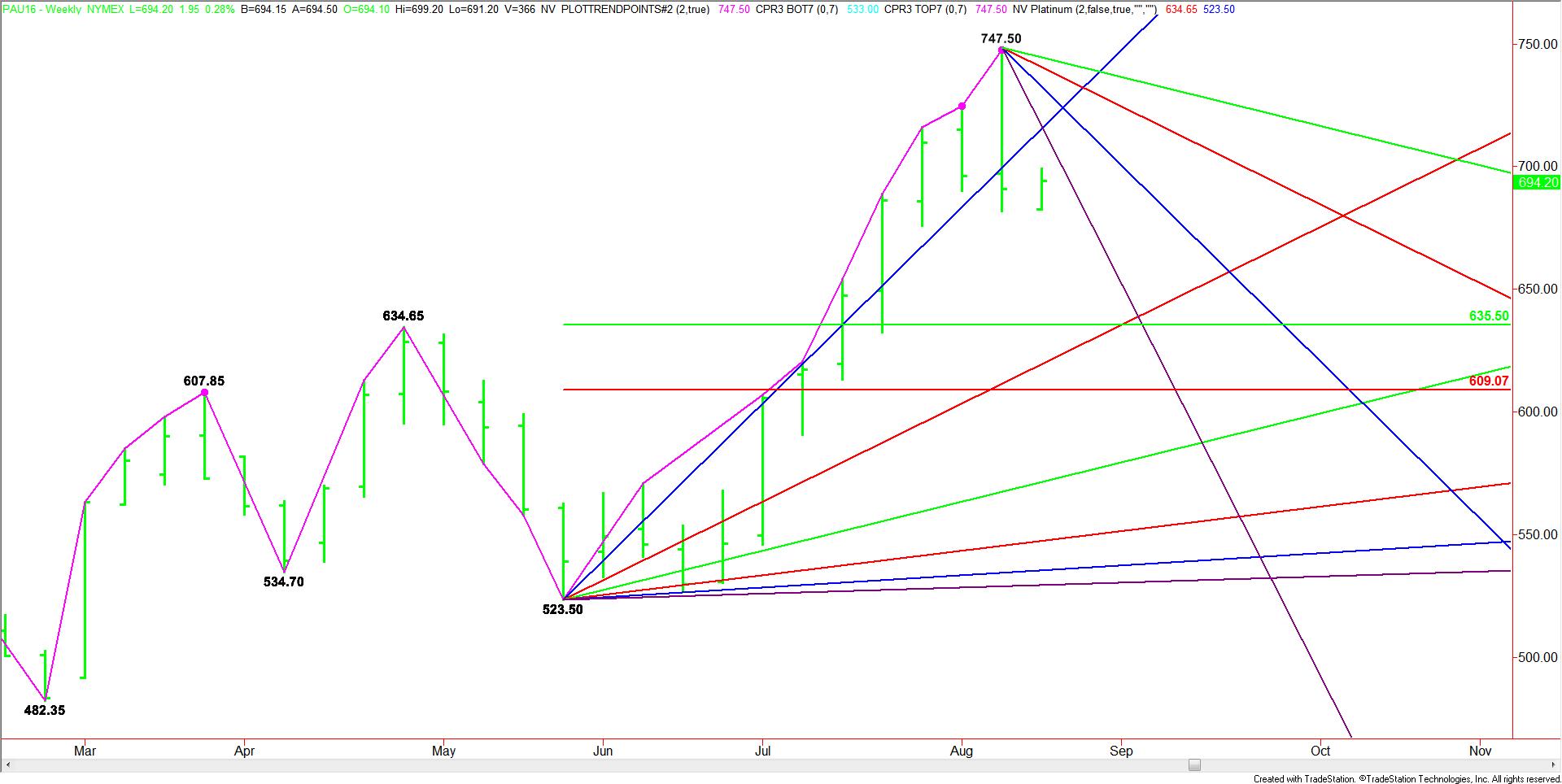

PALLADIUM

A similar pattern has developed in the September Palladium market. The main trend is up, however, its weekly closing price reversal top indicates that it is also ripe for a 2 to 3 week correction into a retracement zone.

The main range is $523.50 to $747.50. Its retracement zone at $635.60 to $609.05 is the primary downside target.

CONCLUSION

The key takeaway from this article is that we are looking for a 2 to 3 week correction on the weekly chart by both October Platinum and September Palladium. This move will bring prices back to earth and into value areas that should attract new buyers.

The fundamentals indicate that supply and demand are close to being balanced. The key market driver, therefore, should be the direction of the U.S. dollar and this will be controlled by what the Fed does with interest rates.

If it looks like the Fed is going to raise rates by the end of the year then we probably saw the top for the year for these two industrial metals. If the Fed remains cautious then investors will get a good buying opportunity on a return to the value zones.

This guest article was written by James Hyerczyk, financial analyst at FX Empire.

A change in the fundamental outlook and a potentially bearish weekly chart pattern are two strong indications that the speculative rally by October NYMEX Platinum and September NYMEX Palladium may be over for now.

After surging to a 15-month high at $1199.50 on August 10, platinum futures plunged $28 an ounce on August 11, a decline of 2.4%. Palladium futures lost 4.8%, falling below $700 an ounce after reaching its highest level the day before at $747.50 on August 10.

Both moves were strong enough to take platinum and palladium lower for the week. October Platinum finished the week at $1129.30, down $22.20 or 1.93%. September Palladium closed at $690.80, down $5.50 or 0.79%.

Fundamental Situation

While the sudden price spike higher last week may have been fueled by excessive speculation and traders taking advantage of thin-trading conditions, the violent sell-off was not without merit. A jump in supply was behind Thursday’s sharp pullback in platinum and palladium after data from South Africa showed increased output from mines.

According to sources, production of platinum and palladium fell by 12.4% in June compared to the prior month. But May output was the second highest on record and production is still rising on a year-on-year basis.

Based on this data, the early portion of the rally was justified. During last week’s trading sessions, however, speculators overdid the upside, setting up platinum and palladium for potential corrections into more reasonable price levels.

This should be considered normal price action. Speculators trade on hope, fear and greed, but the fundamentals always win especially since not all of the supply can be accounted for at times. Sometimes, companies hold on to inventory then bring it all to market when prices get high enough. This is similar to what happened last week.

From a fundamental standpoint, the supply/demand situation doesn’t appear to be out of control like copper. Production is rising, but so is demand from the automotive industry so conditions may be right for the rally to continue, especially if the Fed continues to pass on rate hikes and the U.S. dollar trades in a range or lower. Platinum and palladium are dollar-denominated commodities so they tend to be supported by increased foreign demand when the dollar weakens.

Technical Outlook

PLATINUM

The main trend is up according to the weekly swing chart. However, the higher-high, lower-close or closing price reversal top indicates that momentum has shifted to the downside. So far, the chart pattern only indicates the market is in position to post a 2 to 3 week correction into a retracement zone. There are no indications the trend is changing to down, but this may develop over the longer-term.

The short-term range is $957.10 to $1199.50. Its retracement zone at $1078.30 to $1049.70 is the primary downside target. The next decision for buyers will come following a test of this zone.

PALLADIUM

A similar pattern has developed in the September Palladium market. The main trend is up, however, its weekly closing price reversal top indicates that it is also ripe for a 2 to 3 week correction into a retracement zone.

The main range is $523.50 to $747.50. Its retracement zone at $635.60 to $609.05 is the primary downside target.

CONCLUSION

The key takeaway from this article is that we are looking for a 2 to 3 week correction on the weekly chart by both October Platinum and September Palladium. This move will bring prices back to earth and into value areas that should attract new buyers.

The fundamentals indicate that supply and demand are close to being balanced. The key market driver, therefore, should be the direction of the U.S. dollar and this will be controlled by what the Fed does with interest rates.

If it looks like the Fed is going to raise rates by the end of the year then we probably saw the top for the year for these two industrial metals. If the Fed remains cautious then investors will get a good buying opportunity on a return to the value zones.

James A. Hyerczyk is a financial analyst for FX Empire, a leading financial portal. James has worked as a fundamental and technical financial market analyst since 1982. His technical work features the pattern, price and time analysis techniques of W.D. Gann. James A. Hyerczyk is a senior analyst at FX Empire. He has worked as a fundamental and technical financial market analyst since 1982. His technical work features the pattern, price and time analysis techniques of W.D. Gann.

Plus500 Sees 20% Margin on Its US Business, Double What Its CEO Calls Market Practice

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.