Gain Capital which filed its first S-1 over a year ago has renewed it again month and a half ago and now it finally put a price on it. According to WSJ Gain intends to sell 11 million shares for around $190 million and will have a total of 31 million shares after the IPO. This means that at best scenario Gain Capital values itself at just $535 million - roughly half of what FXCM does.

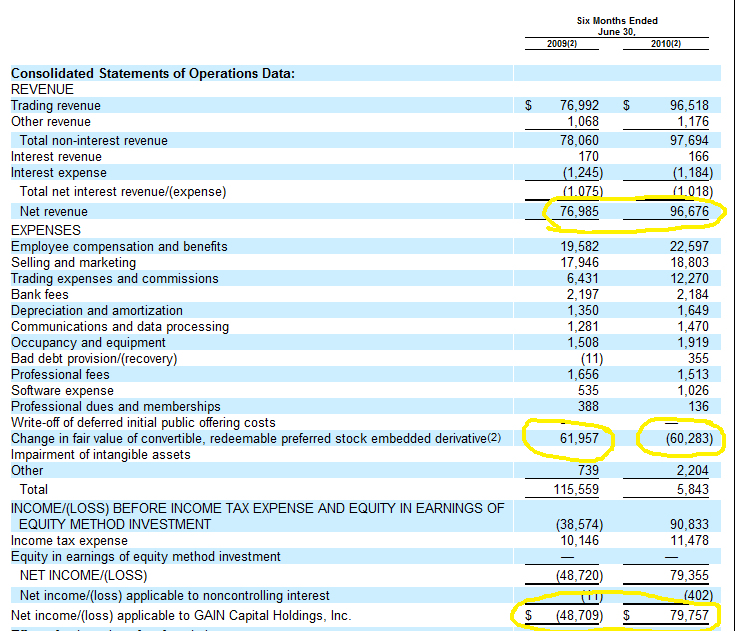

Gain's revenue is roughly 45% lower than FXCM's however count on fancy accounting methods to make Gain appear much more profitable. Looking at the numbers we can see that FXCM kept a relatively steady level of profitability - around $100 million net income before taxes in 2009 and 2010. Gain however displayed a net loss of ~$50 million on a revenue of $77 million in the first half of 2009 but amazingly showed a net income of $79 million on a $97 million revenue. How is such profitability possible even in the highly profitable Forex market you ask? The answer is pretty simple, or not, and is called "Change in fair value of convertible, redeemable preferred stock embedded derivative" which added $62 million to Gain's expenses in 2009 but removed $60 million from Gain's expenses in 2010.

Reading further this is explained as: "For each of the periods indicated, in accordance with Financial Accounting Standards Board, or FASB Accounting Standards Codification, or ASC 815, Derivatives and Hedging, we accounted for an embedded derivative liability attributable to the redemption feature of our outstanding preferred stock. This redemption feature and the associated embedded derivative liability will no longer be required to be recognized upon conversion of our preferred stock in connection with the completion of this offering."

I have no idea what means so help me God, but all I know is that it turned Gain into a very profitable company in 2010 while the income and expenses haven't changed that dramatically from 2009.

The clock is ticking on both companies and FXCM which announced its pricing this week has only one more day left to complete its IPO, if it intends to do so this week. I'd say FXCM's chances are much better than Gain's so if FXCM fails this will also pull the plug on Gain's high flying hopes. It would also be a huge blow for this industry if both IPOs fail as retail fx strives to break it into the mainstream and having a few public companies amongst its ranks will only help it to achieve this goal.

The other interesting IPO that might happen some time soon is FxPro. Trust Oanda that it monitors this situation very very closely for several reasons.