Private equity and private credit dominate alternative investment allocations among Singapore-based family offices.

Geopolitical tensions and market scale influence reduced exposure to China and smaller APAC markets.

From Left: Ginny Goh, Kelly Chia, Ken Chew

Banks and fund managers are tapping into demand from family offices in

Singapore for alternative investments by proactively bringing such

opportunities to their clients.

The family office market in Singapore can be divided into pre-2019 or

‘old’ money and the ‘new’ money that has come into since 2019 – an influx that

has seen the number of private companies handling investment management and

wealth management for a wealthy families increase dramatically over the last

five years.

Entrepreneurial Backgrounds Support Risk-Taking

This cycle of not only assets but also inflow of talent and high net

worths is described by Ken Chew, CEO & Partner at fund manager IWC as the

longest and most sustainable cycle of the last half-century.

One of the most notable aspects of Singapore family offices’

investment strategies is their relatively high allocation to alternatives – a

trend Chew attributes to first generation wealth creators having a higher risk

tolerance.

“This is not to say wealth preservation is not important but their

entrepreneurial background means they are more willing to allocate to digital

assets and explore new markets,” adds Chew. “For example, when we hosted the

first Web3 conference here in 2020 there was no ecosystem – now investment is

booming.”

Another factor that contributes to their openness to alternative

investments is that Asian family office wealth is primarily first generation

and the principals have therefore often made their money through a different

business model to their counterparts in US or Europe.

Regulation and Tax Structures Support Private Market Access

According to Kelly Chia, head of investment strategy UOB Private Bank,

there are a number of other reasons for the shift towards alternatives.

“Firstly, APAC family offices are investing more in private markets to

diversify their risk and generate higher returns with illiquidity premia,” he

says. “Secondly, Singapore has tax rules and fund structures (Sections 13O/13U

and the Variable Capital Company) that make it operationally easier and more

tax efficient to invest in private funds."

"Thirdly, proximity to high growth

deal flows in Southeast Asia and India gives investors better access to direct

and co-investments in private equity, private credit and infrastructure.”

“This contrasts with many western peers, where shorter evaluation

cycles and public market benchmarks remain more dominant,” saysGinny Goh, director, private clients at Ocorian

Singapore.

“In a volatile market environment, alternatives are increasingly

viewed as a core diversification tool rather than a tactical allocation. For

Singapore-based families with global portfolios, alternatives also provide

greater control over risk, access to private growth opportunities in Asia and

insulation from short-term market dislocations.”

Limited Domestic Market Pushes Capital Overseas

The relatively small size of the domestic investment universe forces

family offices in Singapore to look beyond their home market for investment

opportunities, observes Chew.

“Regionally and globally, we are looking at deep tech projects,

including those that are ESG-related with impact plus economic returns,” he

says. “In general, family offices in Singapore prefer to have an additional

edge that is delivered through good technologies and good management teams.”

Chew reiterates that the modest scale of the investment market in

Singapore makes a purely domestic focus generally unsustainable.

“The millions or tens of millions you will make here is nothing

compared to what you can generate when you scale regionally or globally,” he

adds. “So you should look at those start-ups that can scale globally unless

there is a strong disruptive story. Singapore is a good bridge in the current

cycle due to the confluence of money, talent, projects and information.”

While family offices actively seek to diversify across regions,

sectors and asset classes to mitigate risk, regional biases continue to

influence their allocation decisions based on geographic location and

familiarity, she adds.

“For example, Singapore-based family offices typically have

significant exposure to the US, Singapore and Hong Kong/China markets, while

allocating less to Europe or other regions such as Thailand and Australia,”

says Chow. “Conversely, family offices based in Hong Kong tend to concentrate

heavily on the US and Hong Kong/China markets, with minimal exposure to

Singapore or other regions.”

Chia agrees that within alternatives, allocations are primarily

directed toward private equity. These include both direct and co-investments,

private credit - which is rapidly gaining favour for its yield potential - and

real assets such as digital infrastructure (data centres, towers, fibre) and

energy transition platforms.

“Select real estate is also included in portfolios for its income

generation and diversification benefits,” he says. “Sector preferences tend to

focus on AI and computing, software and healthcare, along with fintech and

financial services.”

Private Equity Dominates Alternative Allocations

Chia agrees that Singapore family offices are increasingly expanding

their exposure across the region, particularly in India, Japan and Southeast

Asia, driven by growing opportunities in digital infrastructure and renewables.

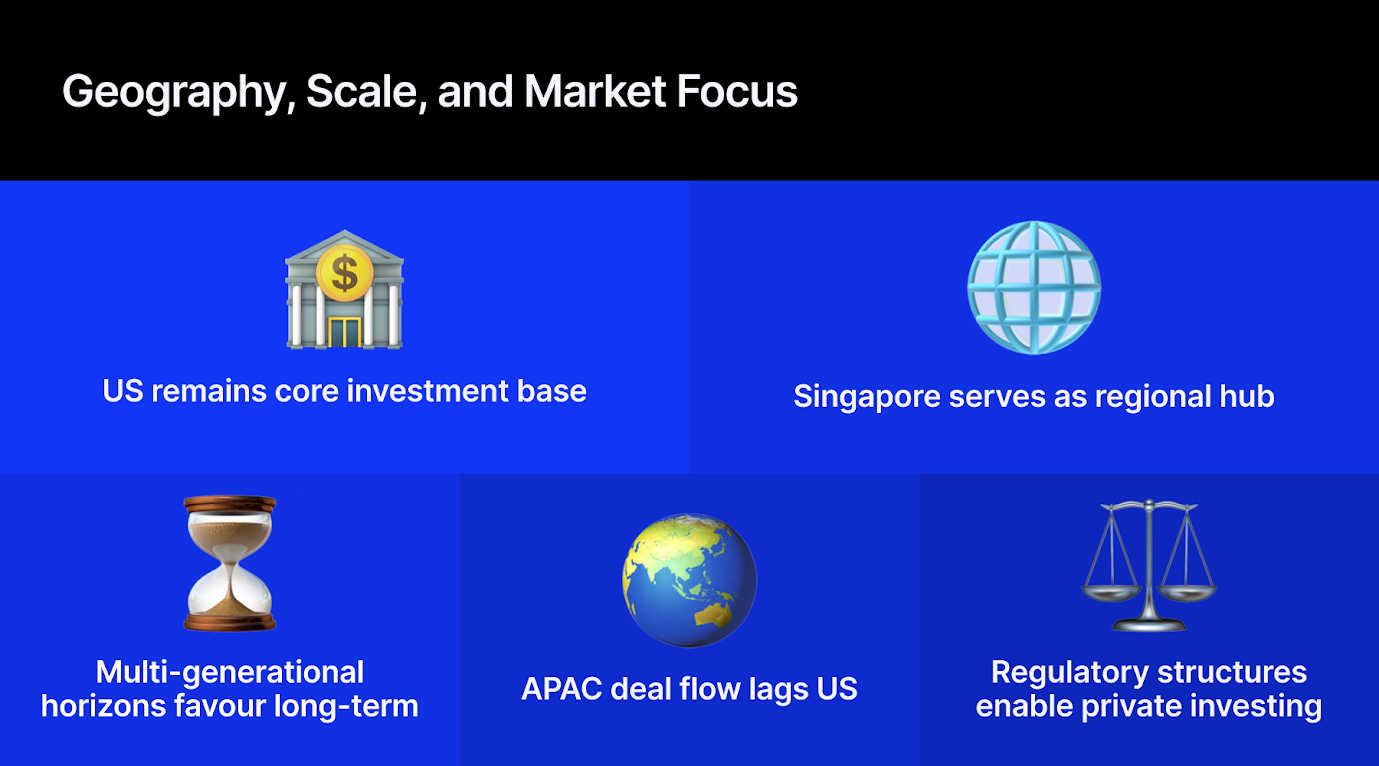

“However, their investment base remains anchored in the US,” he says.

“The US continues to offer the largest pool of private market deals, with 2025

private equity transactions approaching $1.2 trillion, strong exit options and

dominant private credit capacity.

In comparison, APAC recorded only $176

billion in deal value for 2024 and Southeast Asia around $16 billion. Due to

political and geopolitical tensions, deal flows from China have slowed,

resulting in more limited exposure.”

Private equity remains a core allocation, particularly mid-market and

growth strategies focused on buy-and-build and operational transformation, says

Goh. “Private credit continues to attract capital due to its ability to offer

downside protection, income visibility and structural safeguards, especially in

asset-backed and senior lending strategies,” she adds.

US Anchors Portfolios as Asia Provides Growth

Chia concludes that overall, Singapore family offices tend to build

their portfolios with a US core for scale and liquidity, supplemented with

regional investments to benefit from proximity, diversification and secular

growth.

Banks and fund managers are tapping into demand from family offices in

Singapore for alternative investments by proactively bringing such

opportunities to their clients.

The family office market in Singapore can be divided into pre-2019 or

‘old’ money and the ‘new’ money that has come into since 2019 – an influx that

has seen the number of private companies handling investment management and

wealth management for a wealthy families increase dramatically over the last

five years.

Entrepreneurial Backgrounds Support Risk-Taking

This cycle of not only assets but also inflow of talent and high net

worths is described by Ken Chew, CEO & Partner at fund manager IWC as the

longest and most sustainable cycle of the last half-century.

One of the most notable aspects of Singapore family offices’

investment strategies is their relatively high allocation to alternatives – a

trend Chew attributes to first generation wealth creators having a higher risk

tolerance.

“This is not to say wealth preservation is not important but their

entrepreneurial background means they are more willing to allocate to digital

assets and explore new markets,” adds Chew. “For example, when we hosted the

first Web3 conference here in 2020 there was no ecosystem – now investment is

booming.”

Another factor that contributes to their openness to alternative

investments is that Asian family office wealth is primarily first generation

and the principals have therefore often made their money through a different

business model to their counterparts in US or Europe.

Regulation and Tax Structures Support Private Market Access

According to Kelly Chia, head of investment strategy UOB Private Bank,

there are a number of other reasons for the shift towards alternatives.

“Firstly, APAC family offices are investing more in private markets to

diversify their risk and generate higher returns with illiquidity premia,” he

says. “Secondly, Singapore has tax rules and fund structures (Sections 13O/13U

and the Variable Capital Company) that make it operationally easier and more

tax efficient to invest in private funds."

"Thirdly, proximity to high growth

deal flows in Southeast Asia and India gives investors better access to direct

and co-investments in private equity, private credit and infrastructure.”

“This contrasts with many western peers, where shorter evaluation

cycles and public market benchmarks remain more dominant,” saysGinny Goh, director, private clients at Ocorian

Singapore.

“In a volatile market environment, alternatives are increasingly

viewed as a core diversification tool rather than a tactical allocation. For

Singapore-based families with global portfolios, alternatives also provide

greater control over risk, access to private growth opportunities in Asia and

insulation from short-term market dislocations.”

Limited Domestic Market Pushes Capital Overseas

The relatively small size of the domestic investment universe forces

family offices in Singapore to look beyond their home market for investment

opportunities, observes Chew.

“Regionally and globally, we are looking at deep tech projects,

including those that are ESG-related with impact plus economic returns,” he

says. “In general, family offices in Singapore prefer to have an additional

edge that is delivered through good technologies and good management teams.”

Chew reiterates that the modest scale of the investment market in

Singapore makes a purely domestic focus generally unsustainable.

“The millions or tens of millions you will make here is nothing

compared to what you can generate when you scale regionally or globally,” he

adds. “So you should look at those start-ups that can scale globally unless

there is a strong disruptive story. Singapore is a good bridge in the current

cycle due to the confluence of money, talent, projects and information.”

While family offices actively seek to diversify across regions,

sectors and asset classes to mitigate risk, regional biases continue to

influence their allocation decisions based on geographic location and

familiarity, she adds.

“For example, Singapore-based family offices typically have

significant exposure to the US, Singapore and Hong Kong/China markets, while

allocating less to Europe or other regions such as Thailand and Australia,”

says Chow. “Conversely, family offices based in Hong Kong tend to concentrate

heavily on the US and Hong Kong/China markets, with minimal exposure to

Singapore or other regions.”

Chia agrees that within alternatives, allocations are primarily

directed toward private equity. These include both direct and co-investments,

private credit - which is rapidly gaining favour for its yield potential - and

real assets such as digital infrastructure (data centres, towers, fibre) and

energy transition platforms.

“Select real estate is also included in portfolios for its income

generation and diversification benefits,” he says. “Sector preferences tend to

focus on AI and computing, software and healthcare, along with fintech and

financial services.”

Private Equity Dominates Alternative Allocations

Chia agrees that Singapore family offices are increasingly expanding

their exposure across the region, particularly in India, Japan and Southeast

Asia, driven by growing opportunities in digital infrastructure and renewables.

“However, their investment base remains anchored in the US,” he says.

“The US continues to offer the largest pool of private market deals, with 2025

private equity transactions approaching $1.2 trillion, strong exit options and

dominant private credit capacity.

In comparison, APAC recorded only $176

billion in deal value for 2024 and Southeast Asia around $16 billion. Due to

political and geopolitical tensions, deal flows from China have slowed,

resulting in more limited exposure.”

Private equity remains a core allocation, particularly mid-market and

growth strategies focused on buy-and-build and operational transformation, says

Goh. “Private credit continues to attract capital due to its ability to offer

downside protection, income visibility and structural safeguards, especially in

asset-backed and senior lending strategies,” she adds.

US Anchors Portfolios as Asia Provides Growth

Chia concludes that overall, Singapore family offices tend to build

their portfolios with a US core for scale and liquidity, supplemented with

regional investments to benefit from proximity, diversification and secular

growth.

Paul Golden is an experienced freelance financial journalist with a strong institutional background. Over the past two decades, he has written for globally recognised financial publications, covering topics such as market structure, regulation, trading behaviour, and economic policy.

75% of Kalshi Users Never Trade, but Platform Still Intends to Capitalise on That

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.