Financial markets largely moved on after the United States and Iran announced an agreement over the weekend. On Polymarket, traders are still debating whether the event happened at all.

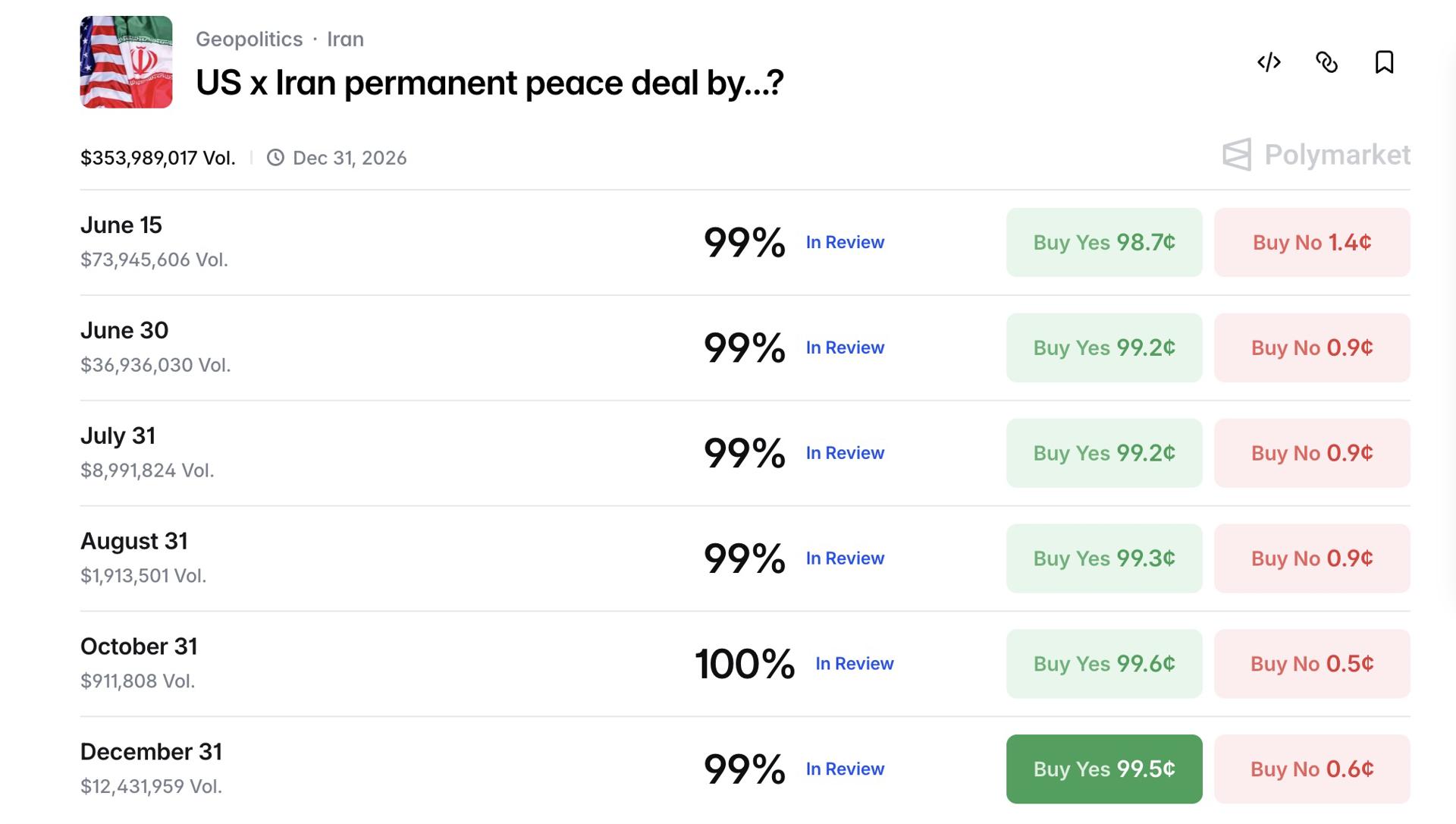

The prediction market platform has processed more than $345 million in volume on contracts tied to a US-Iran peace deal. While both countries announced an agreement, the market remains unresolved because users disagree on whether the developments satisfy the contract’s requirement for a “permanent peace deal.”

When Does a Peace Deal Count?

The dispute turns on Polymarket’s definition of a “permanent peace deal.” According to the contract rules, a qualifying agreement must explicitly indicate that military hostilities between the two countries have ended or will permanently cease. Agreements that are temporary, or that do not clearly establish a lasting end to hostilities, do not qualify.

That wording has left traders split. Supporters of a “yes” resolution point to public statements describing the agreement as a permanent end to military operations.

Opponents argue that negotiations are still ongoing, no final document has been signed, and parts of the arrangement remain temporary, including the reported 60-day reopening of the Strait of Hormuz.

Traders are now arguing over contract language and official paperwork, not the underlying event itself.

Who Gets the Final Say?

As with other disputed Polymarket markets, the final decision now rests with UMA token holders. They debate contested outcomes before voting on a resolution.

The process has faced criticism in the past. Bloomberg recently reported that nine wallets control more than half of the tokens used in dispute votes. That concentration has raised concerns that a small group of participants can influence outcomes involving hundreds of millions of dollars.

The outcome now depends on how UMA voters read the contract language and the available public statements. Contracts remain tradable during the dispute process, meaning users can effectively trade on how arbitrators are likely to settle the dispute.

- Google Employee’s Near-Perfect Polymarket Bets End in Insider Trading Charges

- Polymarket Targets Japan with Formal Lobbying Effort, Signaling Industry Shift

- Nasdaq Private Market Becomes Data Provider for Polymarket’s Private Company Markets

Beyond One Market

The Iran dispute highlights a broader challenge for prediction markets as they move into increasingly complex subjects such as geopolitics, regulation and public policy.

Prediction markets have become highly effective at aggregating expectations. Settlement remains more difficult when outcomes depend on interpretation rather than a clearly verifiable event.

Platforms have taken different approaches. Polymarket relies on external token-holder governance to resolve disputed outcomes. Kalshi, by contrast, settles markets under a predefined CFTC-regulated rulebook.

Both approaches ultimately face the same challenge: how should a binary market resolve events that do not fit neatly into a yes-or-no outcome?