As the spread of COVID-19 continues to evolve, so too does its effects on financial markets around the globe.

FM

Finally, after the coronavirus (COVID-19) brought forth days of some of the worst price movements that financial markets have seen in years--or even decades--investors may be breathing a small sigh of relief.

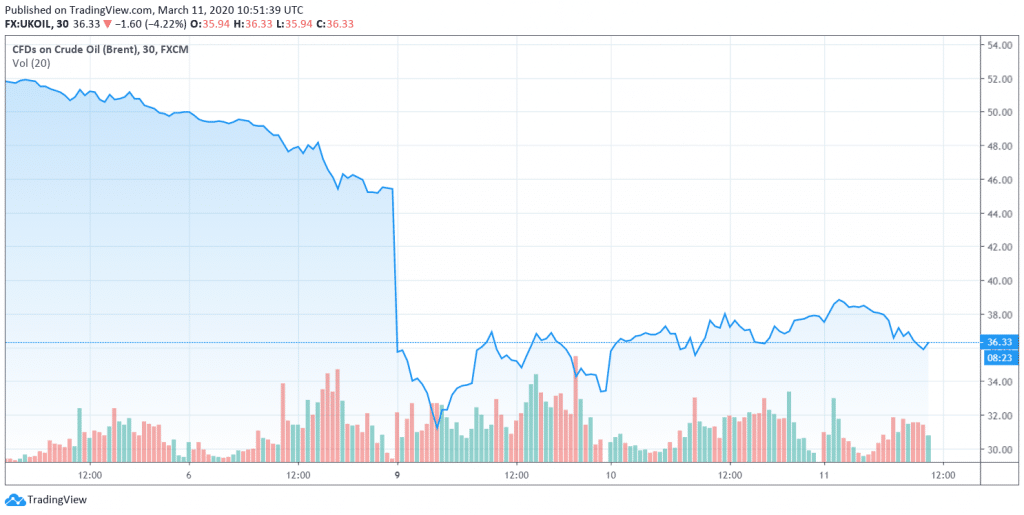

At press time, the S&P500 was showing upward motion, with a 24-hour increase of just under 5 percent. The Brent Crude international oil standard, which dove 30 percent when trading opened on Monday, has stabilized around $37 a barrel and is even showing some small progress toward recovery.

After falling from a weekend peak of around $9,100 on Saturday, March 7th, the price of Bitcoin also seems to have stabilized around $7900, where it has sat for roughly 48 hours.

In other words, it seems that the economic free-fall that was brought by the spread of the coronavirus over the weekend seems to have been slowed, at least for the moment.

But what's next? While markets may have reached a point of stabilization, it seems that they hang in a precarious position between recovery and further disaster.

What are the factors influencing the direction of this path? And what are the best and worst outcomes of the current situation?

"A 'perfect storm' of sorts"

Most analysts agree that the path forward will be determined by two things: first, the way that the virus continues to spread, and second, the ways that governments continue to respond to it.

Meltem Demirors, chief strategy officer at CoinShares.

However, in the worst case, Ms. Demirors says that in the worst case, there will be a "long-term market correction of 20-30% down from highs, with 0 or negative rates and extended quantitative easing (including asset-buying across all asset types.)"

Financial markets appeared unconvinced of a pledge from the United States to blunt the impact of the coronavirus, as the number of cases continued to rise in the world’s biggest economy https://t.co/KeZv9FFCB1

But for the moment, things aren't necessarily looking very good: "we're seeing a sell-off across the board as investors contend with a few macro events converging into a 'perfect storm' of sorts," Ms. Demirors told Finance Magnates.

"First, supply chain disruptions from a slowdown in Chinese manufacturing have impacted many companies across sectors. Second, as concerns over the coronavirus mount, we are seeing individual markets and consumer sectors impacted."

Additionally, Governments have also scrambled--and, in some cases, fumbled--to assemble a proper response to the virus. Some have all by halted business operations in their countries, including Italy, which has extended restrictions on movement to the entire nation: the New York Times reported that Prime Minister Giuseppe Conte has "[banned] public gatherings and [asked] people not to travel except for work or emergencies."

Further market disruptions could be underway

If Italy's movements toward further restriction are any indication of what other governments may institute across the globe, then it may be likely that the virus will continue to disrupt financial markets.

Of crouse, "we're accustomed to volatility in crypto markets, so for those of us who've been on the rollercoaster ride, it's more of the same," she added.

Indeed, while Bitcoin shed roughly 14 percent of its value over the weekend, it had only been several months since a quick drop of a similar size had occurred; on the other hand, a drop matching Brent Crude's 30 percent fall on Monday hadn't been seen since January 17th, 1991, the starting day of the first Gulf War.

Therefore, "for macro markets, volatility is going to be a tricky thing to manage, and we're already seeing implosions and explosions like the VIX blowout on Friday," Ms. Demirors said, referring to CBOE's real-time market index that represents market expectations of forward-looking volatility for the next 30 days.

The index, which has been nicknamed the "fear gauge," spiked between Friday and Monday, peaking at 62.12 on Monday morning, its highest level since the financial crisis, when it rose to 89.53.

The world may "see the failure of monetary policy"

All of these factors seem to indicate that in the longer term, "we [will] see the failure of monetary policy," Ms. Demirors said.

"Since the crisis in 2009, the approach taken by global central banks has been to lower rates and print more money," she explained. Indeed, "since 2009, the US money supply has more than tripled," even when printing between November 2019 and March 2020 isn't counted. At the same time, interest rates in the US "have tumbled."

This has led to a kind of breaking point. "With over 25% of sovereign debt yielding negative interest, we are seeing central bankers rapidly running out of tools in their toolkit, because the tools no longer work," Ms. Demirors said.

Looks like a global coordinated monetary policy response to coronavirus by CenBanks is in the offing. BOE pledges to take needed steps to protect stability amid virus. Verbal intervention first started w/a surprise Fed statement. BoJ also released a similar statement today. pic.twitter.com/2d07sSkSmc

— Holger Zschaepitz (@Schuldensuehner) March 2, 2020

"The question then becomes what other measures they will take," she continued. "Here we see concerning signs, with the Fed indicating they may look to buy corporate bonds."

Indeed, the New York Timesreported that Eric Rosengren, the president of the Federal Reserve Bank of Boston, suggested during a recent speech that "officials may need to buy assets other than government bonds to counter the next downturn," a move that may require legislative changes, and could result in even lower interested rates. This could eventually lead to negative rates, which, although they are "used in Japan and parts of Europe, probably would not work well in the United States."

"The real question is when and how the crisis in the stock market will be expressed."

Monetary policy in the United States could also eventually fail because of the amount of USD liquidity that could potentially flood the market: "there are trillions of dollars of 'dry powder' sitting on the sidelines," she pointed out, citing figures from alternative finance data firm Preqin.

"There is $1.5 trillion of cash in private equity and venture capital funds that need to be deployed," with "the bulk, $1.4 trillion, in private equity."

All of this, in Ms. Demirors' opinion, points to a rather grim ending: "we are certainly headed into a recession, meaning a period of economic contraction, versus the period of economic expansion we have been in the last 11 years," she said.

However, "in terms of crisis or depression, I don't believe we are there yet," she added. Indeed, "if we look at typical signifiers of a crisis or depression," they just aren't there--at least, not yet.

"We haven't seen unemployment rise (yet) – in fact, we are at record employment levels, we have not yet seen a sustained fall in output or GDP, and projections still have GDP across the world expected to rise, albeit at 1% as opposed to 2-3%," Ms. Demirors explained.

Additionally, "deflation in key stores of wealth such as home values and other long-term 'safe haven' assets hasn't hit yet."

"The real question is when and how the crisis in the stock market will be expressed across labor, growth, and long-term asset prices."

Is Bitcoin a safe haven or not? The answer could be somewhere in the middle

But how could the longer-term trajectory of these traditional financial markets affect the longer-term trajectory of the price of Bitcoin?

After all, the price movements of BTC in the wake of the spread of the coronavirus have, to a large extent, upended expectations about the role that Bitcoin will play in the wake of the global financial crisis. Many industry insiders have long expected that Bitcoin will act as a 'safe haven,' and will rise in the face of uncertainty. However, it seems--at least, so far--that the opposite is closer to the truth.

Indeed, a spokesperson from Digital Asset Investment Management (DAiM), the self-styled "first licensed registered investment advisor for Bitcoin and digital assets," told Finance Magnates that although "the conversation and questions about Bitcoin over the past few weeks have centered around, 'is it a safe haven or not a safe haven?'," the reality is that the question isn't so simple.

"In our opinion, the truth is somewhere in the middle," DAiM's spokesperson said. "Bitcoin is absolutely a speculative risk asset and an emerging speculative store of value."

"Any time markets experience fear, uncertainty, and volatility; risk assets trade with a near correlation of zero as investors tend to sell off anything liquid that isn't nailed down," which "includes Bitcoin."

"That being said, Bitcoin doesn't need a perfect inverse relationship against risk assets to prove its usefulness as an emerging store of value or its well-earned place in your overall portfolio as a noncorrelated asset and future form of money."

DAIM also pointed out that "despite its recent weakness, Bitcoin is up more than seven percent on the year while equities are down [roughly] 15 percent."

If you're looking for bearish narratives, there are currently 3 that could be impacting #bitcoin 1.) Coronavirus (all markets selling off) 2.) Miner hoarding (typically strong bearish indication) 3.) PlusToken scam dumping on the market again. (They moved 19k bitcoin yesterday)

"Bitcoin will find a bottom long before stocks do."

But can Bitcoin manage to hold onto the progress that it has made this year, or will the price continue to decline?

DAIM believes that much like other financial markets, Bitcoin's trajectory heavily depends on the ways that the virus is handled as a public health crisis: that in the best case, Bitcoin--along with other financial markets--will react positively to a swift and effective government response that will contain the spread of the coronavirus.

A disease specialist in Seattle had the ability (and instinct) to test for coronavirus as early as January.

This kind of action would "[calm] the markets, and [reduce] the fear of this spiraling into a larger outbreak, which would only cause a more violent and protracted economic slowdown," DAiM said. "The best-case scenario for Bitcoin is that once the dust settles, that it begins decoupling from risk assets, it resumes its noncorrelated performance as a non-sovereign, hard-capped, fixed-supply, immutable store of value."

However, in the worst-case scenario (or even a worst-case scenario), there could be some bigger bumps in the road--again, depending largely on the way that governments manage to handle the outbreak: "while we are not experts in epidemiology, it is our contention that if coronavirus maintains its current trajectory and continues to disrupt global markets, it's more than likely that Bitcoin will be negatively affected," DAiM said.

This is because "speculative capital will likely sell first, ask questions later."

The logo of Digital Asset Investment Management (DAiM), the self-styled "first licensed registered investment advisor for Bitcoin and digital assets."

That being said, DAiM believes that "Bitcoin will find a bottom long before stocks do."

Still, the long-term effects of the coronavirus and the surrounding governmental response are very difficult to predict.

"We will get through this, but at what cost? Will we react fast enough to protect our people and humans of the world? Will the monetary and fiscal policies of central banks and governments be misguided, focusing on saving markets and softening the blow against GDP growth decline and the potential for any sort of recession, rather than care for humans and saving lives?", DAiM asked.

"It's too early to know, but if history is a guide, massive change is coming."

Finally, after the coronavirus (COVID-19) brought forth days of some of the worst price movements that financial markets have seen in years--or even decades--investors may be breathing a small sigh of relief.

At press time, the S&P500 was showing upward motion, with a 24-hour increase of just under 5 percent. The Brent Crude international oil standard, which dove 30 percent when trading opened on Monday, has stabilized around $37 a barrel and is even showing some small progress toward recovery.

After falling from a weekend peak of around $9,100 on Saturday, March 7th, the price of Bitcoin also seems to have stabilized around $7900, where it has sat for roughly 48 hours.

In other words, it seems that the economic free-fall that was brought by the spread of the coronavirus over the weekend seems to have been slowed, at least for the moment.

But what's next? While markets may have reached a point of stabilization, it seems that they hang in a precarious position between recovery and further disaster.

What are the factors influencing the direction of this path? And what are the best and worst outcomes of the current situation?

"A 'perfect storm' of sorts"

Most analysts agree that the path forward will be determined by two things: first, the way that the virus continues to spread, and second, the ways that governments continue to respond to it.

Meltem Demirors, chief strategy officer at CoinShares.

However, in the worst case, Ms. Demirors says that in the worst case, there will be a "long-term market correction of 20-30% down from highs, with 0 or negative rates and extended quantitative easing (including asset-buying across all asset types.)"

Financial markets appeared unconvinced of a pledge from the United States to blunt the impact of the coronavirus, as the number of cases continued to rise in the world’s biggest economy https://t.co/KeZv9FFCB1

But for the moment, things aren't necessarily looking very good: "we're seeing a sell-off across the board as investors contend with a few macro events converging into a 'perfect storm' of sorts," Ms. Demirors told Finance Magnates.

"First, supply chain disruptions from a slowdown in Chinese manufacturing have impacted many companies across sectors. Second, as concerns over the coronavirus mount, we are seeing individual markets and consumer sectors impacted."

Additionally, Governments have also scrambled--and, in some cases, fumbled--to assemble a proper response to the virus. Some have all by halted business operations in their countries, including Italy, which has extended restrictions on movement to the entire nation: the New York Times reported that Prime Minister Giuseppe Conte has "[banned] public gatherings and [asked] people not to travel except for work or emergencies."

Further market disruptions could be underway

If Italy's movements toward further restriction are any indication of what other governments may institute across the globe, then it may be likely that the virus will continue to disrupt financial markets.

Of crouse, "we're accustomed to volatility in crypto markets, so for those of us who've been on the rollercoaster ride, it's more of the same," she added.

Indeed, while Bitcoin shed roughly 14 percent of its value over the weekend, it had only been several months since a quick drop of a similar size had occurred; on the other hand, a drop matching Brent Crude's 30 percent fall on Monday hadn't been seen since January 17th, 1991, the starting day of the first Gulf War.

Therefore, "for macro markets, volatility is going to be a tricky thing to manage, and we're already seeing implosions and explosions like the VIX blowout on Friday," Ms. Demirors said, referring to CBOE's real-time market index that represents market expectations of forward-looking volatility for the next 30 days.

The index, which has been nicknamed the "fear gauge," spiked between Friday and Monday, peaking at 62.12 on Monday morning, its highest level since the financial crisis, when it rose to 89.53.

The world may "see the failure of monetary policy"

All of these factors seem to indicate that in the longer term, "we [will] see the failure of monetary policy," Ms. Demirors said.

"Since the crisis in 2009, the approach taken by global central banks has been to lower rates and print more money," she explained. Indeed, "since 2009, the US money supply has more than tripled," even when printing between November 2019 and March 2020 isn't counted. At the same time, interest rates in the US "have tumbled."

This has led to a kind of breaking point. "With over 25% of sovereign debt yielding negative interest, we are seeing central bankers rapidly running out of tools in their toolkit, because the tools no longer work," Ms. Demirors said.

Looks like a global coordinated monetary policy response to coronavirus by CenBanks is in the offing. BOE pledges to take needed steps to protect stability amid virus. Verbal intervention first started w/a surprise Fed statement. BoJ also released a similar statement today. pic.twitter.com/2d07sSkSmc

— Holger Zschaepitz (@Schuldensuehner) March 2, 2020

"The question then becomes what other measures they will take," she continued. "Here we see concerning signs, with the Fed indicating they may look to buy corporate bonds."

Indeed, the New York Timesreported that Eric Rosengren, the president of the Federal Reserve Bank of Boston, suggested during a recent speech that "officials may need to buy assets other than government bonds to counter the next downturn," a move that may require legislative changes, and could result in even lower interested rates. This could eventually lead to negative rates, which, although they are "used in Japan and parts of Europe, probably would not work well in the United States."

"The real question is when and how the crisis in the stock market will be expressed."

Monetary policy in the United States could also eventually fail because of the amount of USD liquidity that could potentially flood the market: "there are trillions of dollars of 'dry powder' sitting on the sidelines," she pointed out, citing figures from alternative finance data firm Preqin.

"There is $1.5 trillion of cash in private equity and venture capital funds that need to be deployed," with "the bulk, $1.4 trillion, in private equity."

All of this, in Ms. Demirors' opinion, points to a rather grim ending: "we are certainly headed into a recession, meaning a period of economic contraction, versus the period of economic expansion we have been in the last 11 years," she said.

However, "in terms of crisis or depression, I don't believe we are there yet," she added. Indeed, "if we look at typical signifiers of a crisis or depression," they just aren't there--at least, not yet.

"We haven't seen unemployment rise (yet) – in fact, we are at record employment levels, we have not yet seen a sustained fall in output or GDP, and projections still have GDP across the world expected to rise, albeit at 1% as opposed to 2-3%," Ms. Demirors explained.

Additionally, "deflation in key stores of wealth such as home values and other long-term 'safe haven' assets hasn't hit yet."

"The real question is when and how the crisis in the stock market will be expressed across labor, growth, and long-term asset prices."

Is Bitcoin a safe haven or not? The answer could be somewhere in the middle

But how could the longer-term trajectory of these traditional financial markets affect the longer-term trajectory of the price of Bitcoin?

After all, the price movements of BTC in the wake of the spread of the coronavirus have, to a large extent, upended expectations about the role that Bitcoin will play in the wake of the global financial crisis. Many industry insiders have long expected that Bitcoin will act as a 'safe haven,' and will rise in the face of uncertainty. However, it seems--at least, so far--that the opposite is closer to the truth.

Indeed, a spokesperson from Digital Asset Investment Management (DAiM), the self-styled "first licensed registered investment advisor for Bitcoin and digital assets," told Finance Magnates that although "the conversation and questions about Bitcoin over the past few weeks have centered around, 'is it a safe haven or not a safe haven?'," the reality is that the question isn't so simple.

"In our opinion, the truth is somewhere in the middle," DAiM's spokesperson said. "Bitcoin is absolutely a speculative risk asset and an emerging speculative store of value."

"Any time markets experience fear, uncertainty, and volatility; risk assets trade with a near correlation of zero as investors tend to sell off anything liquid that isn't nailed down," which "includes Bitcoin."

"That being said, Bitcoin doesn't need a perfect inverse relationship against risk assets to prove its usefulness as an emerging store of value or its well-earned place in your overall portfolio as a noncorrelated asset and future form of money."

DAIM also pointed out that "despite its recent weakness, Bitcoin is up more than seven percent on the year while equities are down [roughly] 15 percent."

If you're looking for bearish narratives, there are currently 3 that could be impacting #bitcoin 1.) Coronavirus (all markets selling off) 2.) Miner hoarding (typically strong bearish indication) 3.) PlusToken scam dumping on the market again. (They moved 19k bitcoin yesterday)

"Bitcoin will find a bottom long before stocks do."

But can Bitcoin manage to hold onto the progress that it has made this year, or will the price continue to decline?

DAIM believes that much like other financial markets, Bitcoin's trajectory heavily depends on the ways that the virus is handled as a public health crisis: that in the best case, Bitcoin--along with other financial markets--will react positively to a swift and effective government response that will contain the spread of the coronavirus.

A disease specialist in Seattle had the ability (and instinct) to test for coronavirus as early as January.

This kind of action would "[calm] the markets, and [reduce] the fear of this spiraling into a larger outbreak, which would only cause a more violent and protracted economic slowdown," DAiM said. "The best-case scenario for Bitcoin is that once the dust settles, that it begins decoupling from risk assets, it resumes its noncorrelated performance as a non-sovereign, hard-capped, fixed-supply, immutable store of value."

However, in the worst-case scenario (or even a worst-case scenario), there could be some bigger bumps in the road--again, depending largely on the way that governments manage to handle the outbreak: "while we are not experts in epidemiology, it is our contention that if coronavirus maintains its current trajectory and continues to disrupt global markets, it's more than likely that Bitcoin will be negatively affected," DAiM said.

This is because "speculative capital will likely sell first, ask questions later."

The logo of Digital Asset Investment Management (DAiM), the self-styled "first licensed registered investment advisor for Bitcoin and digital assets."

That being said, DAiM believes that "Bitcoin will find a bottom long before stocks do."

Still, the long-term effects of the coronavirus and the surrounding governmental response are very difficult to predict.

"We will get through this, but at what cost? Will we react fast enough to protect our people and humans of the world? Will the monetary and fiscal policies of central banks and governments be misguided, focusing on saving markets and softening the blow against GDP growth decline and the potential for any sort of recession, rather than care for humans and saving lives?", DAiM asked.

"It's too early to know, but if history is a guide, massive change is coming."

Rachel is a self-taught crypto geek and a passionate writer. She believes in the power that the written word has to educate, connect and empower individuals to make positive and powerful financial choices. She is the Podcast Host and a Cryptocurrency Editor at Finance Magnates.

CoinRoutes Adds Dedicated Wincent FIX Sessions for Institutional Clients

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.