Crypto exchange Bybit will enforce mandatory KYC to access all of its products and services.

This is no less than a Cultural conflict, as Crypto has always rejected the notion of proving one’s identity.

Crypto, perhaps rebranded as the more respectable-sounding web3, steers ever closer toward mainstream integration. Is it a given that certain tenets that have always been central to the crypto space may start to be edged out as they are incompatible with traditional and legally compliant operating methods?

Regarding financial operations and anti-money laundering requirements, know-your-customer (KYC) protocols are a regulatory expectation. Yet, up to now, crypto has operated in a gray area, or at least an inconsistent one, with different platforms and services employing systems that are not always aligned.

However, the direction of movement, particularly for centralized exchanges, appears only to be in one direction, towards a greater emphasis on unavoidable KYC procedures for customers, as evidenced recently by changes taking place at the trading exchange, Bybit.

What's Happening at Bybit?

A recent announcement from the major crypto exchange detailed its plans to enforce mandatory KYC on all users to access its products and services. This new arrangement will start today and affect both new and existing customers.

Notably, the first two reasons given by Bybit for enforcing this change are "security and compliance" and "prevent illegal activities". In addition, there are reasons given that relate to improving the user experience, including "enhanced services", "exclusive offers", and "convenience and security".

Notably, Bybit is taking an overall approach in which KYC must use any aspect of its platform, which is not the case with all of its competitors.

Trading without KYC

After Bybit has changed its approach, there will still be some well-known platforms that allow some of their trading services to be accessed without KYC completion, including OKX and KuCoin, both of which allow non-KYC cryptocurrency withdrawals.

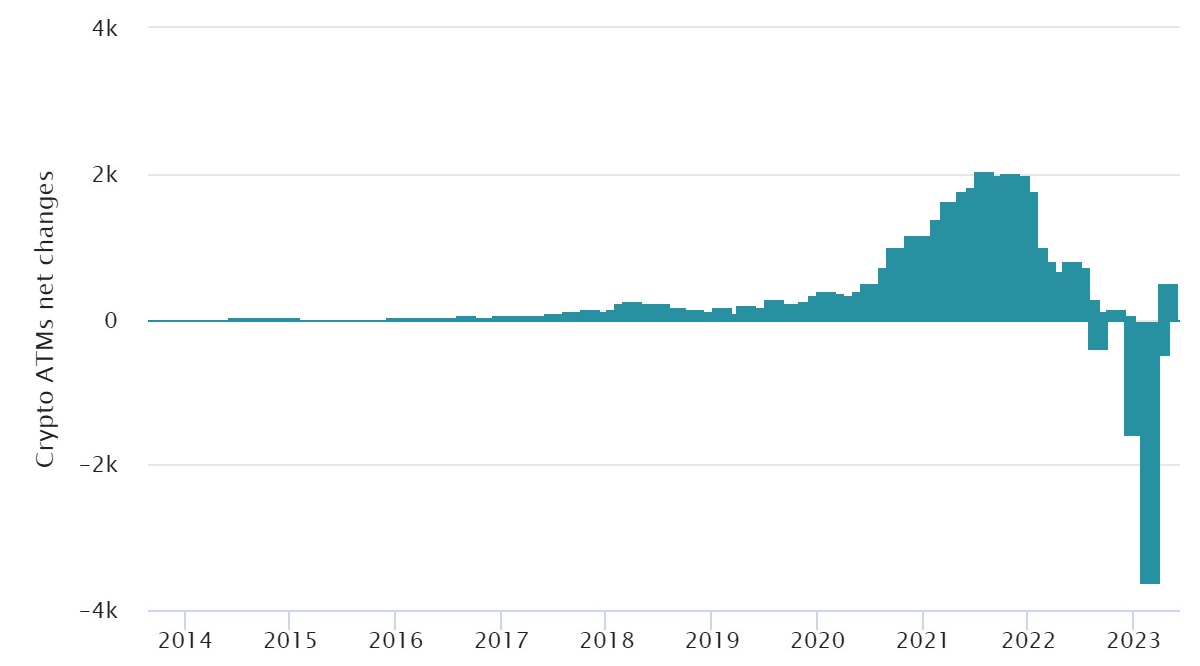

Crypto ATMs and peer-to-peer trades are also still options. However, ATM installation has stalled. Earlier this year, the longstanding platform LocalBitcoins, which acted as a means for buyers and sellers to find one another, closed down due to a lack of market demand for its services after more than ten years in operation. This closure, which is coming at the same time as the EU's MiCA, arguably marks the end of a crypto era as the entire ecosystem shifts in from the fringes.

Chart from Coin ATM Radar

That said, decentralized exchanges such as Uniswap and Sushi remain faithful to the spirit of the tech, requiring neither permission nor verification and no trusted third parties to use their protocols. However, what can't be done on these platforms is cashing out to fiat, and it's at this contact point with traditional finance that most users find themselves subject to orthodox formalities.

Uniswap and Sushi are integrated with fiat on-ramps to allow crypto purchases (through MoonPay and Transak, respectively); these integrated providers enforce their own KYC processes.

Mastercard and Web3 Verification

One giant of traditional finance executing a web3 strategy is Mastercard, and, just as it is occurring at crypto-native exchanges, it's also emphasizing user verification.

Mastercard has demonstrated its interest in crypto and web3 through its Mastercard Artist Accelerator, which uses NFTs on Polygon to connect musical talent with the digital economy, and through a partnership with web3 payment protocol Immersive.

Accordingly, Mastercard has created a standards and infrastructure package called Mastercard Crypto Credential, which aims to facilitate user verification across blockchain networks. The idea is that this system allows varying regulatory standards to be met, errors reduced, and consumer experiences improved.

These developments are being worked on in collaboration with blockchain organizations, including The Solana Foundation, Polygon Labs, Aptos Labs, and several crypto wallet providers.

1/ The future of identity is Web3—and Aptos Labs is partnering with @Mastercard to make that future a reality with Mastercard Crypto Credential, an on-chain identity and verification framework with a variety of applications in payments, remittances, ticketing, and NFTs! pic.twitter.com/4vUwylialQ

Mastercard's announcement talks about "instilling trust in the blockchain ecosystem", but this brings to mind a possible contrast with a founding ideal in crypto of a trustless system, meaning one in which it's not necessary to trust anyone, neither counterparty nor third party since the blockchain network itself enables hard-coded mechanisms for verification instead.

A Clash of Cultures?

Perhaps it's inevitable that as traditional finance and cryptocurrencies shift into a closer shared orbit, clashes in culture, and methods of operation, will become apparent. Crypto has always, at its core, rejected the notion of proving one's identity, and safeguarding the freedom to transact without permission has been a key driver in its development.

When it comes to decentralized exchanges, these ideals are built in, and in the case of peer-to-peer transactions, no third parties or permissioned rails are required.

However, trade-offs are taking place at centralized exchanges and when interacting with non-crypto consumer environments to comply with financial norms and operate above-board platforms. If these adaptations bring in new users and greater adoption, there will, perhaps, be few complaints.

However, there is the potential that once a new user is acquainted with crypto, they may find themselves wandering from centralized entities to decentralized protocols and, in the process, picking up on those founding elements, decentralization, and trustless systems, that crypto was always intended to enable.

Crypto, perhaps rebranded as the more respectable-sounding web3, steers ever closer toward mainstream integration. Is it a given that certain tenets that have always been central to the crypto space may start to be edged out as they are incompatible with traditional and legally compliant operating methods?

Regarding financial operations and anti-money laundering requirements, know-your-customer (KYC) protocols are a regulatory expectation. Yet, up to now, crypto has operated in a gray area, or at least an inconsistent one, with different platforms and services employing systems that are not always aligned.

However, the direction of movement, particularly for centralized exchanges, appears only to be in one direction, towards a greater emphasis on unavoidable KYC procedures for customers, as evidenced recently by changes taking place at the trading exchange, Bybit.

What's Happening at Bybit?

A recent announcement from the major crypto exchange detailed its plans to enforce mandatory KYC on all users to access its products and services. This new arrangement will start today and affect both new and existing customers.

Notably, the first two reasons given by Bybit for enforcing this change are "security and compliance" and "prevent illegal activities". In addition, there are reasons given that relate to improving the user experience, including "enhanced services", "exclusive offers", and "convenience and security".

Notably, Bybit is taking an overall approach in which KYC must use any aspect of its platform, which is not the case with all of its competitors.

Trading without KYC

After Bybit has changed its approach, there will still be some well-known platforms that allow some of their trading services to be accessed without KYC completion, including OKX and KuCoin, both of which allow non-KYC cryptocurrency withdrawals.

Crypto ATMs and peer-to-peer trades are also still options. However, ATM installation has stalled. Earlier this year, the longstanding platform LocalBitcoins, which acted as a means for buyers and sellers to find one another, closed down due to a lack of market demand for its services after more than ten years in operation. This closure, which is coming at the same time as the EU's MiCA, arguably marks the end of a crypto era as the entire ecosystem shifts in from the fringes.

Chart from Coin ATM Radar

That said, decentralized exchanges such as Uniswap and Sushi remain faithful to the spirit of the tech, requiring neither permission nor verification and no trusted third parties to use their protocols. However, what can't be done on these platforms is cashing out to fiat, and it's at this contact point with traditional finance that most users find themselves subject to orthodox formalities.

Uniswap and Sushi are integrated with fiat on-ramps to allow crypto purchases (through MoonPay and Transak, respectively); these integrated providers enforce their own KYC processes.

Mastercard and Web3 Verification

One giant of traditional finance executing a web3 strategy is Mastercard, and, just as it is occurring at crypto-native exchanges, it's also emphasizing user verification.

Mastercard has demonstrated its interest in crypto and web3 through its Mastercard Artist Accelerator, which uses NFTs on Polygon to connect musical talent with the digital economy, and through a partnership with web3 payment protocol Immersive.

Accordingly, Mastercard has created a standards and infrastructure package called Mastercard Crypto Credential, which aims to facilitate user verification across blockchain networks. The idea is that this system allows varying regulatory standards to be met, errors reduced, and consumer experiences improved.

These developments are being worked on in collaboration with blockchain organizations, including The Solana Foundation, Polygon Labs, Aptos Labs, and several crypto wallet providers.

1/ The future of identity is Web3—and Aptos Labs is partnering with @Mastercard to make that future a reality with Mastercard Crypto Credential, an on-chain identity and verification framework with a variety of applications in payments, remittances, ticketing, and NFTs! pic.twitter.com/4vUwylialQ

Mastercard's announcement talks about "instilling trust in the blockchain ecosystem", but this brings to mind a possible contrast with a founding ideal in crypto of a trustless system, meaning one in which it's not necessary to trust anyone, neither counterparty nor third party since the blockchain network itself enables hard-coded mechanisms for verification instead.

A Clash of Cultures?

Perhaps it's inevitable that as traditional finance and cryptocurrencies shift into a closer shared orbit, clashes in culture, and methods of operation, will become apparent. Crypto has always, at its core, rejected the notion of proving one's identity, and safeguarding the freedom to transact without permission has been a key driver in its development.

When it comes to decentralized exchanges, these ideals are built in, and in the case of peer-to-peer transactions, no third parties or permissioned rails are required.

However, trade-offs are taking place at centralized exchanges and when interacting with non-crypto consumer environments to comply with financial norms and operate above-board platforms. If these adaptations bring in new users and greater adoption, there will, perhaps, be few complaints.

However, there is the potential that once a new user is acquainted with crypto, they may find themselves wandering from centralized entities to decentralized protocols and, in the process, picking up on those founding elements, decentralization, and trustless systems, that crypto was always intended to enable.

Sam White is a writer and journalist from the UK who covers cryptocurrencies and web3, with a particular interest in NFTs and the crossover between art and finance. His work, on a wide variety of topics, has appeared on platforms including The Spectator, Vice and Hacker Noon.

Bybit Uses Tokenised Equities as Underlyings for Structured Yield

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.