>

A Look Back At Trading Volumes: FX Industry Hangs Tough As 2013 Bows Out

A Look Back At Trading Volumes: FX Industry Hangs Tough As 2013 Bows Out

Tuesday,31/12/2013|10:00GMTby

Andrew Saks McLeod

Although 2013 brought good fortune to many FX firms, it was not a time for companies to rest on their laurels. On the contrary, as volumes increased, strategic corporate decisions were taken to move the industry on.

High hopes for 2013 were certainly held by senior executives across the FX industry's boardrooms one year ago, with many a company likely concerned that a repeat of 2012's industry-wide low volume and trading activity would not recur during what was then looked upon as a year ahead of hope and recovery.

Japan Remains Retail FX Powerhouse

Most certainly, 2013 began by delivering a complete U-turn from 2012's array of poor corporate results, and then some. In a few cases, especially within the retail sector, not only a recovery surfaced, but indeed a total reversal in trading volume, resulting in a great many companies, especially in Japan, experiencing all-time records in trading volume, including DMM Securities and GMO Click having both declared $1 trillion dollar volumes for the first time since their establishment.

MONEX Group's results this year, although falling short of the $1 trillion mark, rose to an unprecedented high in August 2013, in the form of a 33% spike in trading activity from a year earlier, having recovered from a minor dip during June this year where the company experienced a 12.9% decline in volumes compared with the previous month, at the same time as its compatriots enjoyed a period of record volumes.

Subsequently, MONEX Group's interim dividend for the period ending March 31, 2014 was set to be ten times higher than that of the previous accounting period. Despite the high dividend which reflects overall growth, the company's extremely high increase in fortunes within the Japanese market began to dwindle as the third quarter of the year progressed, leaving its US subsidiary TradeStation to produce steadily increasing volumes.

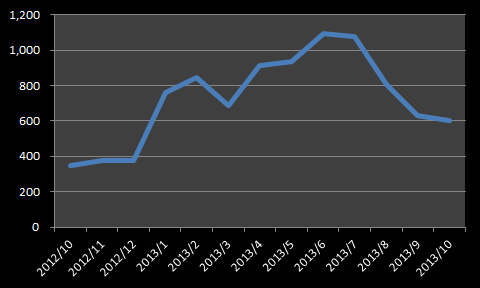

GMO Click Trading Volumes Peaked At Over S1 Trillion, Before Tailing Off In October

Western firms' figures echoed this dynamic, albeit to a lesser extent, however the third quarter of the year represented the slowing down of the high monthly results, and as summer gave way to fall, a protraction began to surface across all retail firms, with some institutional contenders feeling the pinch also, showing that firms made hay whilst the sun shone.

Alpari's combined volumes peaked at $250 billion during October this year, laying testimony to the success garnered by the firm's steady metamorphosis into what is now one of the largest retail FX firms in the world. The company experienced a steady increase in trading activity across a sustained period, which encompassed the majority of the summer months, despite the firm having retracted from the US market during that period.

Indeed, with a very well-developed and active network of introducing brokers and representatives in the Asia-Pacific region, the company shares market dominance with FXCM and FXDD among Far Eastern investors which are referred by introducing brokers in that particular region.

With the often prohibitively high operating costs and $20 million net capital adequacy requirement associated with operating in the United States, Alpari is now unburdened with such considerations, and perhaps spurred on by the 61% increase in volumes during October within the company's Russian operations, the company heads into the new year in a strong position.

FXCM Dominates in North America, Despite Q3 Loss

Although the comparatively enormous cost of operating in the United States has precluded many retail firms from sustaining a viable business, FXCM continued to dominate the largest free-market economy on earth during 2013.

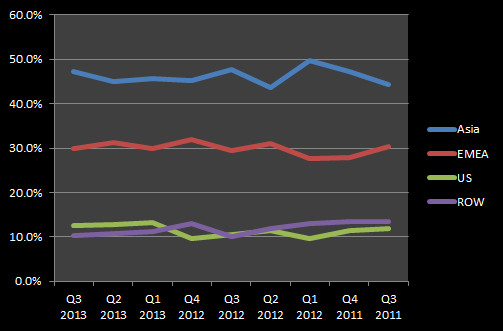

FXCM Regional Retail Volume Percentages

As a public company, shareholders were subjected to witnessing a US GAAP net loss of $5.1 million on revenues of $113.2 million during October, which were 19.2% below Q2 2013. However, retail volumes in October rose 11% from September to $315 billion.

Although the firm's retail volumes exceeded those of contemporary Alpari during October, the outcome of FXCM's overall loss was a 4% dip in its stock prices on November 7, following the company's announcement of its October results.

The company's institutional business fared well, having built steadily on its increasing volumes, as depicted by average institutional trading volume per day during August this year being a staggering 332% higher than that achieved by the company in August 2012.

Post-M&A Strength

Mergers and acquisitions between large, established firms have been a major theme for the FX industry during 2013, and were a contributing factor toward higher reported volumes for companies which invested in buying either a controlling interest in their peers, or completed an outright takeover.

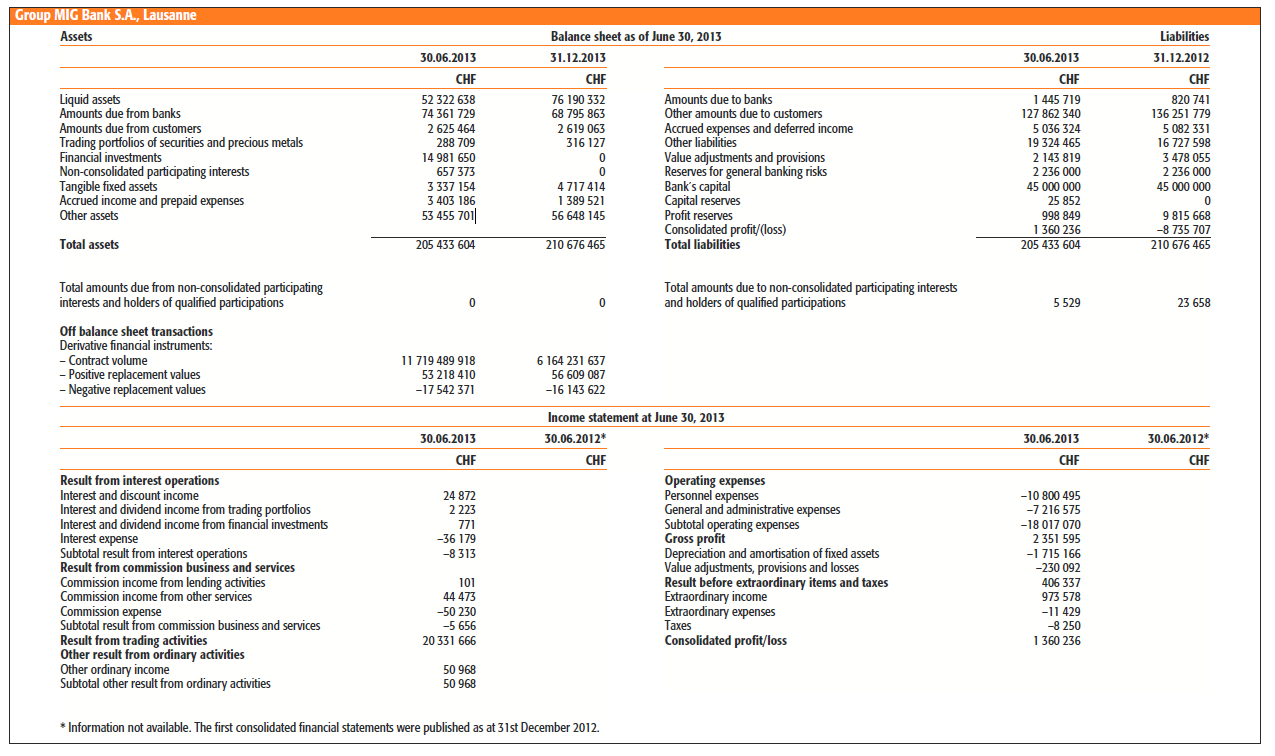

MIG Bank Was Acquired By Swissquote After Publishing These Results For First Six Months of 2013

MIG Bank was sold in its entirety to Swissquote as summer gave way to autumn, the company’s rationale having been to utilize this to greatly expand its FX operations, which was an important strategic move for the firm with FX volumes of CHF 158 billion accounting for 26.2 percent of total net revenues in the first half of 2013.

On this basis, the results for the first nine months of this year detail an increase in the number of accounts by 6.9 percent to 215,237.

The total deposit for this period weighed in at CHF 9,582 million, 11.8 percent higher than that of the same period one year previous. Furthermore, Swissquote has stated that the results for the fourth quarter show FX earnings generated by MIG Bank, which is the first time the company has included this since the acquisition, and has contributed to the positive cumulative return.

GAIN Capital's purchase of GFT may be regarded as a strategic rebuttal of FXCM's unsolicited intention to acquire it lock, stock and barrel, however it too generated a stronger client base and therefore positively affected trading volumes, with a view toward diversifying the firm's reach in the coming year.

On the institutional side, Knight Capital completed its merger with GETCO, bolstering the company's balance sheet with a $128 million one-off net gain as a result of GETCO’s investment in the US-based parent company of FX firm Hotspot FX, thus contributing to KCG having reported net income of $226.8 million and diluted earnings per share of $1.98 for the three months ended September 30, 2013.

At the time that KCG released its figures for the third quarter of this year, it was clear that certain aspects of its business activity other than regular FX order flow has performed remarkably well, when considering the overall tailing off of volumes that other companies have experienced in the same period.

Prior to announcing the company’s net gain resulting from GETCO’s investment, KCG’s commercial offerings were producing more than satisfactory results, with record highs for market share in the categories covering algorithmic and EMS U.S. equity execution, institutional spot foreign exchange and inter-dealer corporate bond transactions.

Going For Gold

Trading venues in emerging markets began to prove their mettle this year, exemplified by the Dubai Gold and Commodities Exchange (DGCX), which relies very strongly on its Indian Rupee contract.

Despite demand for other currencies such as the Euro and Yen the exchange arrived at the end of July with a 91% increase in volume since January.

“The product has been attracting growing attention from international institutional participants, ranging from multinational banks, non-deliverable forward (NDF) markets, traders and other business entities. Building on this success, DGCX is exploring the introduction of new futures contracts in Emerging Market (EM) currencies.”

This somewhat niche product has served the DGCX well, and as a relative newcomer to the market, has proved essential. Contrary to this, some of the established venues did not fare so well, with ICE's volumes experiencing a 45% slump in average daily volumes to 20,440 contracts in October, compared to 36,863 in the previous month.

All Clear On The Western Front

In terms of FX clearing and settlement, a good measure of order flow within the institutional segment is to examine the trades cleared by external firms.

Indeed, according to data published earlier this week by CLS Bank, the firm's average daily volumes fell 2.2% from October to $4.89 trillion from $5 trillion (volumes are double counted representing both sides of the trade being submitted for settlement).

The month-over-month contrasted with reports from public reporting venues such as the CME, EBS, Thomson Reuters and KCG Hotspot, which all saw volumes improvements during November.

With 2014's imminent commencement, the entire industry not only forms a different structure to that of one year ago, but also looks back on 2013 as a fruitful year of sustained highs, counteracted by relatively moderate lows, and can certainly be considered a world away from the doldrums which plagued the entire FX industry worldwide during 2012.

Onwards and upwards, as they say....

High hopes for 2013 were certainly held by senior executives across the FX industry's boardrooms one year ago, with many a company likely concerned that a repeat of 2012's industry-wide low volume and trading activity would not recur during what was then looked upon as a year ahead of hope and recovery.

Japan Remains Retail FX Powerhouse

Most certainly, 2013 began by delivering a complete U-turn from 2012's array of poor corporate results, and then some. In a few cases, especially within the retail sector, not only a recovery surfaced, but indeed a total reversal in trading volume, resulting in a great many companies, especially in Japan, experiencing all-time records in trading volume, including DMM Securities and GMO Click having both declared $1 trillion dollar volumes for the first time since their establishment.

MONEX Group's results this year, although falling short of the $1 trillion mark, rose to an unprecedented high in August 2013, in the form of a 33% spike in trading activity from a year earlier, having recovered from a minor dip during June this year where the company experienced a 12.9% decline in volumes compared with the previous month, at the same time as its compatriots enjoyed a period of record volumes.

Subsequently, MONEX Group's interim dividend for the period ending March 31, 2014 was set to be ten times higher than that of the previous accounting period. Despite the high dividend which reflects overall growth, the company's extremely high increase in fortunes within the Japanese market began to dwindle as the third quarter of the year progressed, leaving its US subsidiary TradeStation to produce steadily increasing volumes.

GMO Click Trading Volumes Peaked At Over S1 Trillion, Before Tailing Off In October

Western firms' figures echoed this dynamic, albeit to a lesser extent, however the third quarter of the year represented the slowing down of the high monthly results, and as summer gave way to fall, a protraction began to surface across all retail firms, with some institutional contenders feeling the pinch also, showing that firms made hay whilst the sun shone.

Alpari's combined volumes peaked at $250 billion during October this year, laying testimony to the success garnered by the firm's steady metamorphosis into what is now one of the largest retail FX firms in the world. The company experienced a steady increase in trading activity across a sustained period, which encompassed the majority of the summer months, despite the firm having retracted from the US market during that period.

Indeed, with a very well-developed and active network of introducing brokers and representatives in the Asia-Pacific region, the company shares market dominance with FXCM and FXDD among Far Eastern investors which are referred by introducing brokers in that particular region.

With the often prohibitively high operating costs and $20 million net capital adequacy requirement associated with operating in the United States, Alpari is now unburdened with such considerations, and perhaps spurred on by the 61% increase in volumes during October within the company's Russian operations, the company heads into the new year in a strong position.

FXCM Dominates in North America, Despite Q3 Loss

Although the comparatively enormous cost of operating in the United States has precluded many retail firms from sustaining a viable business, FXCM continued to dominate the largest free-market economy on earth during 2013.

FXCM Regional Retail Volume Percentages

As a public company, shareholders were subjected to witnessing a US GAAP net loss of $5.1 million on revenues of $113.2 million during October, which were 19.2% below Q2 2013. However, retail volumes in October rose 11% from September to $315 billion.

Although the firm's retail volumes exceeded those of contemporary Alpari during October, the outcome of FXCM's overall loss was a 4% dip in its stock prices on November 7, following the company's announcement of its October results.

The company's institutional business fared well, having built steadily on its increasing volumes, as depicted by average institutional trading volume per day during August this year being a staggering 332% higher than that achieved by the company in August 2012.

Post-M&A Strength

Mergers and acquisitions between large, established firms have been a major theme for the FX industry during 2013, and were a contributing factor toward higher reported volumes for companies which invested in buying either a controlling interest in their peers, or completed an outright takeover.

MIG Bank Was Acquired By Swissquote After Publishing These Results For First Six Months of 2013

MIG Bank was sold in its entirety to Swissquote as summer gave way to autumn, the company’s rationale having been to utilize this to greatly expand its FX operations, which was an important strategic move for the firm with FX volumes of CHF 158 billion accounting for 26.2 percent of total net revenues in the first half of 2013.

On this basis, the results for the first nine months of this year detail an increase in the number of accounts by 6.9 percent to 215,237.

The total deposit for this period weighed in at CHF 9,582 million, 11.8 percent higher than that of the same period one year previous. Furthermore, Swissquote has stated that the results for the fourth quarter show FX earnings generated by MIG Bank, which is the first time the company has included this since the acquisition, and has contributed to the positive cumulative return.

GAIN Capital's purchase of GFT may be regarded as a strategic rebuttal of FXCM's unsolicited intention to acquire it lock, stock and barrel, however it too generated a stronger client base and therefore positively affected trading volumes, with a view toward diversifying the firm's reach in the coming year.

On the institutional side, Knight Capital completed its merger with GETCO, bolstering the company's balance sheet with a $128 million one-off net gain as a result of GETCO’s investment in the US-based parent company of FX firm Hotspot FX, thus contributing to KCG having reported net income of $226.8 million and diluted earnings per share of $1.98 for the three months ended September 30, 2013.

At the time that KCG released its figures for the third quarter of this year, it was clear that certain aspects of its business activity other than regular FX order flow has performed remarkably well, when considering the overall tailing off of volumes that other companies have experienced in the same period.

Prior to announcing the company’s net gain resulting from GETCO’s investment, KCG’s commercial offerings were producing more than satisfactory results, with record highs for market share in the categories covering algorithmic and EMS U.S. equity execution, institutional spot foreign exchange and inter-dealer corporate bond transactions.

Going For Gold

Trading venues in emerging markets began to prove their mettle this year, exemplified by the Dubai Gold and Commodities Exchange (DGCX), which relies very strongly on its Indian Rupee contract.

Despite demand for other currencies such as the Euro and Yen the exchange arrived at the end of July with a 91% increase in volume since January.

“The product has been attracting growing attention from international institutional participants, ranging from multinational banks, non-deliverable forward (NDF) markets, traders and other business entities. Building on this success, DGCX is exploring the introduction of new futures contracts in Emerging Market (EM) currencies.”

This somewhat niche product has served the DGCX well, and as a relative newcomer to the market, has proved essential. Contrary to this, some of the established venues did not fare so well, with ICE's volumes experiencing a 45% slump in average daily volumes to 20,440 contracts in October, compared to 36,863 in the previous month.

All Clear On The Western Front

In terms of FX clearing and settlement, a good measure of order flow within the institutional segment is to examine the trades cleared by external firms.

Indeed, according to data published earlier this week by CLS Bank, the firm's average daily volumes fell 2.2% from October to $4.89 trillion from $5 trillion (volumes are double counted representing both sides of the trade being submitted for settlement).

The month-over-month contrasted with reports from public reporting venues such as the CME, EBS, Thomson Reuters and KCG Hotspot, which all saw volumes improvements during November.

With 2014's imminent commencement, the entire industry not only forms a different structure to that of one year ago, but also looks back on 2013 as a fruitful year of sustained highs, counteracted by relatively moderate lows, and can certainly be considered a world away from the doldrums which plagued the entire FX industry worldwide during 2012.

Opetek Launches ARIUS, Pilots AI Reasoning Platform at Tier 1 Investment Bank

Featured Videos

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.