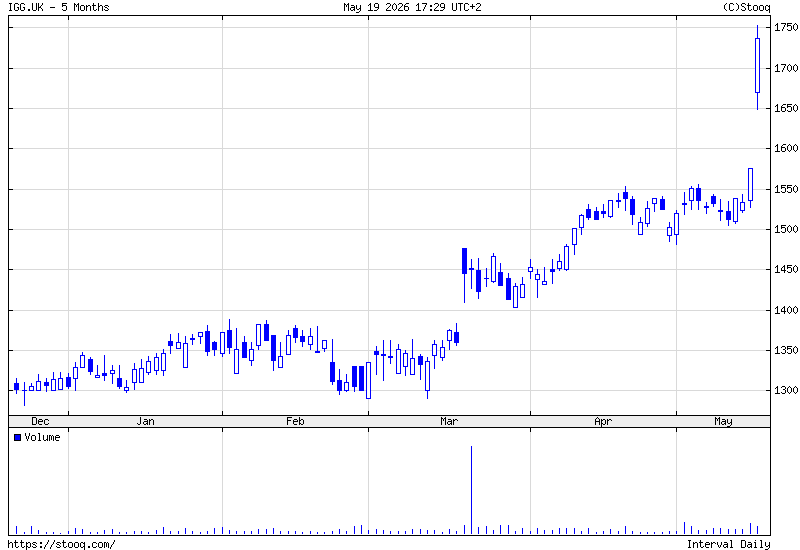

IG Group shares (LSE: IGG) closed at a record 1,742 pence on Tuesday, up almost 11% on the day, after the broker raised its full-year revenue guidance alongside its annual general meeting trading update and reported first-quarter organic revenue growth of 19%.

The move marks the sharpest single-session rally in IG's listed history outside the pandemic-era spikes and takes year-to-date gains above 30%, matching what the stock added across the whole of 2025.

IG entered the FTSE 100 on 23 March 2026 and has since outperformed the broader index by more than 30 percentage points.

Guidance Upgrade Closes the Gap to LTIP Stretch Targets

The numbers behind the rally were straightforward. Organic total revenue of £331.2 million for the three months to 31 March was about 10% ahead of the £300 million the broker had flagged in its pre-close note two months earlier. Active customers grew 12% organically, first trades rose 63%, and assets under administration crossed £20 billion in April.

- IG Group Lifts 2026 Revenue Guidance After Q1 Organic Sales Climb 19% to £331 Million

- “People Knocking on Our Door to See That We’re Here,” IG Group’s MENA CEO

- IG Group Is Taking More Risk, Staff Morale Is Negative, and CEO Earned £1.4 Million in Seven Months

What gives the upgrade more weight is what it implies for the company's 2028 plan. As FinanceMagnates.com reported in April, the long-term incentive plan granted to CEO Breon Corcoran and CFO Clifford Abrahams in September 2025 would only vest in full if revenue reaches £1.51 billion by 2028, implying a compound annual growth rate of 11.4% from the 2025 base.

IG Group 2026 Guidance | March 2026 | May 2026 |

Organic revenue growth | High single-digit | 10-15% |

Net interest income | £110m | £110-120m |

EBITDA margin | Mid-40s % | Mid-40s % |

Medium-term growth | Mid-to-high single-digit | At least 10% per year |

Tuesday's upgrade to 10-15% organic growth in 2026, with at least 10% compound growth beyond that, puts the LTIP threshold of £1,226 million within comfortable reach and the £1.51 billion maximum target into a credible band, rather than a stretch case.

FM Intelligence Data Cements IG Among the Global Top Five

The IG share rally lands in a quarter when FM Intelligence's broker tracker recorded retail FX and CFD volumes at all-time highs, with active accounts across the named-broker cohort reaching 7.42 million and five separate brokers running monthly volumes above $1.5 trillion.

IG sits inside that top five. According to FM Intelligence data, the broker recorded around $1.65 trillion in average monthly trading volume in Q1 2026, alongside roughly 173,000 active accounts in the cohort, up from approximately 149,000 in Q4 2025.

The 16% sequential increase in client count came against headline monthly volumes that ran broadly flat quarter-on-quarter on the FM Intelligence reading.

That contrast matters. Net trading revenue rose 17% QoQ to £306.5 million on IG's own books even as platform-level volumes were stable, which points to a mix shift toward higher-monetization activity rather than pure throughput.

The company itself flagged that OTC customer income retention reached the mid-80s percentage range in Q2 to date, up from 83% at the full-year stage.

IG has held a top-five position in the FM Intelligence cohort consistently since 2021, though it lost market share over the four-year period as the broader sample expanded faster. The Q1 numbers suggest that erosion may have stopped.

Peers Posted Strong Q1s, But IG Got the Sharpest Stock Reaction

Tuesday's move was disproportionate to the news on a peer-relative basis. Plus500 lifted its full-year guidance in April after Q1 revenue rose 18% to $242 million, and its shares are up roughly 16% year-to-date.

XTB reported an 88.5% Q1 revenue jump and a 176% rise in net profit, with the Polish stock up around 12% since the start of the year.

IG's 30%-plus year-to-date move outpaces both. Part of the explanation is positioning. Expectations into the AGM were anchored on the March pre-close, which guided high single-digit organic growth. The actual Q1 read implied something closer to mid-teens, with Q2 active customer growth accelerating beyond 12% in the first seven weeks.

UBS, which upgraded IG to Buy with a 1,600 pence target earlier this quarter, has now seen its price target overtaken by the stock itself. Consensus analyst target prices sit below the current share price after Tuesday's move.

Strategic Review Still the Bigger Catalyst

The autumn 2026 strategy update remains the larger swing factor. The board confirmed alongside the full-year results in March that the review will evaluate acquisitions, IG's domicile and listing venues, and possible combinations of group divisions with other industry participants.

Bloomberg reported earlier this year that a relisting from London to New York is among the options being weighed. Tuesday's record close suggests the market is starting to price in a constructive outcome rather than a defensive one.

The £125 million buyback launched on 1 April continues in the background, with 987,160 shares repurchased for £14.9 million by 15 May.

Interim results for the six months to 30 June are due on 31 July, with the strategy update to follow in the autumn.