The company’s CEO Drew Niv highlighted in the conference call after the FXCM Inc earnings report yesterday that the firm intended to repay its loan to Leucadia National by the end of 2015 primary through assets sales.

After FXCM Inc (NYSE:FXCM) reported its earnings and trading volumes figures yesterday, the company’s CEO Drew Niv and CFO Robert Lande have taken to the earnings call. FXCM’s senior management revealed crucial details about the company's future plans after the dramatic events of the 15th of January.

The main takeaway from the earnings call is that as expected, there will be a major restructuring of FXCM Inc's (NYSE:FXCM) business in the coming months. The company’s CEO Drew Niv outlined that aside from selling its institutional businesses, which was already clearly communicated by the firm, it intends to part with its FXCM Japan and FXCM Hong Kong subsidiaries.

In the aftermath of the Swiss National Bank’s decision to scrap the floor under the EUR/CHF, FXCM Inc (NYSE:FXCM) was forced to shore up its balance sheet. The company was forced to recapitalize, signing a $300 million loan agreement with Leucadia National with a starting interest rate of 10%, growing by 1.5% each quarter.

Revision of Losses from January 15th and Sale of FXCM Japan and Hong Kong

The company’s CEO, Drew Niv, highlighted during the earnings call that the firm intends to make significant reductions in its obligations to Leucadia National through the sale of non-core assets. The main surprise from this statement is in the details, as the CEO of FXCM Inc (NYSE:FXCM) stated that the firm decided to exit its business in Japan and Hong Kong.

Speaking during the earnings call, Mr. Niv said, “We have decided to exit the Japanese and Hong Kong retail markets selling our locally regulated subsidiary in each country. The sales will not only generate meaningful proceeds, but will also liberate over $50 million of cash which currently resides in these two entities.”

“We have multiple bids for each subsidiary and are seeing significant competition for these properties. We are in active discussions to select the best bid and move towards closing in the near future,” he explained.

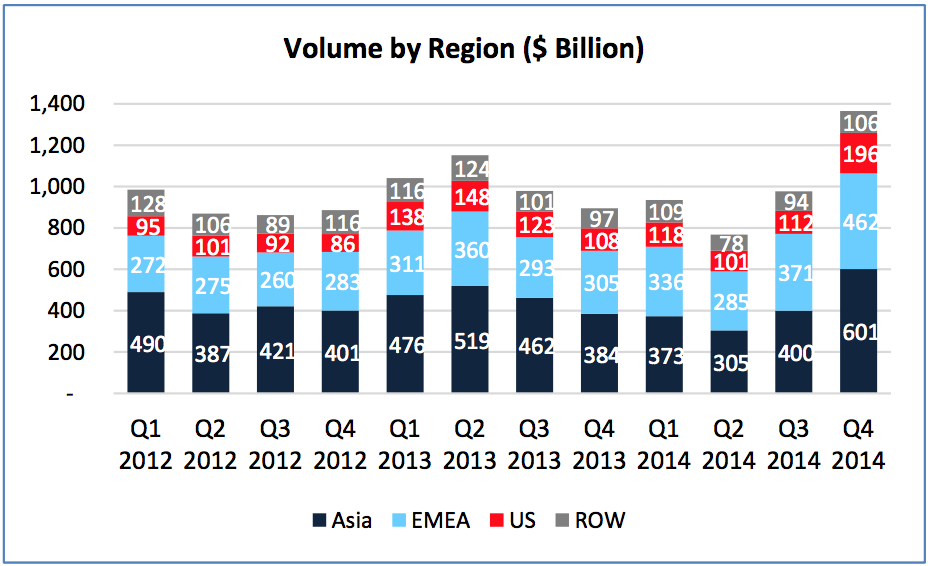

FXCM Trading Volume by Region, Source: FXCM

From the $50 million which Mr. Niv mentioned, $22 million in cash lie on the balance sheet of FXCM Japan, while the remaining $28 million are in the Hong Kong subsidiary of FXCM Inc.

The company's CEO Drew Niv stated, “We believe that the sale proceeds plus cash freed from the balance sheet of these entities could exceed $250 million, which would go a long way towards repaying if not fully repaying the Leucadia loan.”

Considering the lucrative Japanese market and the expansion appetite of many companies to acquire businesses in the region, the sale of this unit could net FXCM somewhere between $40 and $50 million.

The Hong Kong unit of the firm generated about $2.5 million in non-GAAP adjusted EBITDA in 2014. The jurisdiction and the lack of wide media coverage of the Swiss National Bank conundrum which FXCM faced, likely saved the value of the brand and clients continued to hold their accounts with the brokerage.

The main proceeds from potential sales will come from the non-core business of FXCM Inc (NYSE:FXCM). Back in 2012, FXCM acquired Lucid Markets for $176 million, with the estimated total costs of the investment totaling $192 million.

Considering the pressure under which FXCM is to sell its institutional business, and the outflow of institutional clients from FXCM, the company is not likely to recover its investment in this business.

The other big institutional business of FXCM, FastMatch, has experienced dwindling volumes in the aftermath of the Swiss National Bank debacle leading to decreased volumes.

FXCM owns 35% of FastMatch and the stake is on the sale list of the company alongside its high-frequency trading investment in V3. The company paid around $16 million for a 50.1 percent stake in V3, with the rest of the unit owned by Lucid Markets.

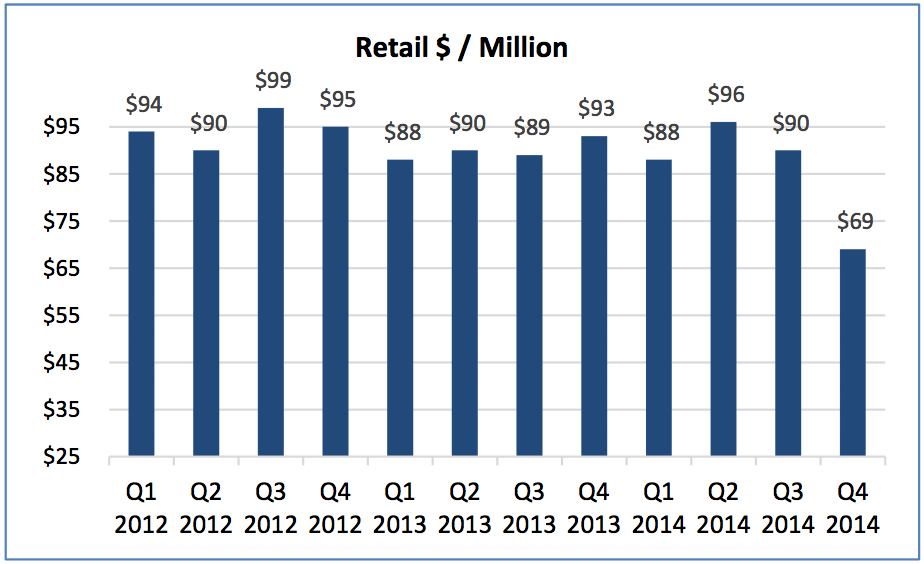

Retail Revenue per Million Drops to $69, Clients to Choose Dealing Desk or Not

FXCM Retail Revenue per Million, Source: FXCM

The retail revenues per million (RPM) which FXCM reported for the fourth quarter of 2014 totaled $69. This is $1 below the estimate which the company made in its previous earnings report.

In order to optimize its RPM, FXCM Inc (NYSE:FXCM) has announced that it will be returning the dealing desk model for clients with equity below $20,000.

The company’s CEO Drew Niv said during the earnings call, “To accelerate growth in our core business we will launch a hybrid desk model for small retail FX accounts. These are accounts with less than $20,000 of deposits. While these accounts maybe large in number, they still represent much less than half of our trading volume.”

After FXCM Inc (NYSE:FXCM) reported its earnings and trading volumes figures yesterday, the company’s CEO Drew Niv and CFO Robert Lande have taken to the earnings call. FXCM’s senior management revealed crucial details about the company's future plans after the dramatic events of the 15th of January.

The main takeaway from the earnings call is that as expected, there will be a major restructuring of FXCM Inc's (NYSE:FXCM) business in the coming months. The company’s CEO Drew Niv outlined that aside from selling its institutional businesses, which was already clearly communicated by the firm, it intends to part with its FXCM Japan and FXCM Hong Kong subsidiaries.

In the aftermath of the Swiss National Bank’s decision to scrap the floor under the EUR/CHF, FXCM Inc (NYSE:FXCM) was forced to shore up its balance sheet. The company was forced to recapitalize, signing a $300 million loan agreement with Leucadia National with a starting interest rate of 10%, growing by 1.5% each quarter.

Revision of Losses from January 15th and Sale of FXCM Japan and Hong Kong

The company’s CEO, Drew Niv, highlighted during the earnings call that the firm intends to make significant reductions in its obligations to Leucadia National through the sale of non-core assets. The main surprise from this statement is in the details, as the CEO of FXCM Inc (NYSE:FXCM) stated that the firm decided to exit its business in Japan and Hong Kong.

Speaking during the earnings call, Mr. Niv said, “We have decided to exit the Japanese and Hong Kong retail markets selling our locally regulated subsidiary in each country. The sales will not only generate meaningful proceeds, but will also liberate over $50 million of cash which currently resides in these two entities.”

“We have multiple bids for each subsidiary and are seeing significant competition for these properties. We are in active discussions to select the best bid and move towards closing in the near future,” he explained.

FXCM Trading Volume by Region, Source: FXCM

From the $50 million which Mr. Niv mentioned, $22 million in cash lie on the balance sheet of FXCM Japan, while the remaining $28 million are in the Hong Kong subsidiary of FXCM Inc.

The company's CEO Drew Niv stated, “We believe that the sale proceeds plus cash freed from the balance sheet of these entities could exceed $250 million, which would go a long way towards repaying if not fully repaying the Leucadia loan.”

Considering the lucrative Japanese market and the expansion appetite of many companies to acquire businesses in the region, the sale of this unit could net FXCM somewhere between $40 and $50 million.

The Hong Kong unit of the firm generated about $2.5 million in non-GAAP adjusted EBITDA in 2014. The jurisdiction and the lack of wide media coverage of the Swiss National Bank conundrum which FXCM faced, likely saved the value of the brand and clients continued to hold their accounts with the brokerage.

The main proceeds from potential sales will come from the non-core business of FXCM Inc (NYSE:FXCM). Back in 2012, FXCM acquired Lucid Markets for $176 million, with the estimated total costs of the investment totaling $192 million.

Considering the pressure under which FXCM is to sell its institutional business, and the outflow of institutional clients from FXCM, the company is not likely to recover its investment in this business.

The other big institutional business of FXCM, FastMatch, has experienced dwindling volumes in the aftermath of the Swiss National Bank debacle leading to decreased volumes.

FXCM owns 35% of FastMatch and the stake is on the sale list of the company alongside its high-frequency trading investment in V3. The company paid around $16 million for a 50.1 percent stake in V3, with the rest of the unit owned by Lucid Markets.

Retail Revenue per Million Drops to $69, Clients to Choose Dealing Desk or Not

FXCM Retail Revenue per Million, Source: FXCM

The retail revenues per million (RPM) which FXCM reported for the fourth quarter of 2014 totaled $69. This is $1 below the estimate which the company made in its previous earnings report.

In order to optimize its RPM, FXCM Inc (NYSE:FXCM) has announced that it will be returning the dealing desk model for clients with equity below $20,000.

The company’s CEO Drew Niv said during the earnings call, “To accelerate growth in our core business we will launch a hybrid desk model for small retail FX accounts. These are accounts with less than $20,000 of deposits. While these accounts maybe large in number, they still represent much less than half of our trading volume.”

ASIC Removed 87 Firms and Individuals From Financial Services Last Year, Up From 58

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.