>

Global FX Market Regulation | Part 1 – A Big Dream That Requires Even Bigger Ambition

Global FX Market Regulation | Part 1 – A Big Dream That Requires Even Bigger Ambition

Friday,12/09/2014|03:00GMTby

George Tchetvertakov

With the majority of financial services under regulatory oversight across the globe, could now be the time when the FX market finally comes in from the cold? In a special two part series Forex Magnates reports.

The Foreign Exchange (FX) market is currently under the microscope. Regulatory agencies from Switzerland, Germany, Europe, US, UK and Australia are investigating how the FX market works in practice and whether it’s prudent to regulate it globally.

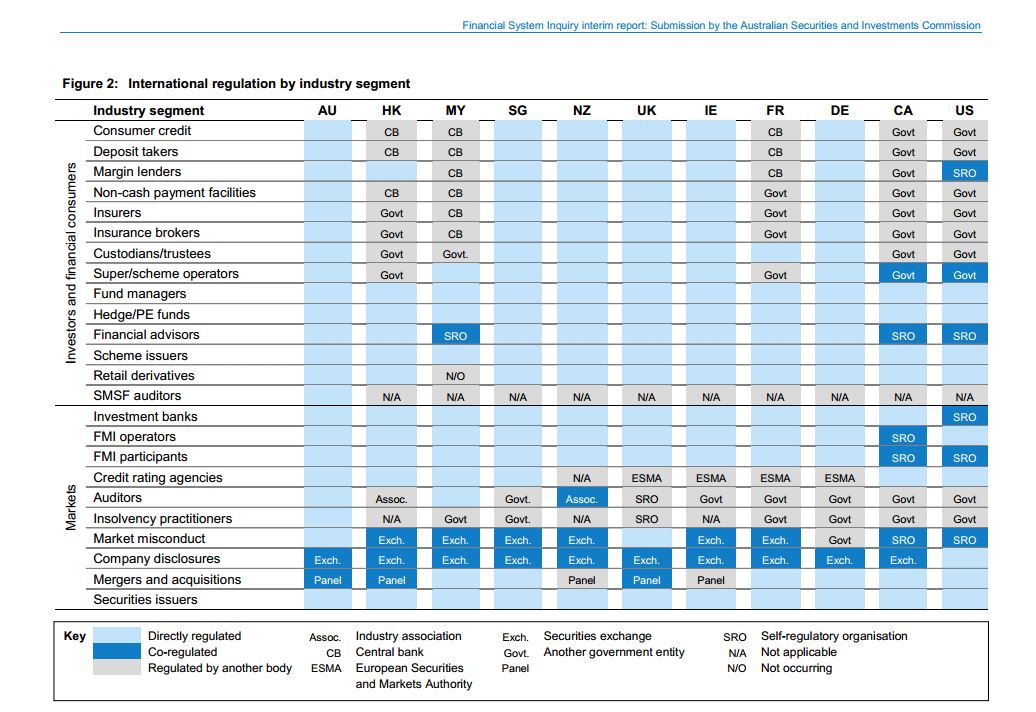

The FX market differs from all other asset classes in that in its current form, it is completely unregulated, operates over-the-counter, which means there is no central marketplace ,and is by far the largest by capitalization. So as regulators ponder ways to regulate this market, they first have to quantify and ring-fence its reach.

This is incredibly difficult to do because large currency transactions can take place as part of everyday life (property investment for example) and given fluctuating currency rates, people effectively speculate on currency movements without even being aware of it. With other asset classes this doesn’t apply.

Spot FX transactions are not regulated in any country, despite the assumption that the FCA, NFA, ASIC and others regulate financial services and by extension, the FX market which is part of the financial services landscape. In fact, what is actually regulated are FX derivatives such as CFDs, Futures and Options. In the case of the Financial Conduct Authority (FCA), spot FX contracts are not qualifying investments under The Financial Services and Markets Act (FSMA) and therefore, FX dealing cannot apply to the market abuse regime under and the FCA’s Code of Market Conduct guidelines. This is likely to factor into how banks defend their actions in response to FX manipulation allegations.

International Financial Markets Regulation by Industry Segment | Source: ASIC

Muzzled but Motivated

Despite the jurisdictional quagmire, some attempts have been made to reduce market abuse and mistreatment of private retail investors. The Commodities and Futures Commission (CFTC) created a special task force in 2008 to reign in unscrupulous brokers and introduced harsh penalties in 2010 to protect retail FX traders.

The knock-on effect has been for U.S traders to seek trading accounts elsewhere around the globe with lower margin requirements. Regulators seem to be creating bit-part solutions which human nature and technology find a way of avoiding before the ink is even dry on the regulatory amendment.

In the UK and Europe, regulation is limited and leverage is unrestrained with 500:1 still available depending on the broker and your trading style. Japan’s ‘Financial Services Agency’ (FSA) reduced the maximum leverage in 2011 from 50:1 to 25:1 having lowered it the year before from 100:1 to 50:1. In a similar vein, increasing numbers of Japanese traders have since looked abroad for a ‘suitable’ broker.

Quite ironic because regulators see margin FX trading as ‘unsuitable’ for many retail investors. It seems that when it comes to leverage and risk-taking, the majority of investors/traders do not want to be restricted or ‘protected’ by regulatory guidelines and rules.

All in the Same Boat

There have been several cases of market abuse that have affected both retail and institutional investors. In the U.S, "nearly 26,000 individuals lost $460 million in currency-related swindles between 2001 and 2007," according to a Forbes article published last month.

Investigations published in 2013 by the UK’s Financial Conduct Authority (FCA) on the abuse of WM/Reuters (FX) rates, combined with the Swiss Financial Market Supervisory Authority (FINMA) investigating several Swiss firms has cast a shadow over the FX market and added weight to calls for a complete overhaul. The German regulator, BaFin, officially confirmed cases of FX manipulation in May this year.

In December 2013, UBS agreed to pay approximately 1.4 billion Swiss francs ($1.6 billion) as part of a settlement with American, British and Swiss authorities in connection with the LIBOR inquiry. Other banks including RBS, Barclays and Lloyds have also been fined for LIBOR rate manipulation.

FINMA said it was investigating several Swiss banks but was reluctant to name them. The agency also said it was cooperating with authorities in other countries and that banks outside the country were also suspected. In a statement FINMA said it is “currently conducting investigations into several Swiss financial institutions in connection with possible manipulation of foreign exchange markets. FINMA is coordinating closely with authorities in other countries as multiple banks around the world are potentially implicated.”

In June 2014, the FCA said it was examining claims that traders at large banks manipulated some foreign exchange benchmark rates and that it might start an official investigation. It was not immediately clear if that preliminary inquiry was related to the Swiss investigation.

Questions for a Regulator

A uniformed approach to FX market standards amongst the world’s most prominent regulatory authorities does not exist and moreover, is not being sought.

Is it cynical to ask whether the 5%-10% market share occupied by the retail FX industry has any bearing on regulators’ priorities? With so many other financial market practices under scrutiny, do regulators have the resources to regulate the FX market as well? If they’re struggling to keep up with the current workload without FX, how does adding FX to their coverage help anyone aside from stretching existing resources further?

For the time being, the two biggest selling points of a global regulatory regime in the FX market is that this would curb FX manipulation amongst the largest market players and protect smaller investors using retail brokers to speculate on the FX market.

But would additional regulation be able to achieve that?

In Part 2 to be published next week. we will discuss the implications of implementing a unilateral, one-size-fits-all regulatory policy across the globe.

The Foreign Exchange (FX) market is currently under the microscope. Regulatory agencies from Switzerland, Germany, Europe, US, UK and Australia are investigating how the FX market works in practice and whether it’s prudent to regulate it globally.

The FX market differs from all other asset classes in that in its current form, it is completely unregulated, operates over-the-counter, which means there is no central marketplace ,and is by far the largest by capitalization. So as regulators ponder ways to regulate this market, they first have to quantify and ring-fence its reach.

This is incredibly difficult to do because large currency transactions can take place as part of everyday life (property investment for example) and given fluctuating currency rates, people effectively speculate on currency movements without even being aware of it. With other asset classes this doesn’t apply.

Spot FX transactions are not regulated in any country, despite the assumption that the FCA, NFA, ASIC and others regulate financial services and by extension, the FX market which is part of the financial services landscape. In fact, what is actually regulated are FX derivatives such as CFDs, Futures and Options. In the case of the Financial Conduct Authority (FCA), spot FX contracts are not qualifying investments under The Financial Services and Markets Act (FSMA) and therefore, FX dealing cannot apply to the market abuse regime under and the FCA’s Code of Market Conduct guidelines. This is likely to factor into how banks defend their actions in response to FX manipulation allegations.

International Financial Markets Regulation by Industry Segment | Source: ASIC

Muzzled but Motivated

Despite the jurisdictional quagmire, some attempts have been made to reduce market abuse and mistreatment of private retail investors. The Commodities and Futures Commission (CFTC) created a special task force in 2008 to reign in unscrupulous brokers and introduced harsh penalties in 2010 to protect retail FX traders.

The knock-on effect has been for U.S traders to seek trading accounts elsewhere around the globe with lower margin requirements. Regulators seem to be creating bit-part solutions which human nature and technology find a way of avoiding before the ink is even dry on the regulatory amendment.

In the UK and Europe, regulation is limited and leverage is unrestrained with 500:1 still available depending on the broker and your trading style. Japan’s ‘Financial Services Agency’ (FSA) reduced the maximum leverage in 2011 from 50:1 to 25:1 having lowered it the year before from 100:1 to 50:1. In a similar vein, increasing numbers of Japanese traders have since looked abroad for a ‘suitable’ broker.

Quite ironic because regulators see margin FX trading as ‘unsuitable’ for many retail investors. It seems that when it comes to leverage and risk-taking, the majority of investors/traders do not want to be restricted or ‘protected’ by regulatory guidelines and rules.

All in the Same Boat

There have been several cases of market abuse that have affected both retail and institutional investors. In the U.S, "nearly 26,000 individuals lost $460 million in currency-related swindles between 2001 and 2007," according to a Forbes article published last month.

Investigations published in 2013 by the UK’s Financial Conduct Authority (FCA) on the abuse of WM/Reuters (FX) rates, combined with the Swiss Financial Market Supervisory Authority (FINMA) investigating several Swiss firms has cast a shadow over the FX market and added weight to calls for a complete overhaul. The German regulator, BaFin, officially confirmed cases of FX manipulation in May this year.

In December 2013, UBS agreed to pay approximately 1.4 billion Swiss francs ($1.6 billion) as part of a settlement with American, British and Swiss authorities in connection with the LIBOR inquiry. Other banks including RBS, Barclays and Lloyds have also been fined for LIBOR rate manipulation.

FINMA said it was investigating several Swiss banks but was reluctant to name them. The agency also said it was cooperating with authorities in other countries and that banks outside the country were also suspected. In a statement FINMA said it is “currently conducting investigations into several Swiss financial institutions in connection with possible manipulation of foreign exchange markets. FINMA is coordinating closely with authorities in other countries as multiple banks around the world are potentially implicated.”

In June 2014, the FCA said it was examining claims that traders at large banks manipulated some foreign exchange benchmark rates and that it might start an official investigation. It was not immediately clear if that preliminary inquiry was related to the Swiss investigation.

Questions for a Regulator

A uniformed approach to FX market standards amongst the world’s most prominent regulatory authorities does not exist and moreover, is not being sought.

Is it cynical to ask whether the 5%-10% market share occupied by the retail FX industry has any bearing on regulators’ priorities? With so many other financial market practices under scrutiny, do regulators have the resources to regulate the FX market as well? If they’re struggling to keep up with the current workload without FX, how does adding FX to their coverage help anyone aside from stretching existing resources further?

For the time being, the two biggest selling points of a global regulatory regime in the FX market is that this would curb FX manipulation amongst the largest market players and protect smaller investors using retail brokers to speculate on the FX market.

But would additional regulation be able to achieve that?

In Part 2 to be published next week. we will discuss the implications of implementing a unilateral, one-size-fits-all regulatory policy across the globe.

The Unnamed Firm Behind Lithuania's 2.5 Million-Client Surge

Featured Videos

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.