In part two of our Italy-focused series, we explore why only 29% of Italian adults invest—one of the lowest rates in Western Europe.

CFDs? Only 9% said they would invest significantly in high-risk security.

Despite being a nation of savers, Italians remain largely absent from the financial markets. The average Italian investor would prefer a low-risk, low-return investment with a short- to medium-term holding period. This is mainly due to liquidity needs related to unexpected expenses, lifestyle choices, and family support rather than long-term retirement planning.

Italian Investors' Habits

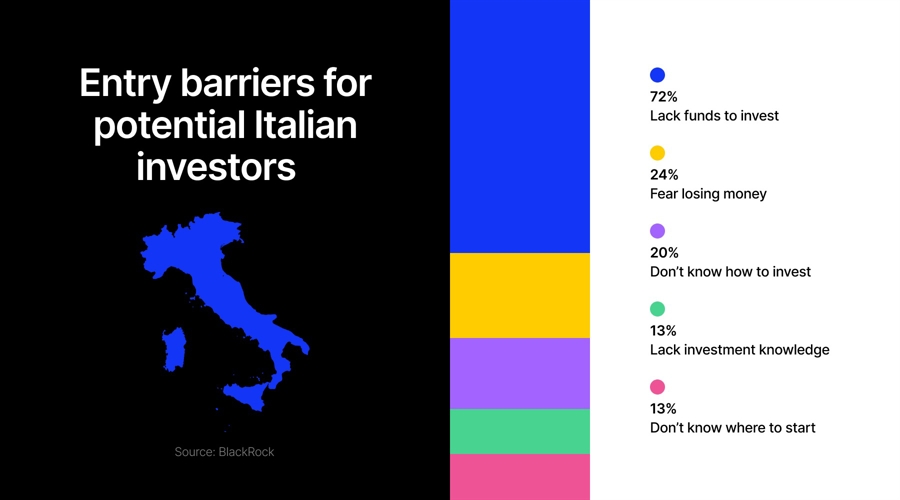

These behavioral patterns and investment preferences were clearly illustrated in BlackRock’s October 2024 “People and Money” report, which analyzed investment trends across 14 European markets. Focusing on the Italian market, BlackRock surveyed nearly 5,000 investors and identified nine key barriers preventing potential Italian investors from entering the market.

The survey revealed that 72% of respondents do not have enough money to invest, while 24% are worried about losing money. Additionally, 20% do not know how to invest, and 13% lack sufficient knowledge about what to invest in. Another 13% do not know where to start, while 7% are unaware of the benefits of investing. Furthermore, 6% find it difficult to control their expenses, 5% do not have enough time to invest, and 3% struggle to select the best investment from different alternatives.

The result? Only 29% of Italian adults invest—one of the lowest percentages in Western Europe, ahead of only Spain and Portugal, where the figure is 28%.

When it comes to investing, the gap between Europe and the United States is striking. While 58% of American households have some exposure to the stock market, only 7% of European families do. Nowhere is this contrast more evident than in Italy, where retail investors have long been known for their cautious approach, favoring stability over risk.

A 2022 survey by the Commissione Nazionale per le Società e la Borsa (CONSOB), Italy’s financial regulator, sheds light on the reasons behind this conservative mindset. It reveals that a combination of low financial literacy, limited budgeting habits, and cultural influences continues to shape the investment choices of the average Italian household.

From this survey, it emerged that the main reasons behind the average Italian household’s portfolio composition—and the stereotype, rooted in tradition, of preferring stable assets—mainly derive from two factors: low perceived financial knowledge and poor financial planning and budgeting skills.

Risk-Averse Italians

Among the surveyed population of Italian retail investors, in most cases, fewer than 50% stated that they had heard of and understood basic financial concepts such as the risk-return relationship, compound interest, inflation, mortgages, and diversification. Consequently, many Italian retail investors might feel completely unprepared when considering an investment in a more complex financial product such as a CFD.

Source: CONSOB survey

To compare perceived and actual financial knowledge, CONSOB’s survey also included a brief questionnaire that investors had to answer to assess their understanding of basic financial concepts. In every category, at least one-fifth of the investors underestimated their knowledge. Netting out the downward and upward mismatch, the results suggest that, on average, Italian investors underestimate their financial understanding. This phenomenon is particularly evident in topics such as the risk-return relationship and compound interest, where only one-third of Italians stated that they had “heard of and understood” the concepts.

Because of this, along with other tradition-based factors, Italian investors can generally be considered risk-averse. Around 70% of investors in Italy prefer to invest in moderate-and low-return assets to limit their exposure. Moreover, almost 70% of investors agreed with the statement, “I feel anxious if there is even the possibility of losing any portion of the invested capital,” further reinforcing the risk aversion of the average household.

Turning to CFDs, the risk aversion survey revealed that only 9% of surveyed investors agreed that they would invest significantly in a high-risk security, indicating the likely portfolio weight of CFDs and other derivatives in the average Italian portfolio.

Despite Italians being considered a nation of savers, recent polls show that one of the main barriers to entering the financial markets is the lack of disposable income. In the CONSOB report, investors were asked about their financial planning and budgeting habits. The findings revealed that 43% of Italians had never had a financial plan in their lives, and only 18% had a budget that they always adhered to. As a result, only 12.4% of Italians were considered savvy planners.

Italian Investors Are Left Behind

A key factor limiting Italians’ ability to invest is the primary reason they save in the first place. Italy ranks second only to Spain and Portugal for having the lowest percentage of adults investing in Western Europe. Beyond the reasons already discussed, a major factor is that only 31% of savers have retirement as their goal. Instead, most households save to enjoy life, support their families, prepare for unexpected events, and for other personal reasons.

Source: CONSOB survey

Given the risk aversion of Italian investors and the barriers to entry faced by potential ones, it is unsurprising that the composition of the average Italian portfolio leans towards safe assets. According to CONSOB’s report, in 2022, the average investor allocated 50% of their portfolio to bank and postal savings, 29% to mutual funds, and 18% to Italian government bonds. Meanwhile, only 2% of the average portfolio was allocated to derivatives, and 3% fell into the “other” category, which includes CFDs, Alternative Investment Funds (AIFs), and other financial instruments.

However, it is important to view this data with caution, as 2021 and 2022 were unique years following the pandemic crisis. The uncertain market conditions and high-yielding bonds may have further pushed Italian investors towards safer investment options during this period.

The next part of this Italy-centric series will dive deep into how the investment trends in the country are changing among young investors.

Despite being a nation of savers, Italians remain largely absent from the financial markets. The average Italian investor would prefer a low-risk, low-return investment with a short- to medium-term holding period. This is mainly due to liquidity needs related to unexpected expenses, lifestyle choices, and family support rather than long-term retirement planning.

Italian Investors' Habits

These behavioral patterns and investment preferences were clearly illustrated in BlackRock’s October 2024 “People and Money” report, which analyzed investment trends across 14 European markets. Focusing on the Italian market, BlackRock surveyed nearly 5,000 investors and identified nine key barriers preventing potential Italian investors from entering the market.

The survey revealed that 72% of respondents do not have enough money to invest, while 24% are worried about losing money. Additionally, 20% do not know how to invest, and 13% lack sufficient knowledge about what to invest in. Another 13% do not know where to start, while 7% are unaware of the benefits of investing. Furthermore, 6% find it difficult to control their expenses, 5% do not have enough time to invest, and 3% struggle to select the best investment from different alternatives.

The result? Only 29% of Italian adults invest—one of the lowest percentages in Western Europe, ahead of only Spain and Portugal, where the figure is 28%.

When it comes to investing, the gap between Europe and the United States is striking. While 58% of American households have some exposure to the stock market, only 7% of European families do. Nowhere is this contrast more evident than in Italy, where retail investors have long been known for their cautious approach, favoring stability over risk.

A 2022 survey by the Commissione Nazionale per le Società e la Borsa (CONSOB), Italy’s financial regulator, sheds light on the reasons behind this conservative mindset. It reveals that a combination of low financial literacy, limited budgeting habits, and cultural influences continues to shape the investment choices of the average Italian household.

From this survey, it emerged that the main reasons behind the average Italian household’s portfolio composition—and the stereotype, rooted in tradition, of preferring stable assets—mainly derive from two factors: low perceived financial knowledge and poor financial planning and budgeting skills.

Risk-Averse Italians

Among the surveyed population of Italian retail investors, in most cases, fewer than 50% stated that they had heard of and understood basic financial concepts such as the risk-return relationship, compound interest, inflation, mortgages, and diversification. Consequently, many Italian retail investors might feel completely unprepared when considering an investment in a more complex financial product such as a CFD.

Source: CONSOB survey

To compare perceived and actual financial knowledge, CONSOB’s survey also included a brief questionnaire that investors had to answer to assess their understanding of basic financial concepts. In every category, at least one-fifth of the investors underestimated their knowledge. Netting out the downward and upward mismatch, the results suggest that, on average, Italian investors underestimate their financial understanding. This phenomenon is particularly evident in topics such as the risk-return relationship and compound interest, where only one-third of Italians stated that they had “heard of and understood” the concepts.

Because of this, along with other tradition-based factors, Italian investors can generally be considered risk-averse. Around 70% of investors in Italy prefer to invest in moderate-and low-return assets to limit their exposure. Moreover, almost 70% of investors agreed with the statement, “I feel anxious if there is even the possibility of losing any portion of the invested capital,” further reinforcing the risk aversion of the average household.

Turning to CFDs, the risk aversion survey revealed that only 9% of surveyed investors agreed that they would invest significantly in a high-risk security, indicating the likely portfolio weight of CFDs and other derivatives in the average Italian portfolio.

Despite Italians being considered a nation of savers, recent polls show that one of the main barriers to entering the financial markets is the lack of disposable income. In the CONSOB report, investors were asked about their financial planning and budgeting habits. The findings revealed that 43% of Italians had never had a financial plan in their lives, and only 18% had a budget that they always adhered to. As a result, only 12.4% of Italians were considered savvy planners.

Italian Investors Are Left Behind

A key factor limiting Italians’ ability to invest is the primary reason they save in the first place. Italy ranks second only to Spain and Portugal for having the lowest percentage of adults investing in Western Europe. Beyond the reasons already discussed, a major factor is that only 31% of savers have retirement as their goal. Instead, most households save to enjoy life, support their families, prepare for unexpected events, and for other personal reasons.

Source: CONSOB survey

Given the risk aversion of Italian investors and the barriers to entry faced by potential ones, it is unsurprising that the composition of the average Italian portfolio leans towards safe assets. According to CONSOB’s report, in 2022, the average investor allocated 50% of their portfolio to bank and postal savings, 29% to mutual funds, and 18% to Italian government bonds. Meanwhile, only 2% of the average portfolio was allocated to derivatives, and 3% fell into the “other” category, which includes CFDs, Alternative Investment Funds (AIFs), and other financial instruments.

However, it is important to view this data with caution, as 2021 and 2022 were unique years following the pandemic crisis. The uncertain market conditions and high-yielding bonds may have further pushed Italian investors towards safer investment options during this period.

The next part of this Italy-centric series will dive deep into how the investment trends in the country are changing among young investors.

Edoardo Catani is an Italian financial analyst and financial writer specializing in trading and investing. Since 2021, he has produced over 1,000 articles on technical and fundamental analysis for leading financial platforms, including DailyForex, Finance Magnates, and Investing.com. His expertise covers forex, stocks, cryptocurrencies, and market indices.

Passionate about global markets, he focuses on financial research, risk management, and derivative analysis. Edoardo actively manages a well-diversified portfolio of North American and European stocks and ETFs with a long-term approach. He also operates a swing trading account, optimizing value-based investment strategies through fundamental analysis and quantitative modeling.

Plus500 Sees 20% Margin on Its US Business, Double What Its CEO Calls Market Practice

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.