FCA wants to see more competition in the open banking services industry.

Seven million Britons currently use the UK’s open banking products.

Bloomberg

The Joint

Regulatory Oversight Committee (JROC), which is co-led by the Financial Conduct

Authority (FCA) and the Payment Systems Regulator (PSR), has released its

proposed guidelines for the upcoming stage of open banking in the United

Kingdom.

JROC Unveils Two-Year Open

Banking Development Plan

JROC was

established with the cooperation of the FCA and the PSR in March 2022, and its

main purpose is to oversee planning and preparation for the creation of a

future open banking entity and the transition to the future framework.

The term 'open

banking' pertains to the utilization of banking data from clients at

established financial institutions by third-party companies to provide

customized services like lending and payments. This industry has contributed to

the transformation of the UK's fintech sector into the third largest in the

world.

More than a

year after its establishment, JROC has published recommendations presenting the

next phase of open banking development in the islands. Among the recommended

steps were proposals to develop a scalable, secure and economically sustainable

system.

"Open

banking can be a UK success story and we want to help it grow and develop

sustainably. Today's report sets out a roadmap and the framework for delivering

the next phase of open banking," the Co-Chairs of the Committee, PSR's

Managing Director, Chris Hemsley, and the FCA's Executive Director of Consumers and

Competition, Sheldon Mills, said in the statement.

"Only

through effective collaboration can we deliver on our ambition and develop open

banking in a way that promotes continued innovation and competition, for the

benefit of consumers, businesses, and the wider economy," the statement

added.

The report details how open banking can develop further in a safe, scalable and economically sustainable way. https://t.co/amOfOq155n

The JROC

has outlined its vision for the future of open banking and identified the

necessary steps required in its design. This includes a transition from the

current Open Banking Implementation Entity (OBIE) to the new entity that will

build on the substantial progress achieved so far.

"Britain

leads the pack in open banking, with 7 million users, but we can't sit back and

put our feet up," Andrew Griffith, the City Minister, said. "Today's plan

will deliver a new generation of products and services, making banking more

accessible and convenient for millions of people."

The JROC

will collaborate with industry stakeholders and oversee progress towards the

five key themes and the design of the future entity. They will provide a

progress report in Q4 2023 and a detailed plan for the transition from OBIE to

the future entity. The roadmap's full timetable is outlined

in the publication.

What Is the Future of Open

Banking?

After

Brexit, the UK is eager to advance open banking to draw in more fintech

companies, especially since the European Union is preparing to launch its own

comprehensive open banking scheme. While regulators have praised the successful

implementation of open banking technology in the UK fintech industry, industry

leaders cautioned against becoming too complacent.

According

to Chris Hayward, the Policy Chief at the City of London Corporation, which manages

London's financial district, the UK's fintech industry ranks third worldwide,

with a total investment of $12.5 billion in 2022, following the United States

and China.

Fintechs

and challenger banks are

projected to grow in the coming years. According to Business Insider

Intelligence, digital banks will have over 75 million subscribers in the United

States alone by 2023. This indicates a 25% growth over the current user base.

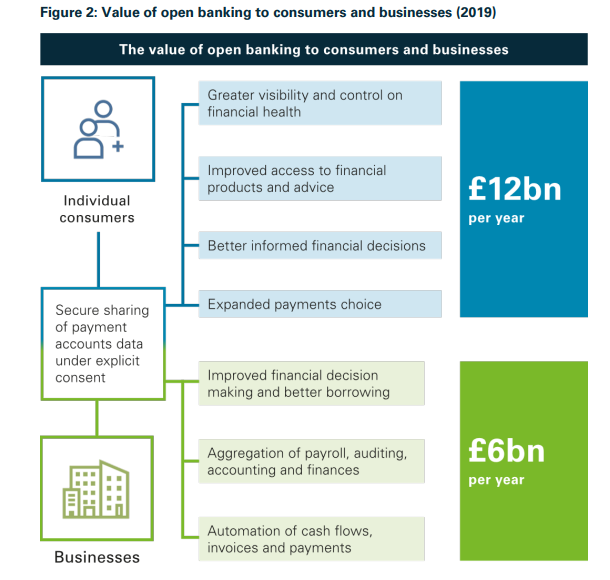

Value of open banking to consumers and businesses (2019). Source: Gov.uk

API

integration is a significant focus in the industry, involving linking

various software systems via APIs. APIs enable secure and efficient sharing of

data between software systems. Within banking, API integration facilitates the

exchange of consumer data among different financial institutions and enables

the creation of innovative new services.

The Global

Opportunity Analysis and Industry Forecast report states that the size of the

global online banking market was worth $11.43 billion in 2019 and is

expected to grow to $31.81 billion by 2027.

FCA Wants Greater Investor

Protection

In the

meantime, the FCA has released its business plan for 2023-2024, outlining its

roadmap for the next 12 months in accordance with the three-year development

strategy introduced a year ago. Its primary objective is to enhance overall

investor protection.

Meanwhile,

the UK is taking steps to prepare for cryptocurrency regulation by launching a

public consultation to create a draft law on regulating digital assets.

To further

bolster the safety of retail traders, the UK financial market supervisor has

appointed joint Executive Directors of Enforcement and Market Oversight, Steve

Smart and Therese Chambers, following Mark Steward's retirement in October last

year.

Additionally,

the FCA and the Advertising Standards Authority (ASA) have collaborated on a

campaign to educate financial influencers and prevent the promotion of illegal

'get rich quick' schemes. The agencies have partnered with prominent social

media influencer Sharon Gaffka.

Furthermore, the FCA is actively expanding its regulatory efforts, as evidenced by its rejection

of 8,582 financial promotions in 2022, seeking their amendment or removal by

authorized firms, which is an increase of 1,400% from the 573 financial promotions it

rejected in 2021.

The Joint

Regulatory Oversight Committee (JROC), which is co-led by the Financial Conduct

Authority (FCA) and the Payment Systems Regulator (PSR), has released its

proposed guidelines for the upcoming stage of open banking in the United

Kingdom.

JROC Unveils Two-Year Open

Banking Development Plan

JROC was

established with the cooperation of the FCA and the PSR in March 2022, and its

main purpose is to oversee planning and preparation for the creation of a

future open banking entity and the transition to the future framework.

The term 'open

banking' pertains to the utilization of banking data from clients at

established financial institutions by third-party companies to provide

customized services like lending and payments. This industry has contributed to

the transformation of the UK's fintech sector into the third largest in the

world.

More than a

year after its establishment, JROC has published recommendations presenting the

next phase of open banking development in the islands. Among the recommended

steps were proposals to develop a scalable, secure and economically sustainable

system.

"Open

banking can be a UK success story and we want to help it grow and develop

sustainably. Today's report sets out a roadmap and the framework for delivering

the next phase of open banking," the Co-Chairs of the Committee, PSR's

Managing Director, Chris Hemsley, and the FCA's Executive Director of Consumers and

Competition, Sheldon Mills, said in the statement.

"Only

through effective collaboration can we deliver on our ambition and develop open

banking in a way that promotes continued innovation and competition, for the

benefit of consumers, businesses, and the wider economy," the statement

added.

The report details how open banking can develop further in a safe, scalable and economically sustainable way. https://t.co/amOfOq155n

The JROC

has outlined its vision for the future of open banking and identified the

necessary steps required in its design. This includes a transition from the

current Open Banking Implementation Entity (OBIE) to the new entity that will

build on the substantial progress achieved so far.

"Britain

leads the pack in open banking, with 7 million users, but we can't sit back and

put our feet up," Andrew Griffith, the City Minister, said. "Today's plan

will deliver a new generation of products and services, making banking more

accessible and convenient for millions of people."

The JROC

will collaborate with industry stakeholders and oversee progress towards the

five key themes and the design of the future entity. They will provide a

progress report in Q4 2023 and a detailed plan for the transition from OBIE to

the future entity. The roadmap's full timetable is outlined

in the publication.

What Is the Future of Open

Banking?

After

Brexit, the UK is eager to advance open banking to draw in more fintech

companies, especially since the European Union is preparing to launch its own

comprehensive open banking scheme. While regulators have praised the successful

implementation of open banking technology in the UK fintech industry, industry

leaders cautioned against becoming too complacent.

According

to Chris Hayward, the Policy Chief at the City of London Corporation, which manages

London's financial district, the UK's fintech industry ranks third worldwide,

with a total investment of $12.5 billion in 2022, following the United States

and China.

Fintechs

and challenger banks are

projected to grow in the coming years. According to Business Insider

Intelligence, digital banks will have over 75 million subscribers in the United

States alone by 2023. This indicates a 25% growth over the current user base.

Value of open banking to consumers and businesses (2019). Source: Gov.uk

API

integration is a significant focus in the industry, involving linking

various software systems via APIs. APIs enable secure and efficient sharing of

data between software systems. Within banking, API integration facilitates the

exchange of consumer data among different financial institutions and enables

the creation of innovative new services.

The Global

Opportunity Analysis and Industry Forecast report states that the size of the

global online banking market was worth $11.43 billion in 2019 and is

expected to grow to $31.81 billion by 2027.

FCA Wants Greater Investor

Protection

In the

meantime, the FCA has released its business plan for 2023-2024, outlining its

roadmap for the next 12 months in accordance with the three-year development

strategy introduced a year ago. Its primary objective is to enhance overall

investor protection.

Meanwhile,

the UK is taking steps to prepare for cryptocurrency regulation by launching a

public consultation to create a draft law on regulating digital assets.

To further

bolster the safety of retail traders, the UK financial market supervisor has

appointed joint Executive Directors of Enforcement and Market Oversight, Steve

Smart and Therese Chambers, following Mark Steward's retirement in October last

year.

Additionally,

the FCA and the Advertising Standards Authority (ASA) have collaborated on a

campaign to educate financial influencers and prevent the promotion of illegal

'get rich quick' schemes. The agencies have partnered with prominent social

media influencer Sharon Gaffka.

Furthermore, the FCA is actively expanding its regulatory efforts, as evidenced by its rejection

of 8,582 financial promotions in 2022, seeking their amendment or removal by

authorized firms, which is an increase of 1,400% from the 573 financial promotions it

rejected in 2021.

Damian Chmiel is a Senior Analyst & Editor at Finance Magnates with more than 15 years of experience in the CFD and online trading industry. Active as both a trader and journalist since 2010, he focuses on broker coverage, fintech innovation, and regulatory developments across Europe, the Middle East, and Asia.

His work includes interviews with C-level leaders at major brokerages and fintech platforms, as well as co-authoring Finance Magnates’ quarterly industry benchmarking reports. Damian’s reporting is data-driven, market-aware, and grounded in direct industry engagement. His analysis and commentary have also been cited by external media outlets, including Investing.com, Binance, The Asset, Stockhead, and Dispatch.

Education:

MA in Finance and Accounting, Cracow University of Economics

75% of Kalshi Users Never Trade, but Platform Still Intends to Capitalise on That

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.