And this mirage--regardless of whether or not any Bitcoin ETF application is ever approved--has served an important function: hope. Indeed, the fact that so many Bitcoin ETF applications have been delayed rather than denied outright has given way to much positive speculation (although, perhaps, not all of it has been healthy.)

In several weeks, the SEC will be forced to make a decision on two Bitcoin ETF applications: Bitwise Asset Management will receive a decision on October 13, while VanEck/SolidX will receive its decision on the 18th.Analysts inside and outside of the industry have predicted that the approval of either one of these Bitcoin ETF applications would be the regulatory and financial boon to Bitcoin that the cryptocurrency has been seeking for such a long time.

But is there any truth to that assumption?

Underwhelming response to Van Eck & SolidX' "BTF"

If the recent launch of VanEck and SolidX’ most recent investment product--which has been described as a “limited” Bitcoin ETF--is any indication of what will happen when a full Bitcoin ETF is launched, the answer is a resounding “no.”

Let’s back up for a moment: earlier this month, VanEck Securities and SolidX management--two firms that have jointly applied for the opportunity to create a Bitcoin ETF in the past--bypassed regulatory hurdles to launching the new product.

Because of SEC exemption 144a, which can be used to allow securities to be resold to qualified buyers, shares of the VanEck SolidX Bitcoin Trust can now be traded by hedge funds and banks, but they are still unavailable to retail investors. Still, the product is similar to an ETF: Ed Lopez, head of ETF Product at VanEck, told CoinDesk that the offering “allows for shares to be created and redeemed like ETFs, but it is not an ETF.”

A press release announcing the new product explained that “the shares will provide institutional investors access to a physically-backed bitcoin product that is tradeable through traditional and prime brokerage accounts.”

“The Shares are the first institutional-quality, cleared product providing exposure to bitcoin and enabling a standard ETF creation-and-redemption process.”

Lopez clarified that “unlike an ETF it isn’t listed on a national exchange, rather it is quoted on the OTC Link ATS platform. This is a first-of-its-kind type of offering. Given it will trade over-the-counter via broker-to-broker transactions, we’ve been casually referring to it as a Broker Traded Fund, a BTF.”

"This trust is just a bad launch of a product for which there's not much demand.”

More than a week after the product’s launch, however, the market’s response to the product has been seriously underwhelming.

Alex Krüger, a well-known economist and trader within the cryptocurrency space, tweeted that “this trust is just a bad launch of a product for which there's not much demand.”

Three days after launch, the VanEck bitcoin trust for institutional investors has reportedly managed to issue a whopping 1 (one) basket. It has 4 bitcoins or $41,400 in assets under management. Massive. pic.twitter.com/TUePbLVqBi

Krüger also pointed specifically to the fact that the product isn’t available to retail investors: “It is for QIBs [qualified institutional buyers] alone,” he wrote.

In a piece for Investing.com, financial journalist Tanzeel Akhtar explained that QIBs are “[purchasers who are] considered financially sophisticated and manages a minumum of $100 million or more in securities. These investors are recognized by securities market regulators as needing less protection from issuers than retail investors.”

Krüger’s point seems to have an interesting implication: that the imagined pool of qualified institutional buyers that are waiting for a Bitcoin ETF in order to get into cryptocurrency markets simply doesn’t exist--and perhaps that the QIBs who are interested in investing in Bitcoin have already done so.

Investors who want Bitcoin “have already found a way to do it”

This was exactly the point that Bitcoin developer Jimmy Song made in an interview conducted with BlockTV earlier this week.

“If you want Bitcoin, you’re going to have found a way to do it,” he said. “The thing is, that if you’re going to own Bitcoin, you’re going to need to know about it--and the people that hold it know about it, really understand it. The people who come in and think ‘oh, that’s a cute looking ticker, I’ll go and buy some,”--they’re gonna sell within six months when it doubles or halves.”

"If you don't get it, then you are going to get it eventually because bitcoin is the hardest money in existence." - @jimmysong.

Song also said that the world doesn’t need a Bitcoin ETF and that it won’t be the “game-changer” that so many have hoped that it will be. Song said that instead, the ETF was “more of a convenience play,” and that while it may make investing in Bitcoin a bit easier for institutional investors, investors who truly want Bitcoin in their portfolios have probably already found a way to do so.

“Those are not the people that really give it value,” he added. “The people that store it and really believe in it--the holders of last resort--they’re the ones that really give it value.”

Just “another GBTC”

So exactly what purpose does this new "limited ETF" serve? And what can we learn from it?

Clement Thibault, senior financial analyst for Investing.com, tweeted about his skepticism of the product. “Don't get too excited about the Van-Eck SolidX ‘Bitcoin ETF’ that was just approved,” he tweeted on September 3rd. “It's another GBTC, not the retail Bitcoin ETF everyone's been hoping for for the past 2 years.”

Don't get too excited about the Van-Eck SolidX "Bitcoin ETF" that was just approved. It's another GBTC, not the retail Bitcoin ETF everyone's been hoping for for the past 2 years.

There's still no Bitcoin retail ETF, I don't expect one anytime soon either

— Clement Thibault (@ClemThibault) September 3, 2019

“GBTC” refers to the Greyscale Bitcoin Investment Trust, a product that--unlike Van Eck’s “limited ETF”--allows both QIBs and non-accredited investors to trade in Bitcoin markets by purchasing shares of GBTC through a broker. However, GBTC charges investors a 2 percent annual fee, which is considerably higher than fees charged for similar products--for example, the GLD Gold ETF charges an annual fee of just 0.4 percent.

GBTC also charges a premium on its underlying asset--in May of 2017, that premium rose as high as 132.6% in May of 2017. This means two things: that you can get a lot less bang for your buck in terms of BTC ownership, and that the price of the Bitcoin Trust does not necessarily mimic the price of BTC.

A report on GBTC by SaneCrypto in May 2018 explained that “in fact, on roughly one out of three trading days, bitcoin and GBTC actually moved in opposite directions. In fact, looking at the three month period just ended, the price of GBTC’ Bitcoin holdings went up 6.55% on the open market but the market price of GBTC itself, went down 1.67%.”

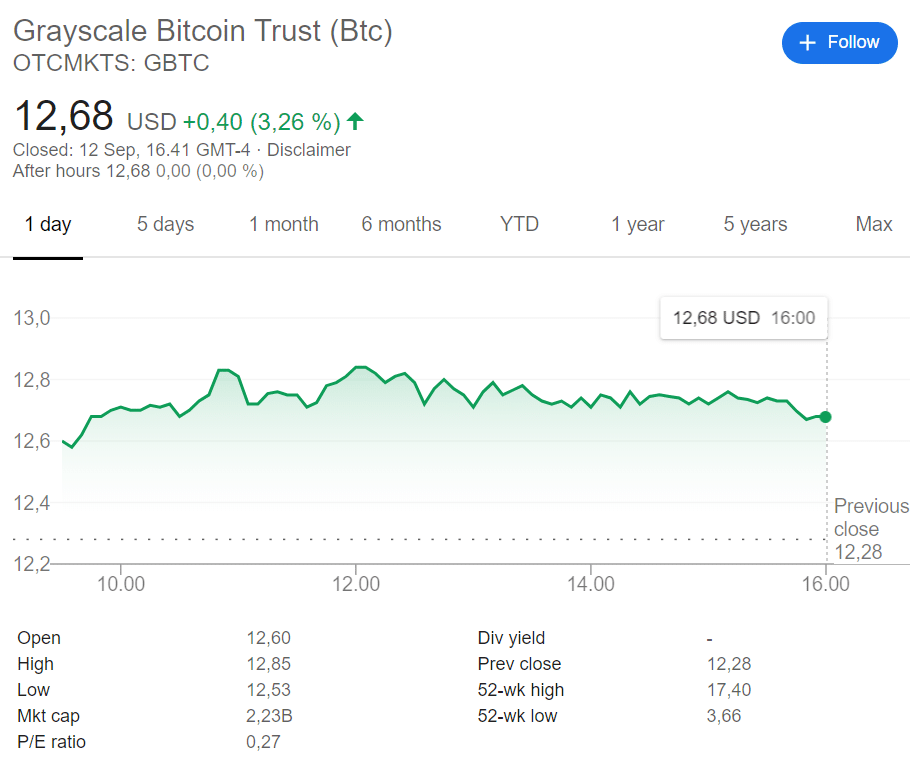

At press time, for example, the price of BTC had risen 2.37 percent in the last 24 hours, while the price of GBTC was up 3.26 percent. BTC’s market cap was $186.3 billion, while GTBC’s sat at $2.23 billion.

Source: Google; 13.9.2019

Therefore, the "limited ETF" could indeed be "another GBTC"--but so far, investor interest has been even more underwhelming.

”Too early to judge the success of the product,”

However, Tom Lee, Managing Partner and the Head of Research at Fundstrat, seems to have a slightly more optimistic take on the launch of the limited ETF and the subsequent lack of interest.

“I think it is too early to judge the success of the product,” he tweeted in response to Krüger’s initial comments on the low flow of capital into the limited ETF.

I think it is too early to judge the success of the product.

Charles Lu, CEO of Findora, pointed out that the new product could also act as a sort of litmus test for regulators that could eventually pave the way to a “real” Bitcoin ETF: “The Van Eck SolidX offering is a good sign of experimentation under the current regulatory framework in the U.S.," he said to Investing.com.

However, Mitesh Shah, Founder & CEO of Omnia Markets, disagrees.

Mitesh Shah, Founder & CEO of Omnia Markets.

Shah argued that in fact, the launch (and subsequent flop) of the product so close to the final judgment day of the Van Eck/SolidX Bitcoin ETF application is likely fuel for the fire against an approval.

“Due to the trust’s lack of support and three upcoming ETFs that the SEC will be making decisions on their approval in the coming weeks, I do not believe that the trust offers a valid enough use case for the SEC to base its decisions on,” he told Finance Magnates.

Kyle Asman, partner at BX3 Capital, said to Finance Magnates that even if “the VanEck ETF will give people an insight into how [a Bitcoin ETF] might operate,” this ultimately won’t have a major effect on whether or not a Bitcoin ETF will hit the markets anytime soon.

Kyle Asman, partner at BX3 Capital.

“That isn’t the issue with getting approval,” he wrote. “The problem is the cryptocurrency markets are still young and thus easily can be manipulated. That is the fear among regulators in approving an ETF before the marketplace is ready.”

Clayton’s latest remarks

And indeed, SEC Chairman Jay Clayton said in an interview with CNBC conducted earlier this week that the Commission’s concerns regarding market manipulation and a lack of custody options in the cryptocurrency space still have not been abated.

“Given that they trade on largely unregulated exchanges is how can we be sure that those prices aren’t subject to significant manipulation?”, he said. “Now progress is being made, but people needed to answer those hard questions for us to be comfortable that this was the appropriate type of product.”

So is an approval on the horizon? Perhaps--but it seems unlikely that Van Eck/SolidX and Bitwise will receive the news they’ve been waiting for in October. Clayton said that the time may not be right: there is “work left to be done” before an approval is realistic.

And if the underwhelming response is any indication to how markets will react when (and if) a Bitcoin ETF is approved, well--VanEck/SolidX, Bitwise, and the other companies vying to be the first to create the product may want to reconsider the time and energy that they are continuing to spend on getting the SEC’s approval.

And this mirage--regardless of whether or not any Bitcoin ETF application is ever approved--has served an important function: hope. Indeed, the fact that so many Bitcoin ETF applications have been delayed rather than denied outright has given way to much positive speculation (although, perhaps, not all of it has been healthy.)

In several weeks, the SEC will be forced to make a decision on two Bitcoin ETF applications: Bitwise Asset Management will receive a decision on October 13, while VanEck/SolidX will receive its decision on the 18th.Analysts inside and outside of the industry have predicted that the approval of either one of these Bitcoin ETF applications would be the regulatory and financial boon to Bitcoin that the cryptocurrency has been seeking for such a long time.

But is there any truth to that assumption?

Underwhelming response to Van Eck & SolidX' "BTF"

If the recent launch of VanEck and SolidX’ most recent investment product--which has been described as a “limited” Bitcoin ETF--is any indication of what will happen when a full Bitcoin ETF is launched, the answer is a resounding “no.”

Let’s back up for a moment: earlier this month, VanEck Securities and SolidX management--two firms that have jointly applied for the opportunity to create a Bitcoin ETF in the past--bypassed regulatory hurdles to launching the new product.

Because of SEC exemption 144a, which can be used to allow securities to be resold to qualified buyers, shares of the VanEck SolidX Bitcoin Trust can now be traded by hedge funds and banks, but they are still unavailable to retail investors. Still, the product is similar to an ETF: Ed Lopez, head of ETF Product at VanEck, told CoinDesk that the offering “allows for shares to be created and redeemed like ETFs, but it is not an ETF.”

A press release announcing the new product explained that “the shares will provide institutional investors access to a physically-backed bitcoin product that is tradeable through traditional and prime brokerage accounts.”

“The Shares are the first institutional-quality, cleared product providing exposure to bitcoin and enabling a standard ETF creation-and-redemption process.”

Lopez clarified that “unlike an ETF it isn’t listed on a national exchange, rather it is quoted on the OTC Link ATS platform. This is a first-of-its-kind type of offering. Given it will trade over-the-counter via broker-to-broker transactions, we’ve been casually referring to it as a Broker Traded Fund, a BTF.”

"This trust is just a bad launch of a product for which there's not much demand.”

More than a week after the product’s launch, however, the market’s response to the product has been seriously underwhelming.

Alex Krüger, a well-known economist and trader within the cryptocurrency space, tweeted that “this trust is just a bad launch of a product for which there's not much demand.”

Three days after launch, the VanEck bitcoin trust for institutional investors has reportedly managed to issue a whopping 1 (one) basket. It has 4 bitcoins or $41,400 in assets under management. Massive. pic.twitter.com/TUePbLVqBi

Krüger also pointed specifically to the fact that the product isn’t available to retail investors: “It is for QIBs [qualified institutional buyers] alone,” he wrote.

In a piece for Investing.com, financial journalist Tanzeel Akhtar explained that QIBs are “[purchasers who are] considered financially sophisticated and manages a minumum of $100 million or more in securities. These investors are recognized by securities market regulators as needing less protection from issuers than retail investors.”

Krüger’s point seems to have an interesting implication: that the imagined pool of qualified institutional buyers that are waiting for a Bitcoin ETF in order to get into cryptocurrency markets simply doesn’t exist--and perhaps that the QIBs who are interested in investing in Bitcoin have already done so.

Investors who want Bitcoin “have already found a way to do it”

This was exactly the point that Bitcoin developer Jimmy Song made in an interview conducted with BlockTV earlier this week.

“If you want Bitcoin, you’re going to have found a way to do it,” he said. “The thing is, that if you’re going to own Bitcoin, you’re going to need to know about it--and the people that hold it know about it, really understand it. The people who come in and think ‘oh, that’s a cute looking ticker, I’ll go and buy some,”--they’re gonna sell within six months when it doubles or halves.”

"If you don't get it, then you are going to get it eventually because bitcoin is the hardest money in existence." - @jimmysong.

Song also said that the world doesn’t need a Bitcoin ETF and that it won’t be the “game-changer” that so many have hoped that it will be. Song said that instead, the ETF was “more of a convenience play,” and that while it may make investing in Bitcoin a bit easier for institutional investors, investors who truly want Bitcoin in their portfolios have probably already found a way to do so.

“Those are not the people that really give it value,” he added. “The people that store it and really believe in it--the holders of last resort--they’re the ones that really give it value.”

Just “another GBTC”

So exactly what purpose does this new "limited ETF" serve? And what can we learn from it?

Clement Thibault, senior financial analyst for Investing.com, tweeted about his skepticism of the product. “Don't get too excited about the Van-Eck SolidX ‘Bitcoin ETF’ that was just approved,” he tweeted on September 3rd. “It's another GBTC, not the retail Bitcoin ETF everyone's been hoping for for the past 2 years.”

Don't get too excited about the Van-Eck SolidX "Bitcoin ETF" that was just approved. It's another GBTC, not the retail Bitcoin ETF everyone's been hoping for for the past 2 years.

There's still no Bitcoin retail ETF, I don't expect one anytime soon either

— Clement Thibault (@ClemThibault) September 3, 2019

“GBTC” refers to the Greyscale Bitcoin Investment Trust, a product that--unlike Van Eck’s “limited ETF”--allows both QIBs and non-accredited investors to trade in Bitcoin markets by purchasing shares of GBTC through a broker. However, GBTC charges investors a 2 percent annual fee, which is considerably higher than fees charged for similar products--for example, the GLD Gold ETF charges an annual fee of just 0.4 percent.

GBTC also charges a premium on its underlying asset--in May of 2017, that premium rose as high as 132.6% in May of 2017. This means two things: that you can get a lot less bang for your buck in terms of BTC ownership, and that the price of the Bitcoin Trust does not necessarily mimic the price of BTC.

A report on GBTC by SaneCrypto in May 2018 explained that “in fact, on roughly one out of three trading days, bitcoin and GBTC actually moved in opposite directions. In fact, looking at the three month period just ended, the price of GBTC’ Bitcoin holdings went up 6.55% on the open market but the market price of GBTC itself, went down 1.67%.”

At press time, for example, the price of BTC had risen 2.37 percent in the last 24 hours, while the price of GBTC was up 3.26 percent. BTC’s market cap was $186.3 billion, while GTBC’s sat at $2.23 billion.

Source: Google; 13.9.2019

Therefore, the "limited ETF" could indeed be "another GBTC"--but so far, investor interest has been even more underwhelming.

”Too early to judge the success of the product,”

However, Tom Lee, Managing Partner and the Head of Research at Fundstrat, seems to have a slightly more optimistic take on the launch of the limited ETF and the subsequent lack of interest.

“I think it is too early to judge the success of the product,” he tweeted in response to Krüger’s initial comments on the low flow of capital into the limited ETF.

I think it is too early to judge the success of the product.

Charles Lu, CEO of Findora, pointed out that the new product could also act as a sort of litmus test for regulators that could eventually pave the way to a “real” Bitcoin ETF: “The Van Eck SolidX offering is a good sign of experimentation under the current regulatory framework in the U.S.," he said to Investing.com.

However, Mitesh Shah, Founder & CEO of Omnia Markets, disagrees.

Mitesh Shah, Founder & CEO of Omnia Markets.

Shah argued that in fact, the launch (and subsequent flop) of the product so close to the final judgment day of the Van Eck/SolidX Bitcoin ETF application is likely fuel for the fire against an approval.

“Due to the trust’s lack of support and three upcoming ETFs that the SEC will be making decisions on their approval in the coming weeks, I do not believe that the trust offers a valid enough use case for the SEC to base its decisions on,” he told Finance Magnates.

Kyle Asman, partner at BX3 Capital, said to Finance Magnates that even if “the VanEck ETF will give people an insight into how [a Bitcoin ETF] might operate,” this ultimately won’t have a major effect on whether or not a Bitcoin ETF will hit the markets anytime soon.

Kyle Asman, partner at BX3 Capital.

“That isn’t the issue with getting approval,” he wrote. “The problem is the cryptocurrency markets are still young and thus easily can be manipulated. That is the fear among regulators in approving an ETF before the marketplace is ready.”

Clayton’s latest remarks

And indeed, SEC Chairman Jay Clayton said in an interview with CNBC conducted earlier this week that the Commission’s concerns regarding market manipulation and a lack of custody options in the cryptocurrency space still have not been abated.

“Given that they trade on largely unregulated exchanges is how can we be sure that those prices aren’t subject to significant manipulation?”, he said. “Now progress is being made, but people needed to answer those hard questions for us to be comfortable that this was the appropriate type of product.”

So is an approval on the horizon? Perhaps--but it seems unlikely that Van Eck/SolidX and Bitwise will receive the news they’ve been waiting for in October. Clayton said that the time may not be right: there is “work left to be done” before an approval is realistic.

And if the underwhelming response is any indication to how markets will react when (and if) a Bitcoin ETF is approved, well--VanEck/SolidX, Bitwise, and the other companies vying to be the first to create the product may want to reconsider the time and energy that they are continuing to spend on getting the SEC’s approval.

Rachel is a self-taught crypto geek and a passionate writer. She believes in the power that the written word has to educate, connect and empower individuals to make positive and powerful financial choices. She is the Podcast Host and a Cryptocurrency Editor at Finance Magnates.

Bybit Splits Crypto and Payments Into Two Austrian Entities. Bybit.eu Will Run Both Under One Login

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.