Several national cryptocurrencies have made headlines over the last year, but not all of the publicity has been good.

In late 2017 and early 2018, national stablecoins were the talk of the industry. Rumors - some confirmed, some unconfirmed - that Estonia, Sweden, Iran, Russia, Venezuela, and others may be exploring the launch of a national stablecoin spread like wildfire.

Many believed that the launch of national cryptocurrencies was the thing - the thing that would finally prove cryptocurrencies as a valid transactional instrument, as a worthy investment, as more than just a fad.

However, the hype around many of these national cryptocurrency projects--just like the hype around many cryptocurrency projects--came and went. In most cases, national crypto initiatives faded out of the spotlight or disappeared altogether; in the worst cases, these national crypto projects were used as vehicles to avoid international sanctions and commit large-scale financial crimes.

How have these projects evolved over the last year? And how have they influenced the world’s view of cryptocurrency?

Whatever Happened with the Petro?

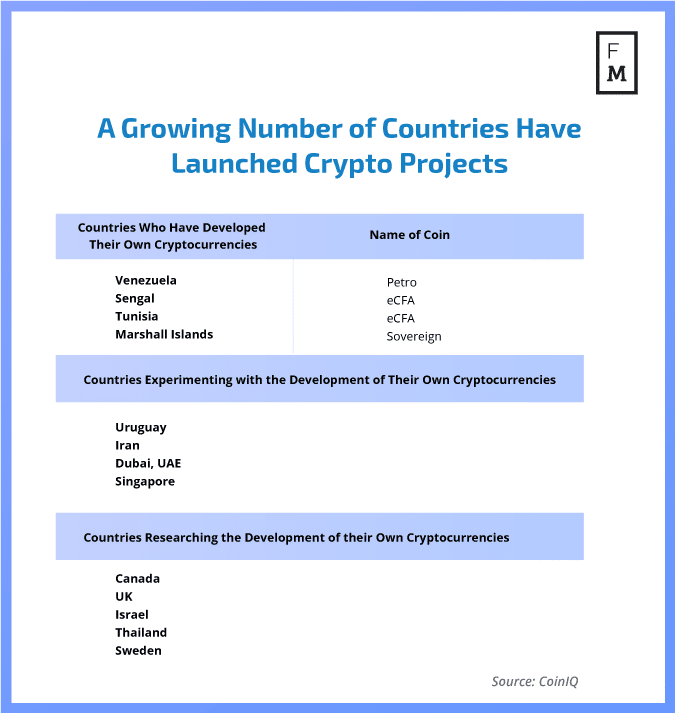

Perhaps the most infamous example of a national cryptocurrency gone wrong is the Venezuelan Petro. The Petro, a cryptocurrency that is allegedly backed by oil and other commodities, was launched by President Nicholas Maduro as a possible solution to the country’s financial crisis. Hyperinflation has struck the nation’s economy so severely that in the worst of times, a loaf of bread costs close to 500,000 Bolivars.

At the launch of the Petro, the Venezuelan government is alleged to have allocated five billion barrels of oil to it. Each single Petro coin was worth one barrel. The government said that the Petro would be “a second accounting unit of the Republic and will begin operations as a mandatory accounting unit of our PDVSA oil industry.”

“The new Bolivar with five zeroes dropped is not “anchored” (to the #petro#fraud crypto) as #maduro said). It is rather attached to an ANVIL amd will sink faster.” No policies against #hyperinflation but more petrol for the fire. https://t.co/J6FjHsp01A

Preceding the launch of the Petro, the Venezuelan government came under fire from other government bodies around the world, which accused the country of developing the Petro as a way to evade sanctions and access international debt markets. Some governments even barred their own citizens from taking part in the Petro’s token sale.

Almost immediately after the launch of the Petro, accusations emerged that Maduro and his associates were directly involved in a huge money-laundering scheme with the Petro at the center of it. More specifically, the allegations were made in connection with the $735 million that was raised within hours after the Petro went public.

“The mention of agreements with the ghost company ‘Aerotrading’, does not figure in the [Petro’s] ecosystem of development and neither on the internet,” a report by the company read (translated from Spanish.) “In addition, the Zeus company dissociates itself from the agreements made, while the Venezuelan government is still naming the companies and the NEM foundation as the parties directly responsible for the integration of the Token [Petro].”

Interesante...

La cuestión es que el 'Petro' es un #ENTE fantasma ?

No llega ni a la categoría de criptomoneda basura...

Suspicions were raised even higher when a Reuter’s investigation conducted in August of 2018 revealed that the man who had been named as Venezuela’s Superintendent of Cryptocurrencies did not have an industry in the Ministry of Finance and that the office’s promoted website did not exist. Ataparire, the parish where the project’s oil reserves were supposedly based, had seen no oil-related activity; oil rigs found in the area appeared to have lain abandoned for some time.

Additionally, Reuters could not identify any actual human being that had been able to buy the petro at all. In the end, it seems that the project was one giant lie.

As you can perhaps imagine, this did not do wonders for the cryptocurrency industry. Most of the public saw yet another example of cryptocurrency being linked with illicit activity. However, the debacle did serve as a learning experience for governments interested in learning how to better regulate their own interactions with cryptocurrency projects.

The US Fights Against the Iranian ‘PayMon’

Another national cryptocurrency project that has garnered quite a bit of negative attention is the Iranian PayMon, a digital currency that would be backed by national reserves of gold. Similar to the Petro, the project has been criticized for having been developed as a method of evading international sanctions.

Anticipating these, US lawmakers introduced a bill due impose further sanctions that would hinder the development and use of the PayMon. The “Blocking Iran Illicit Finance Act,” which was published in late 2018, would place sanctions on foreign individuals who are involved in the transfer, holding, sale, or supply of the PayMon.

#Iran's economy has been creaking badly under the reimposed US sanctions, which were activated in H2/2018; the #PayMon is one of those innovations borne of dire circumstances

The act also requests that a comprehensive report on the project be made to Congress. A similar bill was introduced by Ted Cruz around the same time.

According to a report from CoinTelegraph, cryptocurrencies have already been widely used by Iranians who are seeking to evade sanctions. Additionally, crypto and blockchain technology have been eyed as an alternative to the SWIFT financial messaging services, as a number of Iranian banks have been forcibly removed from the SWIFT system.

Iran’s crypto-rial has sparked controversies. While the gold-backed "PayMon" can be used to invest in the country, critics suggest that #Iran is trying to evade U.S sanctions. The question now is: does it have a future? #paymon#cryptocurrency#CryptoNewshttps://t.co/8iUpww5vD0

So, Iran is in a tight spot. A sovereign cryptocurrency could indeed improve the country’s own financial services--a problem that is particularly acute due to the absence of SWIFT from some of its banks. However, its financial and political situations could worsen more generally if the countries pursues the creation of the PayMon any further.

Governments Could Reduce Crime and Increase Efficiency With their Own Cryptocurrencies

Despite the mixed results of the national cryptocurrency projects that have appeared over the course of the last two years, many analysts believe that a growing number of countries will eventually have some kind of cryptocurrency or blockchain-based system within their financial infrastructure.

In fact, Christine Lagarde, head of the International Monetary Fund (IMF), recently endorsed the concept of national cryptocurrencies in order to prevent systems like the Bitcoin network from becoming havens for money-launderers and other kinds of criminals.

Lagarde also said that integrating regulated cryptocurrency and blockchain systems into national banks could greatly increase efficiency and lower costs. “The advantage is clear. Your payment would be immediate, safe, cheap, and potentially semi-anonymous,” she explained, speaking at a fintech conference in Singapore last year.

“Putting it another way. The central bank focuses on its comparative advantage – back-end settlement – and financial institutions and start-ups are free to focus on what they do best – client interface and innovation. This is [a] public-private partnership at its best.”

Countries With Legit Projects are Plugging Along, But Most Projects are Far From Release

One country that is working on developing a blockchain-based system that could improve its own banking services is Thailand. The Thai central bank, along with eight other Thai financial institutions, teamed up in August to create a cryptocurrency to be used between banks. The announcement of the coin is meant to “enhance the efficiency of the Thai financial market infrastructure.”

After the interbank cryptocurrency system is established, the project is set to expand into cross-border transactions. “Building upon the findings and outcomes from Phase 1, the project participants aim to further develop the capabilities of the prototype for broader functions including third party funds transfer and cross-border funds transfer,” the announcement explained. No public news of the project has emerged since its launch.

A number of similar projects have emerged--projects that appear to be well-regulated and created with the intent to operate in line with international sanctions.

Tunisia has developed a transaction platform that would also serve as a digital ID; it would be used for salary transfers, loans, and bill payments. Sweden is creating the ‘e-krona’ - among other use-cases, the e-krona is set to be used by asylum seekers as a verifiable and secure method of transaction. A similar platform is being developed by Finnish company MONI in collaboration with the Finnish government.

Some countries are even working to create cryptocurrencies as a way to become less reliant on the international economy. Marshall Islands President Hilda Heina has declared her support for the creation of a sovereign cryptocurrency as a way to become more independent from the US and its banking system. A growing number of small island nations have also been considering developing their own cryptocurrencies for similar reasons.

It’s unclear when any of these projects will come to fruition. However, what’s clear is that the speculation around these projects has increased, so too has the apparent need for international regulations and infrastructure that would allow these cryptocurrencies to function on a legal scale.

In late 2017 and early 2018, national stablecoins were the talk of the industry. Rumors - some confirmed, some unconfirmed - that Estonia, Sweden, Iran, Russia, Venezuela, and others may be exploring the launch of a national stablecoin spread like wildfire.

Many believed that the launch of national cryptocurrencies was the thing - the thing that would finally prove cryptocurrencies as a valid transactional instrument, as a worthy investment, as more than just a fad.

However, the hype around many of these national cryptocurrency projects--just like the hype around many cryptocurrency projects--came and went. In most cases, national crypto initiatives faded out of the spotlight or disappeared altogether; in the worst cases, these national crypto projects were used as vehicles to avoid international sanctions and commit large-scale financial crimes.

How have these projects evolved over the last year? And how have they influenced the world’s view of cryptocurrency?

Whatever Happened with the Petro?

Perhaps the most infamous example of a national cryptocurrency gone wrong is the Venezuelan Petro. The Petro, a cryptocurrency that is allegedly backed by oil and other commodities, was launched by President Nicholas Maduro as a possible solution to the country’s financial crisis. Hyperinflation has struck the nation’s economy so severely that in the worst of times, a loaf of bread costs close to 500,000 Bolivars.

At the launch of the Petro, the Venezuelan government is alleged to have allocated five billion barrels of oil to it. Each single Petro coin was worth one barrel. The government said that the Petro would be “a second accounting unit of the Republic and will begin operations as a mandatory accounting unit of our PDVSA oil industry.”

“The new Bolivar with five zeroes dropped is not “anchored” (to the #petro#fraud crypto) as #maduro said). It is rather attached to an ANVIL amd will sink faster.” No policies against #hyperinflation but more petrol for the fire. https://t.co/J6FjHsp01A

Preceding the launch of the Petro, the Venezuelan government came under fire from other government bodies around the world, which accused the country of developing the Petro as a way to evade sanctions and access international debt markets. Some governments even barred their own citizens from taking part in the Petro’s token sale.

Almost immediately after the launch of the Petro, accusations emerged that Maduro and his associates were directly involved in a huge money-laundering scheme with the Petro at the center of it. More specifically, the allegations were made in connection with the $735 million that was raised within hours after the Petro went public.

“The mention of agreements with the ghost company ‘Aerotrading’, does not figure in the [Petro’s] ecosystem of development and neither on the internet,” a report by the company read (translated from Spanish.) “In addition, the Zeus company dissociates itself from the agreements made, while the Venezuelan government is still naming the companies and the NEM foundation as the parties directly responsible for the integration of the Token [Petro].”

Interesante...

La cuestión es que el 'Petro' es un #ENTE fantasma ?

No llega ni a la categoría de criptomoneda basura...

Suspicions were raised even higher when a Reuter’s investigation conducted in August of 2018 revealed that the man who had been named as Venezuela’s Superintendent of Cryptocurrencies did not have an industry in the Ministry of Finance and that the office’s promoted website did not exist. Ataparire, the parish where the project’s oil reserves were supposedly based, had seen no oil-related activity; oil rigs found in the area appeared to have lain abandoned for some time.

Additionally, Reuters could not identify any actual human being that had been able to buy the petro at all. In the end, it seems that the project was one giant lie.

As you can perhaps imagine, this did not do wonders for the cryptocurrency industry. Most of the public saw yet another example of cryptocurrency being linked with illicit activity. However, the debacle did serve as a learning experience for governments interested in learning how to better regulate their own interactions with cryptocurrency projects.

The US Fights Against the Iranian ‘PayMon’

Another national cryptocurrency project that has garnered quite a bit of negative attention is the Iranian PayMon, a digital currency that would be backed by national reserves of gold. Similar to the Petro, the project has been criticized for having been developed as a method of evading international sanctions.

Anticipating these, US lawmakers introduced a bill due impose further sanctions that would hinder the development and use of the PayMon. The “Blocking Iran Illicit Finance Act,” which was published in late 2018, would place sanctions on foreign individuals who are involved in the transfer, holding, sale, or supply of the PayMon.

#Iran's economy has been creaking badly under the reimposed US sanctions, which were activated in H2/2018; the #PayMon is one of those innovations borne of dire circumstances

The act also requests that a comprehensive report on the project be made to Congress. A similar bill was introduced by Ted Cruz around the same time.

According to a report from CoinTelegraph, cryptocurrencies have already been widely used by Iranians who are seeking to evade sanctions. Additionally, crypto and blockchain technology have been eyed as an alternative to the SWIFT financial messaging services, as a number of Iranian banks have been forcibly removed from the SWIFT system.

Iran’s crypto-rial has sparked controversies. While the gold-backed "PayMon" can be used to invest in the country, critics suggest that #Iran is trying to evade U.S sanctions. The question now is: does it have a future? #paymon#cryptocurrency#CryptoNewshttps://t.co/8iUpww5vD0

So, Iran is in a tight spot. A sovereign cryptocurrency could indeed improve the country’s own financial services--a problem that is particularly acute due to the absence of SWIFT from some of its banks. However, its financial and political situations could worsen more generally if the countries pursues the creation of the PayMon any further.

Governments Could Reduce Crime and Increase Efficiency With their Own Cryptocurrencies

Despite the mixed results of the national cryptocurrency projects that have appeared over the course of the last two years, many analysts believe that a growing number of countries will eventually have some kind of cryptocurrency or blockchain-based system within their financial infrastructure.

In fact, Christine Lagarde, head of the International Monetary Fund (IMF), recently endorsed the concept of national cryptocurrencies in order to prevent systems like the Bitcoin network from becoming havens for money-launderers and other kinds of criminals.

Lagarde also said that integrating regulated cryptocurrency and blockchain systems into national banks could greatly increase efficiency and lower costs. “The advantage is clear. Your payment would be immediate, safe, cheap, and potentially semi-anonymous,” she explained, speaking at a fintech conference in Singapore last year.

“Putting it another way. The central bank focuses on its comparative advantage – back-end settlement – and financial institutions and start-ups are free to focus on what they do best – client interface and innovation. This is [a] public-private partnership at its best.”

Countries With Legit Projects are Plugging Along, But Most Projects are Far From Release

One country that is working on developing a blockchain-based system that could improve its own banking services is Thailand. The Thai central bank, along with eight other Thai financial institutions, teamed up in August to create a cryptocurrency to be used between banks. The announcement of the coin is meant to “enhance the efficiency of the Thai financial market infrastructure.”

After the interbank cryptocurrency system is established, the project is set to expand into cross-border transactions. “Building upon the findings and outcomes from Phase 1, the project participants aim to further develop the capabilities of the prototype for broader functions including third party funds transfer and cross-border funds transfer,” the announcement explained. No public news of the project has emerged since its launch.

A number of similar projects have emerged--projects that appear to be well-regulated and created with the intent to operate in line with international sanctions.

Tunisia has developed a transaction platform that would also serve as a digital ID; it would be used for salary transfers, loans, and bill payments. Sweden is creating the ‘e-krona’ - among other use-cases, the e-krona is set to be used by asylum seekers as a verifiable and secure method of transaction. A similar platform is being developed by Finnish company MONI in collaboration with the Finnish government.

Some countries are even working to create cryptocurrencies as a way to become less reliant on the international economy. Marshall Islands President Hilda Heina has declared her support for the creation of a sovereign cryptocurrency as a way to become more independent from the US and its banking system. A growing number of small island nations have also been considering developing their own cryptocurrencies for similar reasons.

It’s unclear when any of these projects will come to fruition. However, what’s clear is that the speculation around these projects has increased, so too has the apparent need for international regulations and infrastructure that would allow these cryptocurrencies to function on a legal scale.

Rachel is a self-taught crypto geek and a passionate writer. She believes in the power that the written word has to educate, connect and empower individuals to make positive and powerful financial choices. She is the Podcast Host and a Cryptocurrency Editor at Finance Magnates.

CoinRoutes Adds Dedicated Wincent FIX Sessions for Institutional Clients

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.