>

BIS Releases Data on Effects of Intervention in Peru's $700 Million Per Day FX Market

BIS Releases Data on Effects of Intervention in Peru's $700 Million Per Day FX Market

Wednesday,18/09/2013|11:12GMTby

Andrew Saks McLeod

The Bank For International Settlements has today released the results of a study in which it extrapolated data from Peru's interbank FX market over a two year period to examine the effects of FX intervention.

South America is a relatively unknown quantity among many market participants, its own rapidly developing FX industry having remained in the shadow of its mainstream counterparts such as Europe, North America and the Far East – until now.

Today, the Bank for International Settlements (BIS), released a report in which the results of its examination of the asymmetric effects of FOREX intervention using intraday data are documented, using evidence from the Peruvian market.

Proprietary Platform Serves Domestic Market

Peru, according to the report, has a very domestic-oriented inter-bank FX market, being primarily a local market based on spot transactions. Although, there is a forwards and options market, it is very small compared to the nation’s spot FX market.

It operates between 9 am and 1:30 pm, Monday through Friday. The transactions are settled same day, under a real time gross settlement (RTGS) system, on a payment versus payment platform through each bank's account at the central bank.

The participants in the FX market are commercial banks. However, about five banks are the major players in terms of average amount traded. Currently, the average amount traded in the interbank spot forex market is around $700 million a day. The record amount for one day is approximately $1,700 million, representing almost 1 percent of GDP.

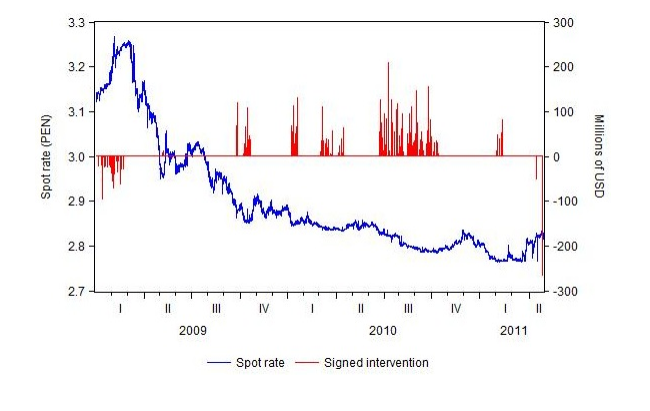

The initial point of interest is that this represents the first time, undisclosed and comprehensive intraday intervention data - minute by minute data points for all trading days between January 2009 and April 2011 - have been used for Peru.

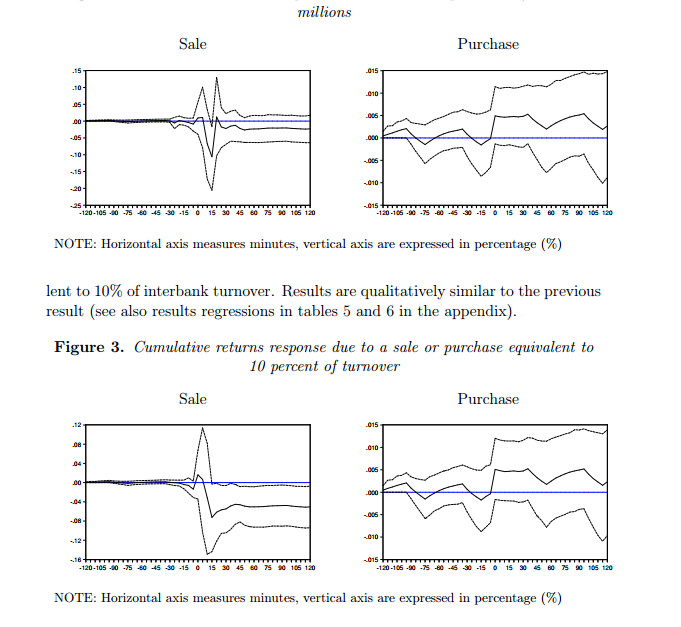

Secondly, the paper shows that Central Bank interventions in the foreign exchange market have asymmetric effects on the spot exchange rate.

In particular, sale interventions have a greater effect on exchange rate than purchase interventions. This result is robust to event study regressions, and to a SVAR identification proposed in the research paper.

Lastly, the paper provides a simple signaling framework which formalizes the asymmetric effect, whereby sale interventions are more effective than purchase interventions.

Asymmetric Loss Functions

For policy makers who participate in the forex market, the dangers of sharp exchange rate depreciations are markedly different from those of exchange rate appreciations. Exchange rate depreciations are linked to stress episodes associated with financial crises. Fear of floating entails, mostly a fear of depreciation. Large and abrupt depreciations trigger fears of financial distress. Such fears are particularly acute in emerging market economies whose financial markets are vulnerable - for example, as a result of financial dollarization.

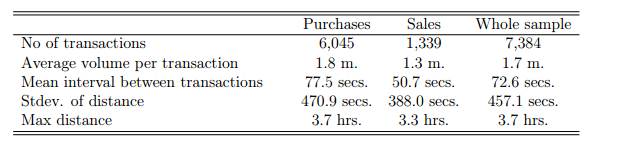

Descriptive Statistics From Transaction-Level Intervention Data

In contrast, exchange rate appreciations are not linked to short-run financial crises, but to capital flow bonanzas. Thus, fear of appreciation is more related to fear of misallocation of resources between tradeable and non-tradeable sectors, and fear of excessive credit booms.

The BIS considers that in this case, the asymmetry turns on the fact that large depreciations are avoided because they may imply financial crisis in the short run, while sharp or persistent appreciations are avoided, because these may harm growth prospects.

An asymmetric reaction function, in turn, implies that for a given pressure of appreciation or depreciation, the central bank intervenes differently, depending on whether it is purchasing or selling. This means that the features of purchase and sale interventions differ in terms of the volume of each transaction, daily aggregate volumes, dispersion of intervention transactions across market participants and intraday timing of intervention.

The data used to compile this particular report was extrapolated from trading activity between 2009 and 2011 in Peru’s FX markets. The paper shows that central bank interventions in the FX market have asymmetric effects on the spot exchange rate. In particular, sale interventions are more effective than purchase interventions. In addition, the conclusion reached by the BIS confirms a previous finding for Peru, which was documented in Flores in 2003.

Latin America in general, is fast becoming a region of interest among the institutional FX sector. For a full and detailed report on the entire dynamics of the FX landscape in Latin America, Forex Magnates research can be purchased here.

South America is a relatively unknown quantity among many market participants, its own rapidly developing FX industry having remained in the shadow of its mainstream counterparts such as Europe, North America and the Far East – until now.

Today, the Bank for International Settlements (BIS), released a report in which the results of its examination of the asymmetric effects of FOREX intervention using intraday data are documented, using evidence from the Peruvian market.

Proprietary Platform Serves Domestic Market

Peru, according to the report, has a very domestic-oriented inter-bank FX market, being primarily a local market based on spot transactions. Although, there is a forwards and options market, it is very small compared to the nation’s spot FX market.

It operates between 9 am and 1:30 pm, Monday through Friday. The transactions are settled same day, under a real time gross settlement (RTGS) system, on a payment versus payment platform through each bank's account at the central bank.

The participants in the FX market are commercial banks. However, about five banks are the major players in terms of average amount traded. Currently, the average amount traded in the interbank spot forex market is around $700 million a day. The record amount for one day is approximately $1,700 million, representing almost 1 percent of GDP.

The initial point of interest is that this represents the first time, undisclosed and comprehensive intraday intervention data - minute by minute data points for all trading days between January 2009 and April 2011 - have been used for Peru.

Secondly, the paper shows that Central Bank interventions in the foreign exchange market have asymmetric effects on the spot exchange rate.

In particular, sale interventions have a greater effect on exchange rate than purchase interventions. This result is robust to event study regressions, and to a SVAR identification proposed in the research paper.

Lastly, the paper provides a simple signaling framework which formalizes the asymmetric effect, whereby sale interventions are more effective than purchase interventions.

Asymmetric Loss Functions

For policy makers who participate in the forex market, the dangers of sharp exchange rate depreciations are markedly different from those of exchange rate appreciations. Exchange rate depreciations are linked to stress episodes associated with financial crises. Fear of floating entails, mostly a fear of depreciation. Large and abrupt depreciations trigger fears of financial distress. Such fears are particularly acute in emerging market economies whose financial markets are vulnerable - for example, as a result of financial dollarization.

Descriptive Statistics From Transaction-Level Intervention Data

In contrast, exchange rate appreciations are not linked to short-run financial crises, but to capital flow bonanzas. Thus, fear of appreciation is more related to fear of misallocation of resources between tradeable and non-tradeable sectors, and fear of excessive credit booms.

The BIS considers that in this case, the asymmetry turns on the fact that large depreciations are avoided because they may imply financial crisis in the short run, while sharp or persistent appreciations are avoided, because these may harm growth prospects.

An asymmetric reaction function, in turn, implies that for a given pressure of appreciation or depreciation, the central bank intervenes differently, depending on whether it is purchasing or selling. This means that the features of purchase and sale interventions differ in terms of the volume of each transaction, daily aggregate volumes, dispersion of intervention transactions across market participants and intraday timing of intervention.

The data used to compile this particular report was extrapolated from trading activity between 2009 and 2011 in Peru’s FX markets. The paper shows that central bank interventions in the FX market have asymmetric effects on the spot exchange rate. In particular, sale interventions are more effective than purchase interventions. In addition, the conclusion reached by the BIS confirms a previous finding for Peru, which was documented in Flores in 2003.

Latin America in general, is fast becoming a region of interest among the institutional FX sector. For a full and detailed report on the entire dynamics of the FX landscape in Latin America, Forex Magnates research can be purchased here.

Opetek Launches ARIUS, Pilots AI Reasoning Platform at Tier 1 Investment Bank

Featured Videos

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.