The Moscow Exchange (MOEX) implemented today an update to its ASTS FX market trading and clearing system as per announcement. The updated version of the system will have many technical improvements and two major functional changes.

The most important technical change seems to be risk netting between FX and derivatives markets. Forex Magnates talked with Alexander Ageev,Vice-President and Head of FX at MOEX to understand how he sees this will help traders. Mr. Ageev explained: "The main idea of the innovation is that participants working on both derivative and FX markets will be able to net their collateral/margin obligations on both markets transferring position from serivatives market to the FX market and netting this with position on the FX market."

He provided an example: "A participant has a long position USD 1,000,000 at the derivatives market (came from USD/RUB futures trading) could transfer this position via SPECTRA (Derivative market platform) to the FX market where he is USD 500,000 short (derived from USD/RUB spot & swap trading) – then his net position will be USD 500,000 long and his margining obligations will change respectively. Obviously this innovation is positive for MOEX participants that work on both markets."

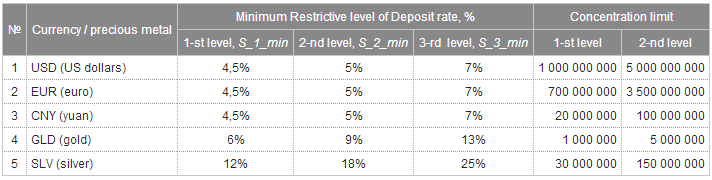

In the announcement MOEX described the two changes to its Risk Management system as novelties in the FX market. As a result of the first change individual risk parameters will become available for the MOEX FX market clearing members. They will be able to manage the risk parameters such as risk assessment range limits, at the level of settlement codes.

The second risk "novelty" change relates to concentration limits. The risk assessment limits used to calculate the single limit of a clearing member will depend on its value of obligations under trades. Two concentration limit levels are to be introduced. If the value of the obligations exceeds the first level concentration limit, risk parameters for the second level (higher margin rates broadening the risk assessment ranges) will be used. Similarly, even higher risk parameters of the third level are applied if the value of obligations exceeds the second level concentration limit.

This move by MOEX aims to unify the FX and precious metals markets risk management system with those of other exchange markets and enhance the financial sustainability of the exchange infrastructure according to the announcement.

Mr. Ageev explained to Forex Magnates the FX market risk management system changes at MOEX: "Individual risk parameters- This innovation allows a market participant to manage margining requirements on each separate Settlement code kept with the CCP individually. Settlement code in fact is an account with the CCP on which claims/obligations of the participant’s client are normally accounted and settled. So far (before the innovation is put in effect) participants do not have such flexibility and margining requirements are set up equally by the CCP for all settlement codes. So the innovation helps participants better control clients’ risks.

Concentration limits- In general this innovation allows the CCP better control participants’ risks using more flexible tools (increasing margining requirements) rather than simply switch them off the clearing system. Currently CCP risk management system blocks participants, which bring unaffordable risks to the clearing."