The transition to API banking requires proficiency in modern technologies like microservices and cloud-native environments.

Educating both internal and external stakeholders about API integration is critical.

Over the past years, API banking has evolved from a niche technological concept to a wellspring of innovation and revenue for banks and other financial institutions.

However, the journey towards effective API banking can be more complex than some industry observers suggest. As banks pivot from viewing APIs as mere technical tools to recognizing them as strategic business assets, they face challenges that are often overlooked amid the hype—from the need to reimagine their approach to APIs and educate customers to the IT expertise gap.

Three Stumbling Blocks Along the Way

While the promise of new revenue streams and enhanced customer experiences is alluring, the path to realizing these API banking benefits is not that simple.

First and most importantly, banks need to fundamentally reimagine their approach to APIs. Traditionally viewed as technical integration points, APIs must now be conceptualized as products in their own right.

This shift demands a comprehensive strategy that clearly defines the bank's API approach. Whether focusing on embedded offerings, marketplaces, or compliance-focused solutions, banks must carefully consider their objectives and capabilities to take full advantage of the opportunities API provides for their business.

There are a number of banks that have found their way. For example, the Spanish bank BBVA went the marketplace route and launched its API Market, making its APIs commercially available.

BBVA, the Spanish banking giant, is preparing to enter the stablecoin market, with plans to launch its own digital asset in 2025, supported by Visa. According to Francisco Maroto, BBVA’s head of digital assets and blockchain, the bank is currently participating in a new Visa… pic.twitter.com/EsU4rx0Xh4

— Digital Pound Foundation (@digitalpoundfdn) October 6, 2024

These APIs enable third-party developers to integrate BBVA’s banking services into their applications, improving user experiences and creating new services. All that while adding a new revenue stream to the bank—this business makes them a reported additional $7.1M in revenue.

There are a number of similar cases, but it doesn't mean these decisions come easy for all banks—they require a seismic shift in thinking that cannot be underestimated. Equally daunting is the IT expertise gap that some banks face. The transition to API banking often requires proficiency in cutting-edge technologies such as microservices and cloud-native environments.

For institutions still grappling with legacy systems, this creates both a technical challenge (updating systems) and a skills challenge (acquiring new expertise). So, banks must decide whether to build this expertise internally or seek external partnerships—a choice that will significantly impact their competitive position.

Finally, and perhaps the most overlooked challenge, is the need for customer and partner education. The complexities of API integration often necessitate intensive, personalized guidance. This is particularly true for the main “consumers” of APIs: other partners or units within banks with whom new services for end-users and businesses are being created.

These internal and external partners often require attention and guidance, relying heavily on face-to-face communication to understand and implement API solutions. While effective, such communication complicates the process and strains bank resources.

Seven Steps to Your API Success

Suavek Zajac, CTO at Tandem Bank, suggests that banks follow a pragmatic seven-step approach to navigate these challenges and unlock the full potential of API banking. The seven steps are:

Focusing on End-to-End Use Cases

As banks reimagine their approach to APIs, it's crucial to recognize that APIs are not just technical interfaces—they are products that require a customer-centric mindset. This means identifying and understanding the needs of all potential users, including downstream operational and back-office functions, regulatory bodies, and reporting entities, in addition to the end-users.

By adopting an end-to-end perspective, banks can create APIs that deliver value at every stage, enhancing efficiency and reducing operational bottlenecks.

Designing for All Scenarios

While it's tempting to focus on ideal use cases—the “happy path,” a robust API design must account for error conditions and fallback scenarios. Transactions may fail due to insufficient funds, network issues, or compliance flags. In such cases, the API should provide clear notifications to users, allowing them to understand the issue and take corrective action.

Moreover, APIs should enable operational teams to intervene when necessary. If a transaction is flagged for potential fraud, the API should facilitate a review process rather than simply rejecting the transaction. Planning for these contingencies improves user trust and satisfaction while ensuring compliance and operational efficiency.

Security and Compliance from Day One

In the banking industry, security and compliance are non-negotiable. APIs expose banking services to external entities, making them potential targets for cyberattacks. Therefore, security measures such as authentication, authorization, encryption, and penetration testing must be integral parts of the API development process from the outset.

Addressing security and compliance after the API is developed can lead to vulnerabilities and regulatory issues. Continuous monitoring is also essential to detect and respond to threats in real time. By embedding security and compliance into the API lifecycle from day one, banks can protect their assets and maintain customer trust.

Developer-Centric Design

APIs' primary audience is developers, and their experience can make or break a product's success. Comprehensive documentation, code samples, and easy-to-use sandboxes for experimentation are vital components of a developer-friendly API offering. These resources reduce the learning curve, enabling developers to integrate and test APIs efficiently.

Providing interactive documentation portals, software development kits (SDKs) in multiple programming languages, and responsive support channels can further enhance the developer experience. By investing in these areas, banks can foster a strong developer community, leading to increased adoption and innovation around their APIs.

Clear Pricing and Billing

Transparency in pricing is essential for building trust with API consumers. Banks need to establish clear pricing models and implement billing systems from the very beginning. Whether the pricing is based on usage, subscription tiers, or value-added services, it should be straightforward and easily accessible.

As banks venture into offering APIs as products, supporting customers throughout their journey becomes critical. Establishing dedicated customer success teams and professional services can significantly enhance the adoption and effective use of APIs. These teams act as trusted advisors, helping clients navigate the complexities of API integration, customization, and optimization.

By providing hands-on assistance, training, and ongoing support, customer success teams ensure clients can fully leverage the bank's APIs to achieve their business objectives. Professional services can offer tailored solutions, from initial implementation to scaling and optimization, thereby reducing time to market and increasing customer satisfaction.

This proactive approach strengthens client relationships and opens up additional revenue streams through premium support offerings. Investing in customer success and professional services demonstrates the bank's commitment to its client's success and differentiates its API offerings in a competitive market.

Leveraging Strategic Partnerships

Building strategic partnerships is a powerful way to expand the reach and capabilities of a bank's API ecosystem. Collaborating with fintech companies, technology providers, and other financial institutions can lead to innovative solutions that neither party could achieve independently.

Partnerships can enhance the value proposition of the bank's APIs by integrating complementary services, accessing new customer segments, and accelerating innovation through shared expertise. For example, partnering with a fintech startup specializing in AI could enable advanced analytics features within the bank's API offerings.

OpenAI has developed a system to track its progress toward building AI software capable of outperforming humans. https://t.co/x4jhitnPXp

Moreover, strategic alliances can help banks navigate regulatory landscapes, share development costs, and reduce time-to-market for new services. By actively seeking and nurturing partnerships, banks can create a more robust and versatile API ecosystem that drives mutual growth and benefits all stakeholders.

The Double-Edged Sword of API Banking

Despite challenges, the potential benefits of API banking remain substantial. Banks know this very well, with some allocating as much as 14% of their IT budget to APIs.

But even with significant investments, the path to successful API banking is neither straightforward nor guaranteed. It requires it all—a level of strategic thinking, technological adaptation, and industry collaboration that goes beyond mere technical implementation. Banks that will learn to navigate these complexities stand to gain significantly, potentially reshaping the competitive landscape of the industry.

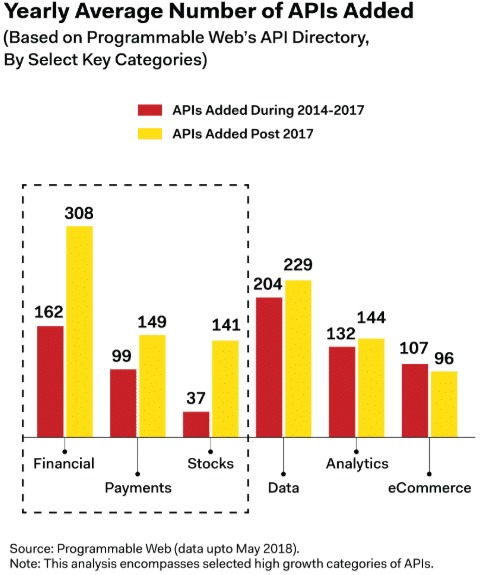

Yearly Average Number of APIs Added

Banks that have successfully established the right structure, including having a dedicated team responsible for API banking products or API marketplace, are thriving. In this journey, it's important that within each business unit—whether it be loans, deposits, cards, payments, or other areas—teams are focused on how their products can be transformed into API offerings for fintech partners.

API banking begins a new era of financial services. So, at the end of the day, the question is not whether banks will participate in API banking but how effectively they will be able to overcome these obstacles and take the lead in this new financial paradigm.

Over the past years, API banking has evolved from a niche technological concept to a wellspring of innovation and revenue for banks and other financial institutions.

However, the journey towards effective API banking can be more complex than some industry observers suggest. As banks pivot from viewing APIs as mere technical tools to recognizing them as strategic business assets, they face challenges that are often overlooked amid the hype—from the need to reimagine their approach to APIs and educate customers to the IT expertise gap.

Three Stumbling Blocks Along the Way

While the promise of new revenue streams and enhanced customer experiences is alluring, the path to realizing these API banking benefits is not that simple.

First and most importantly, banks need to fundamentally reimagine their approach to APIs. Traditionally viewed as technical integration points, APIs must now be conceptualized as products in their own right.

This shift demands a comprehensive strategy that clearly defines the bank's API approach. Whether focusing on embedded offerings, marketplaces, or compliance-focused solutions, banks must carefully consider their objectives and capabilities to take full advantage of the opportunities API provides for their business.

There are a number of banks that have found their way. For example, the Spanish bank BBVA went the marketplace route and launched its API Market, making its APIs commercially available.

BBVA, the Spanish banking giant, is preparing to enter the stablecoin market, with plans to launch its own digital asset in 2025, supported by Visa. According to Francisco Maroto, BBVA’s head of digital assets and blockchain, the bank is currently participating in a new Visa… pic.twitter.com/EsU4rx0Xh4

— Digital Pound Foundation (@digitalpoundfdn) October 6, 2024

These APIs enable third-party developers to integrate BBVA’s banking services into their applications, improving user experiences and creating new services. All that while adding a new revenue stream to the bank—this business makes them a reported additional $7.1M in revenue.

There are a number of similar cases, but it doesn't mean these decisions come easy for all banks—they require a seismic shift in thinking that cannot be underestimated. Equally daunting is the IT expertise gap that some banks face. The transition to API banking often requires proficiency in cutting-edge technologies such as microservices and cloud-native environments.

For institutions still grappling with legacy systems, this creates both a technical challenge (updating systems) and a skills challenge (acquiring new expertise). So, banks must decide whether to build this expertise internally or seek external partnerships—a choice that will significantly impact their competitive position.

Finally, and perhaps the most overlooked challenge, is the need for customer and partner education. The complexities of API integration often necessitate intensive, personalized guidance. This is particularly true for the main “consumers” of APIs: other partners or units within banks with whom new services for end-users and businesses are being created.

These internal and external partners often require attention and guidance, relying heavily on face-to-face communication to understand and implement API solutions. While effective, such communication complicates the process and strains bank resources.

Seven Steps to Your API Success

Suavek Zajac, CTO at Tandem Bank, suggests that banks follow a pragmatic seven-step approach to navigate these challenges and unlock the full potential of API banking. The seven steps are:

Focusing on End-to-End Use Cases

As banks reimagine their approach to APIs, it's crucial to recognize that APIs are not just technical interfaces—they are products that require a customer-centric mindset. This means identifying and understanding the needs of all potential users, including downstream operational and back-office functions, regulatory bodies, and reporting entities, in addition to the end-users.

By adopting an end-to-end perspective, banks can create APIs that deliver value at every stage, enhancing efficiency and reducing operational bottlenecks.

Designing for All Scenarios

While it's tempting to focus on ideal use cases—the “happy path,” a robust API design must account for error conditions and fallback scenarios. Transactions may fail due to insufficient funds, network issues, or compliance flags. In such cases, the API should provide clear notifications to users, allowing them to understand the issue and take corrective action.

Moreover, APIs should enable operational teams to intervene when necessary. If a transaction is flagged for potential fraud, the API should facilitate a review process rather than simply rejecting the transaction. Planning for these contingencies improves user trust and satisfaction while ensuring compliance and operational efficiency.

Security and Compliance from Day One

In the banking industry, security and compliance are non-negotiable. APIs expose banking services to external entities, making them potential targets for cyberattacks. Therefore, security measures such as authentication, authorization, encryption, and penetration testing must be integral parts of the API development process from the outset.

Addressing security and compliance after the API is developed can lead to vulnerabilities and regulatory issues. Continuous monitoring is also essential to detect and respond to threats in real time. By embedding security and compliance into the API lifecycle from day one, banks can protect their assets and maintain customer trust.

Developer-Centric Design

APIs' primary audience is developers, and their experience can make or break a product's success. Comprehensive documentation, code samples, and easy-to-use sandboxes for experimentation are vital components of a developer-friendly API offering. These resources reduce the learning curve, enabling developers to integrate and test APIs efficiently.

Providing interactive documentation portals, software development kits (SDKs) in multiple programming languages, and responsive support channels can further enhance the developer experience. By investing in these areas, banks can foster a strong developer community, leading to increased adoption and innovation around their APIs.

Clear Pricing and Billing

Transparency in pricing is essential for building trust with API consumers. Banks need to establish clear pricing models and implement billing systems from the very beginning. Whether the pricing is based on usage, subscription tiers, or value-added services, it should be straightforward and easily accessible.

As banks venture into offering APIs as products, supporting customers throughout their journey becomes critical. Establishing dedicated customer success teams and professional services can significantly enhance the adoption and effective use of APIs. These teams act as trusted advisors, helping clients navigate the complexities of API integration, customization, and optimization.

By providing hands-on assistance, training, and ongoing support, customer success teams ensure clients can fully leverage the bank's APIs to achieve their business objectives. Professional services can offer tailored solutions, from initial implementation to scaling and optimization, thereby reducing time to market and increasing customer satisfaction.

This proactive approach strengthens client relationships and opens up additional revenue streams through premium support offerings. Investing in customer success and professional services demonstrates the bank's commitment to its client's success and differentiates its API offerings in a competitive market.

Leveraging Strategic Partnerships

Building strategic partnerships is a powerful way to expand the reach and capabilities of a bank's API ecosystem. Collaborating with fintech companies, technology providers, and other financial institutions can lead to innovative solutions that neither party could achieve independently.

Partnerships can enhance the value proposition of the bank's APIs by integrating complementary services, accessing new customer segments, and accelerating innovation through shared expertise. For example, partnering with a fintech startup specializing in AI could enable advanced analytics features within the bank's API offerings.

OpenAI has developed a system to track its progress toward building AI software capable of outperforming humans. https://t.co/x4jhitnPXp

Moreover, strategic alliances can help banks navigate regulatory landscapes, share development costs, and reduce time-to-market for new services. By actively seeking and nurturing partnerships, banks can create a more robust and versatile API ecosystem that drives mutual growth and benefits all stakeholders.

The Double-Edged Sword of API Banking

Despite challenges, the potential benefits of API banking remain substantial. Banks know this very well, with some allocating as much as 14% of their IT budget to APIs.

But even with significant investments, the path to successful API banking is neither straightforward nor guaranteed. It requires it all—a level of strategic thinking, technological adaptation, and industry collaboration that goes beyond mere technical implementation. Banks that will learn to navigate these complexities stand to gain significantly, potentially reshaping the competitive landscape of the industry.

Yearly Average Number of APIs Added

Banks that have successfully established the right structure, including having a dedicated team responsible for API banking products or API marketplace, are thriving. In this journey, it's important that within each business unit—whether it be loans, deposits, cards, payments, or other areas—teams are focused on how their products can be transformed into API offerings for fintech partners.

API banking begins a new era of financial services. So, at the end of the day, the question is not whether banks will participate in API banking but how effectively they will be able to overcome these obstacles and take the lead in this new financial paradigm.

Spotex Connects Execution Venue to BitGo Custody and Settlement Network

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.