>

Hong Kong Regulator Calls For Greater Transparency - HKMA To Implement Trade Reporting Structure in July

Hong Kong Regulator Calls For Greater Transparency - HKMA To Implement Trade Reporting Structure in July

Thursday,20/06/2013|10:22GMTby

Andrew Saks McLeod

Following the lead taken by the CFTC in US, Hong Kong's HKMA has developed a set of rules for the reporting of all OTC derivatives trades via an electronic system, with FX NDFs being in the frame.

The parameters of the ever-changing and evolving regulatory environment in which OTC derivatives companies find themselves nowadays is making its presence felt on an international level, and such rules aimed at creating greater transparency within the markets are not just the preserve of the US regulators.

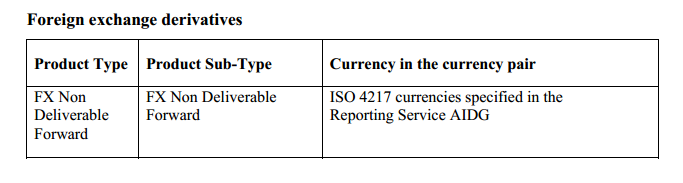

Hong Kong’s regulatory authority, the Hong Kong Monetary Association (HKMA) is very much engaged in establishing the final stages of its trade reporting service which is due to come into effect in July 2013, under which FX Non Deliverable Forwards will be classified as reportable instruments.

According to the regulator, an electronic system for collecting, keeping and maintaining details of OTC derivatives transactions efficiently and securely, primarily for market participants to meet the statutory reporting requirements under the OTC regulatory regime will be provided, and all eligible entities will be required to operate the system.

Entities eligible to subscribe to the Trade Reporting Service are either:

• Entities subject to mandatory reporting requirement under the OTC regulatory regime, or

• Other entities at the discretion of and subject to conditions specified by the HKMA.

Scope and Structure

On April 30 this year the HKMA set out its scope for trade reporting, which is depicted here:

Rather in the same vein as the contributing factors toward the commencement of the Dodd-Frank Wall Street Reform Act in the United States, the HKMA cites a global movement to improve transparency and reduce counterparty risks in the OTC derivatives markets as being a direct result of the global financial crisis in 2008.

The HKMA defines a trade repository as a centralized registry which maintains an electronic database of records of OTC derivatives transactions. By collecting and providing OTC derivatives transactions information to regulatory authorities, the TR plays a vital role in supporting authorities in carrying out their market surveillance responsibilities, which will help maintain stability of the financial systems.

It also helps increase transparency in the market, promotes standardization and provides a level of consistency in the quality and availability of transaction data.

Development Period

The HKMA initially announced in December 2010 its intention to establish a TR in Hong Kong under the Central Moneymarkets Unit (CMU), and that a link will be developed between the TR and the CCP for OTC derivatives to be launched by Hong Kong Exchanges and Clearing Ltd. to allow eligible transactions to be passed to the CCP for central clearing.

The HKMA also worked in concert with the Government and the Securities and Futures Commission (SFC) to build a regulatory regime for the OTC derivatives markets under the Securities and Futures Ordinance (SFO), including requirements for mandatory reporting to the TR of the HKMA and mandatory clearing at designated CCPs.

Interim Arrangement Finalized

In March 2013, the HKMA consulted the banking industry on introducing an Interim Reporting Arrangement to require reporting of OTC derivatives transactions to the TR of the HKMA.

The Interim Reporting Arrangement was targeted to be implemented within 2013, and was expected to remain in effect until the regulatory regime under the SFO takes effect.

Functionality

The HKMA has confirmed that it will apply charges to market participants for the reporting service, which will be payable in Hong Kong Dollars and will be provided to members on the 10th day of each month. The actual fee scale has not yet been confirmed, however.

Transactions reported to the HKTR will be effected by agreements between the parties involved in the transactions. The fact that they are reported to and maintained by the HKTR does not of itself confer any legally binding effect on such transactions.

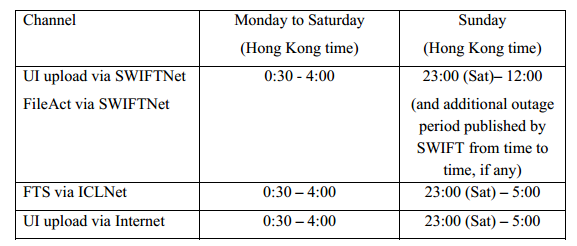

Operating Times for Sending Trade Reports to HKTR

The parameters of the ever-changing and evolving regulatory environment in which OTC derivatives companies find themselves nowadays is making its presence felt on an international level, and such rules aimed at creating greater transparency within the markets are not just the preserve of the US regulators.

Hong Kong’s regulatory authority, the Hong Kong Monetary Association (HKMA) is very much engaged in establishing the final stages of its trade reporting service which is due to come into effect in July 2013, under which FX Non Deliverable Forwards will be classified as reportable instruments.

According to the regulator, an electronic system for collecting, keeping and maintaining details of OTC derivatives transactions efficiently and securely, primarily for market participants to meet the statutory reporting requirements under the OTC regulatory regime will be provided, and all eligible entities will be required to operate the system.

Entities eligible to subscribe to the Trade Reporting Service are either:

• Entities subject to mandatory reporting requirement under the OTC regulatory regime, or

• Other entities at the discretion of and subject to conditions specified by the HKMA.

Scope and Structure

On April 30 this year the HKMA set out its scope for trade reporting, which is depicted here:

Rather in the same vein as the contributing factors toward the commencement of the Dodd-Frank Wall Street Reform Act in the United States, the HKMA cites a global movement to improve transparency and reduce counterparty risks in the OTC derivatives markets as being a direct result of the global financial crisis in 2008.

The HKMA defines a trade repository as a centralized registry which maintains an electronic database of records of OTC derivatives transactions. By collecting and providing OTC derivatives transactions information to regulatory authorities, the TR plays a vital role in supporting authorities in carrying out their market surveillance responsibilities, which will help maintain stability of the financial systems.

It also helps increase transparency in the market, promotes standardization and provides a level of consistency in the quality and availability of transaction data.

Development Period

The HKMA initially announced in December 2010 its intention to establish a TR in Hong Kong under the Central Moneymarkets Unit (CMU), and that a link will be developed between the TR and the CCP for OTC derivatives to be launched by Hong Kong Exchanges and Clearing Ltd. to allow eligible transactions to be passed to the CCP for central clearing.

The HKMA also worked in concert with the Government and the Securities and Futures Commission (SFC) to build a regulatory regime for the OTC derivatives markets under the Securities and Futures Ordinance (SFO), including requirements for mandatory reporting to the TR of the HKMA and mandatory clearing at designated CCPs.

Interim Arrangement Finalized

In March 2013, the HKMA consulted the banking industry on introducing an Interim Reporting Arrangement to require reporting of OTC derivatives transactions to the TR of the HKMA.

The Interim Reporting Arrangement was targeted to be implemented within 2013, and was expected to remain in effect until the regulatory regime under the SFO takes effect.

Functionality

The HKMA has confirmed that it will apply charges to market participants for the reporting service, which will be payable in Hong Kong Dollars and will be provided to members on the 10th day of each month. The actual fee scale has not yet been confirmed, however.

Transactions reported to the HKTR will be effected by agreements between the parties involved in the transactions. The fact that they are reported to and maintained by the HKTR does not of itself confer any legally binding effect on such transactions.

Russia's BCS Puts US Stock CFDs in Main App as Group Deepens Retail Push

Featured Videos

FM Daily Brief - 24 April 2026

FM Daily Brief - 24 April 2026

FM Daily Brief - 24 April 2026

FM Daily Brief - 24 April 2026

It's Friday, the twenty-fourth of April 2026. You're listening to the Finance Magnates Daily Brief. Today's lead: Finance Magnates can exclusively report on ACCM's all-time Q1 volume record. Also ahead: the FCA's first coordinated crypto raids in the UK, and a major US day trading rule change. Listen to the full episode...

It's Friday, the twenty-fourth of April 2026. You're listening to the Finance Magnates Daily Brief. Today's lead: Finance Magnates can exclusively report on ACCM's all-time Q1 volume record. Also ahead: the FCA's first coordinated crypto raids in the UK, and a major US day trading rule change. Listen to the full episode...

It's Friday, the twenty-fourth of April 2026. You're listening to the Finance Magnates Daily Brief. Today's lead: Finance Magnates can exclusively report on ACCM's all-time Q1 volume record. Also ahead: the FCA's first coordinated crypto raids in the UK, and a major US day trading rule change. Listen to the full episode...

It's Friday, the twenty-fourth of April 2026. You're listening to the Finance Magnates Daily Brief. Today's lead: Finance Magnates can exclusively report on ACCM's all-time Q1 volume record. Also ahead: the FCA's first coordinated crypto raids in the UK, and a major US day trading rule change. Listen to the full episode...

It's Wednesday, the twenty-third of April 2026. You're listening to the Finance Magnates Daily Brief. Broker results first today: NAGA posts its first profitable quarter, and Hantec's Q1 volume hits one-point-two trillion. Also ahead: prop firm payout data and a three-hundred-million-dollar exchange deal.

Sponsored by FM Academy

It's Wednesday, the twenty-third of April 2026. You're listening to the Finance Magnates Daily Brief. Broker results first today: NAGA posts its first profitable quarter, and Hantec's Q1 volume hits one-point-two trillion. Also ahead: prop firm payout data and a three-hundred-million-dollar exchange deal.

Sponsored by FM Academy

It's Wednesday, the twenty-third of April 2026. You're listening to the Finance Magnates Daily Brief. Broker results first today: NAGA posts its first profitable quarter, and Hantec's Q1 volume hits one-point-two trillion. Also ahead: prop firm payout data and a three-hundred-million-dollar exchange deal.

Sponsored by FM Academy

It's Wednesday, the twenty-third of April 2026. You're listening to the Finance Magnates Daily Brief. Broker results first today: NAGA posts its first profitable quarter, and Hantec's Q1 volume hits one-point-two trillion. Also ahead: prop firm payout data and a three-hundred-million-dollar exchange deal.

Sponsored by FM Academy

It's Wednesday, the twenty-third of April 2026. You're listening to the Finance Magnates Daily Brief. Broker results first today: NAGA posts its first profitable quarter, and Hantec's Q1 volume hits one-point-two trillion. Also ahead: prop firm payout data and a three-hundred-million-dollar exchange deal.

Sponsored by FM Academy

It's Wednesday, the twenty-third of April 2026. You're listening to the Finance Magnates Daily Brief. Broker results first today: NAGA posts its first profitable quarter, and Hantec's Q1 volume hits one-point-two trillion. Also ahead: prop firm payout data and a three-hundred-million-dollar exchange deal.

Sponsored by FM Academy

FM Daily Brief: 21 April 2026

FM Daily Brief: 21 April 2026

FM Daily Brief: 21 April 2026

FM Daily Brief: 21 April 2026

FM Daily Brief: 21 April 2026

FM Daily Brief: 21 April 2026

It's Tuesday, the twenty-first of April, twenty twenty-six. You're listening to the Finance Magnates Daily Brief. Today's lead: the Bank for International Settlements has put dollar stablecoins on the regulatory hot seat. Also ahead: first quarter earnings from Capital.com and Plus500, Revolut pushes its IPO to twenty twenty-eight, and a look at where Singapore hedge funds are really moving.

It's Tuesday, the twenty-first of April, twenty twenty-six. You're listening to the Finance Magnates Daily Brief. Today's lead: the Bank for International Settlements has put dollar stablecoins on the regulatory hot seat. Also ahead: first quarter earnings from Capital.com and Plus500, Revolut pushes its IPO to twenty twenty-eight, and a look at where Singapore hedge funds are really moving.

It's Tuesday, the twenty-first of April, twenty twenty-six. You're listening to the Finance Magnates Daily Brief. Today's lead: the Bank for International Settlements has put dollar stablecoins on the regulatory hot seat. Also ahead: first quarter earnings from Capital.com and Plus500, Revolut pushes its IPO to twenty twenty-eight, and a look at where Singapore hedge funds are really moving.

It's Tuesday, the twenty-first of April, twenty twenty-six. You're listening to the Finance Magnates Daily Brief. Today's lead: the Bank for International Settlements has put dollar stablecoins on the regulatory hot seat. Also ahead: first quarter earnings from Capital.com and Plus500, Revolut pushes its IPO to twenty twenty-eight, and a look at where Singapore hedge funds are really moving.

It's Tuesday, the twenty-first of April, twenty twenty-six. You're listening to the Finance Magnates Daily Brief. Today's lead: the Bank for International Settlements has put dollar stablecoins on the regulatory hot seat. Also ahead: first quarter earnings from Capital.com and Plus500, Revolut pushes its IPO to twenty twenty-eight, and a look at where Singapore hedge funds are really moving.

It's Tuesday, the twenty-first of April, twenty twenty-six. You're listening to the Finance Magnates Daily Brief. Today's lead: the Bank for International Settlements has put dollar stablecoins on the regulatory hot seat. Also ahead: first quarter earnings from Capital.com and Plus500, Revolut pushes its IPO to twenty twenty-eight, and a look at where Singapore hedge funds are really moving.

In this video, we review @FundedNext a proprietary trading firm offering evaluation challenges for CFD and futures traders using simulated accounts.

We cover how the model works, including challenge types, profit targets, loss limits, and performance-based rewards. You’ll also learn about payout structures, supported platforms, and key features such as the firm’s 24-hour payout policy and flexible challenge formats.

Watch the full video to see if FundedNext fits your trading approach.

#FundedNext #PropFirm #PropTrading #FinanceMagnates #Trading #CFDTrading #FuturesTrading #TradingReview

In this video, we review @FundedNext a proprietary trading firm offering evaluation challenges for CFD and futures traders using simulated accounts.

We cover how the model works, including challenge types, profit targets, loss limits, and performance-based rewards. You’ll also learn about payout structures, supported platforms, and key features such as the firm’s 24-hour payout policy and flexible challenge formats.

Watch the full video to see if FundedNext fits your trading approach.

#FundedNext #PropFirm #PropTrading #FinanceMagnates #Trading #CFDTrading #FuturesTrading #TradingReview

In this video, we review @FundedNext a proprietary trading firm offering evaluation challenges for CFD and futures traders using simulated accounts.

We cover how the model works, including challenge types, profit targets, loss limits, and performance-based rewards. You’ll also learn about payout structures, supported platforms, and key features such as the firm’s 24-hour payout policy and flexible challenge formats.

Watch the full video to see if FundedNext fits your trading approach.

#FundedNext #PropFirm #PropTrading #FinanceMagnates #Trading #CFDTrading #FuturesTrading #TradingReview

In this video, we review @FundedNext a proprietary trading firm offering evaluation challenges for CFD and futures traders using simulated accounts.

We cover how the model works, including challenge types, profit targets, loss limits, and performance-based rewards. You’ll also learn about payout structures, supported platforms, and key features such as the firm’s 24-hour payout policy and flexible challenge formats.

Watch the full video to see if FundedNext fits your trading approach.

#FundedNext #PropFirm #PropTrading #FinanceMagnates #Trading #CFDTrading #FuturesTrading #TradingReview

In this video, we review @FundedNext a proprietary trading firm offering evaluation challenges for CFD and futures traders using simulated accounts.

We cover how the model works, including challenge types, profit targets, loss limits, and performance-based rewards. You’ll also learn about payout structures, supported platforms, and key features such as the firm’s 24-hour payout policy and flexible challenge formats.

Watch the full video to see if FundedNext fits your trading approach.

#FundedNext #PropFirm #PropTrading #FinanceMagnates #Trading #CFDTrading #FuturesTrading #TradingReview

In this video, we review @FundedNext a proprietary trading firm offering evaluation challenges for CFD and futures traders using simulated accounts.

We cover how the model works, including challenge types, profit targets, loss limits, and performance-based rewards. You’ll also learn about payout structures, supported platforms, and key features such as the firm’s 24-hour payout policy and flexible challenge formats.

Watch the full video to see if FundedNext fits your trading approach.

#FundedNext #PropFirm #PropTrading #FinanceMagnates #Trading #CFDTrading #FuturesTrading #TradingReview

TradingPro Winner Spotlight 🏆 | Global Best Overall Broker 2025

TradingPro Winner Spotlight 🏆 | Global Best Overall Broker 2025

TradingPro Winner Spotlight 🏆 | Global Best Overall Broker 2025

TradingPro Winner Spotlight 🏆 | Global Best Overall Broker 2025

TradingPro Winner Spotlight 🏆 | Global Best Overall Broker 2025

TradingPro Winner Spotlight 🏆 | Global Best Overall Broker 2025

TradingPro takes the spotlight as Global Best Overall Broker 2025 at the Finance Magnates Awards.

Yusna Yusman, Head of Global Marketing, describes the night as inspiring, elegant, and full of energy.

She also shares a message of appreciation to the clients and community whose support made this achievement possible.

👉 Be part of FM Awards 2026.

#FinanceMagnatesAwards #TradingPro #Trading #Fintech #Broker #WinnerSpotlight #Shorts

TradingPro takes the spotlight as Global Best Overall Broker 2025 at the Finance Magnates Awards.

Yusna Yusman, Head of Global Marketing, describes the night as inspiring, elegant, and full of energy.

She also shares a message of appreciation to the clients and community whose support made this achievement possible.

👉 Be part of FM Awards 2026.

#FinanceMagnatesAwards #TradingPro #Trading #Fintech #Broker #WinnerSpotlight #Shorts

TradingPro takes the spotlight as Global Best Overall Broker 2025 at the Finance Magnates Awards.

Yusna Yusman, Head of Global Marketing, describes the night as inspiring, elegant, and full of energy.

She also shares a message of appreciation to the clients and community whose support made this achievement possible.

👉 Be part of FM Awards 2026.

#FinanceMagnatesAwards #TradingPro #Trading #Fintech #Broker #WinnerSpotlight #Shorts

TradingPro takes the spotlight as Global Best Overall Broker 2025 at the Finance Magnates Awards.

Yusna Yusman, Head of Global Marketing, describes the night as inspiring, elegant, and full of energy.

She also shares a message of appreciation to the clients and community whose support made this achievement possible.

👉 Be part of FM Awards 2026.

#FinanceMagnatesAwards #TradingPro #Trading #Fintech #Broker #WinnerSpotlight #Shorts

TradingPro takes the spotlight as Global Best Overall Broker 2025 at the Finance Magnates Awards.

Yusna Yusman, Head of Global Marketing, describes the night as inspiring, elegant, and full of energy.

She also shares a message of appreciation to the clients and community whose support made this achievement possible.

👉 Be part of FM Awards 2026.

#FinanceMagnatesAwards #TradingPro #Trading #Fintech #Broker #WinnerSpotlight #Shorts

TradingPro takes the spotlight as Global Best Overall Broker 2025 at the Finance Magnates Awards.

Yusna Yusman, Head of Global Marketing, describes the night as inspiring, elegant, and full of energy.

She also shares a message of appreciation to the clients and community whose support made this achievement possible.

👉 Be part of FM Awards 2026.

#FinanceMagnatesAwards #TradingPro #Trading #Fintech #Broker #WinnerSpotlight #Shorts