The BoJ has nearly $1.25 Trillion USD worth of reserves which it may be considering to allocate a portion of to the local FX Industry in an effort to outsource some of its monetary policy efforts.

The timing may be convenient for both the Bank of Japan (BOJ) and the local private FX sector, the latter of which may be considered to manage a portion of the central bank's currency reserves, according to reports from a Japanese government source as told to Reuters.

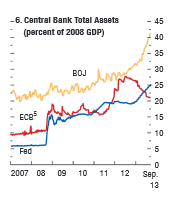

According to a recent report, the International Monetary Fund (IMF) estimates the the BOJ reserves to the tune of $1.25 trillion dollars (as of September 2013). Figure 6 above, excerpted from the World Economic Outlook (WEO) depicts the BOJ's rising assets in comparison with the ECB and US Fed since 2007.

As per reports to the media, Tohru Sasaki, head of Japanese rates and FX research at JP Morgan Tokyo, told clients in a note: "Although we do not think the Japanese government will outsource all of the foreign exchange reserve to the private sector, even just a 10 percent outsourcing will become a $120 billion business."

Timely Opportunities or Coincidence

The Japanese Financial Services Authority (JFSA) website currently lists 2,112 companies with licenses as financial instrument firms, 64 regional banks, 16 bank holding companies and 35 bank trusts, among other financial services categories. Which, if any, could be the recipient of such honor to manage a portion of BOJ's reserves is still a matter of speculation.

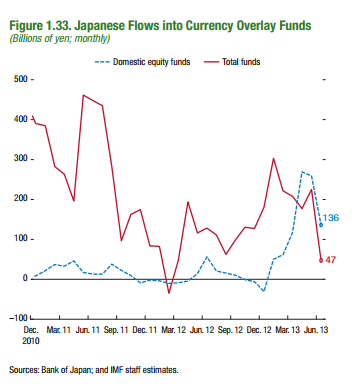

The Bank of Japan is the "central" bank of Japan, and is tasked with the common role shared by central banks globally to carry out a specific monetary policy aimed at balancing the ebbs and flows of the economy, in accordance with its needs for long- term sustainable growth or manageability. The recent flows into Currency overlay funds, as displayed in figure 1.33, has been decreasing.

According to the latest quarterly review (September) from the Bank for International Settlements (BIS), Japanese banks have recently become once again, the biggest suppliers of cross-border bank credit, a trend that has been years in the making. The BIS consolidated banking statistics show that in 2011 Japanese banks replaced German banks as the world’s largest international lenders. On a consolidated basis, US banks were the next largest cross-border lenders, with a market share of about 12% at end-March 2013, followed by German banks at 11%. This marks a return of Japanese banks to the position they held in the international banking market during the second half of the 1980's, according to the BIS report.

The World Economic Outlook (WEO) forecasts real GDP in Japan to be 1.2% in 2014 - largely due to a tightening fiscal policy - down from the 2% forecast for 2013. According to the IMF, Asia is likely to remain the world’s economic engine despite the recent soft patch in global growth and increasing volatility in international financial markets.

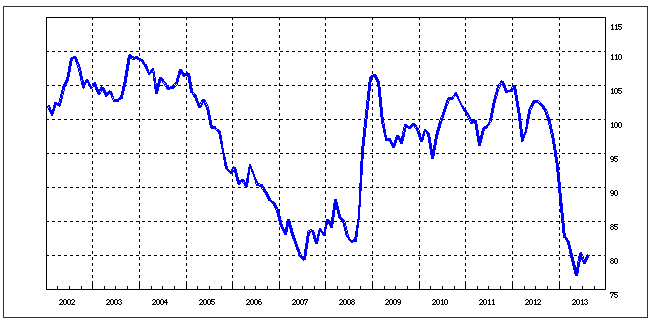

USD JPY exchange rate averaged monthly - source BoJ

Abeonomic Views

Over this past weekend, Haruhiko Kuroda, the Governor of the BOJ, commented at the Institute of International Finance (IIF) during its annual membership meeting in Washington saying, "Positive developments in the Japanese economy have become increasingly pronounced, and the outlook is perhaps brighter than at any other point since the turn of the century."

Mr. Kuroda pointed out at the BOJ's introduction of Quantitative and Qualitative Easing (QQE) in April, saying, "Regulators and supervisors must be humble about the usefulness and effectiveness of regulatory standards and rules. Risk-based capital standards should remain at the center, but other approaches must complement them in areas where capital charges cannot adequately address problematic behavior among banks. Though I do not have time to elaborate, tough and effective supervision is also very, very important. The simple leverage ratio may be a good metric in some respects, and is a useful complement to risk-based capital ratios."

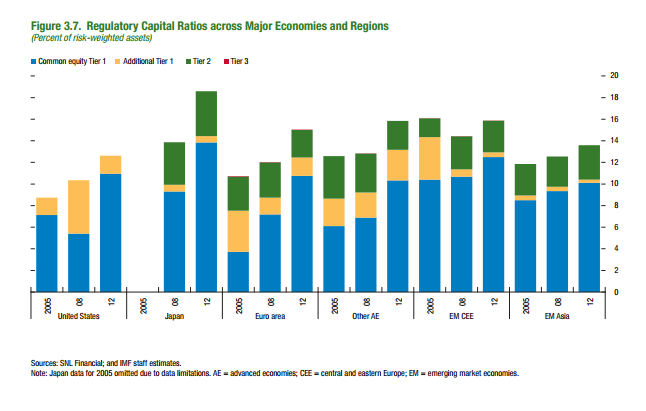

While the Governor praised and welcomed Basel III, he followed with a detailed critique expressing how other major economies have not caught up yet (due to delays), while Japan and many other economies are in full force with the new capital standard. With regards to the global regulatory approach, he compared the progress to "patching up leaks in a roof," and that the next steps are crucial. Figure 3.7 below shows how Japan stands out with regards to its high regulatory capital ratios in 2012, in comparison to other major economies in recent years.

Lessons Already Learned

The BOJ's Governor concluded that there needs to be a degree of harmonized standardization of regulations across borders, and how Japan should implement swift and fast responses reflecting the lessons learned from the Great Financial Crisis.He said that the BOJ was ready to contribute to improve the rules and standards surrounding domestic regulations, and how they tie into the global landscape.

The most recent financial statement from the BOJ for its latest fiscal year reflected net assets of nearly 164.8 trillion yen, and net assets of 3.2 trillion yen after liabilities. After gross operating profits of 1.13 trillion yen, 836 billion yen was attributed to net profits and 301 billion to a special loss listed as a transfer to provision for possible losses on foreign exchange transactions. After taxes, reserve deduction and dividend, a net income of 547 billion yen was appropriated back to the Government.

According to the WEO, the recovery in Japan has been spurred by Abenomics, but sustaining it will depend on meeting two major challenges. The first, reflected in the debate about increasing the consumption tax, is setting the right pace for fiscal consolidation; too slowly will compromise credibility, and moving too fast will kill growth. The second is implementing a credible set of structural reforms to transform what is now a cyclical recovery into sustained growth. Taro Aso, the Deputy Prime Minister of Japan also spoke over the weekend regarding revitalizing Japan's economy, at the International Monetary and Financial Committee during its 28th meeting on October 12, 2013 where he serves as Governor to the IMF for Japan.

The timing may be convenient for both the Bank of Japan (BOJ) and the local private FX sector, the latter of which may be considered to manage a portion of the central bank's currency reserves, according to reports from a Japanese government source as told to Reuters.

According to a recent report, the International Monetary Fund (IMF) estimates the the BOJ reserves to the tune of $1.25 trillion dollars (as of September 2013). Figure 6 above, excerpted from the World Economic Outlook (WEO) depicts the BOJ's rising assets in comparison with the ECB and US Fed since 2007.

As per reports to the media, Tohru Sasaki, head of Japanese rates and FX research at JP Morgan Tokyo, told clients in a note: "Although we do not think the Japanese government will outsource all of the foreign exchange reserve to the private sector, even just a 10 percent outsourcing will become a $120 billion business."

Timely Opportunities or Coincidence

The Japanese Financial Services Authority (JFSA) website currently lists 2,112 companies with licenses as financial instrument firms, 64 regional banks, 16 bank holding companies and 35 bank trusts, among other financial services categories. Which, if any, could be the recipient of such honor to manage a portion of BOJ's reserves is still a matter of speculation.

The Bank of Japan is the "central" bank of Japan, and is tasked with the common role shared by central banks globally to carry out a specific monetary policy aimed at balancing the ebbs and flows of the economy, in accordance with its needs for long- term sustainable growth or manageability. The recent flows into Currency overlay funds, as displayed in figure 1.33, has been decreasing.

According to the latest quarterly review (September) from the Bank for International Settlements (BIS), Japanese banks have recently become once again, the biggest suppliers of cross-border bank credit, a trend that has been years in the making. The BIS consolidated banking statistics show that in 2011 Japanese banks replaced German banks as the world’s largest international lenders. On a consolidated basis, US banks were the next largest cross-border lenders, with a market share of about 12% at end-March 2013, followed by German banks at 11%. This marks a return of Japanese banks to the position they held in the international banking market during the second half of the 1980's, according to the BIS report.

The World Economic Outlook (WEO) forecasts real GDP in Japan to be 1.2% in 2014 - largely due to a tightening fiscal policy - down from the 2% forecast for 2013. According to the IMF, Asia is likely to remain the world’s economic engine despite the recent soft patch in global growth and increasing volatility in international financial markets.

USD JPY exchange rate averaged monthly - source BoJ

Abeonomic Views

Over this past weekend, Haruhiko Kuroda, the Governor of the BOJ, commented at the Institute of International Finance (IIF) during its annual membership meeting in Washington saying, "Positive developments in the Japanese economy have become increasingly pronounced, and the outlook is perhaps brighter than at any other point since the turn of the century."

Mr. Kuroda pointed out at the BOJ's introduction of Quantitative and Qualitative Easing (QQE) in April, saying, "Regulators and supervisors must be humble about the usefulness and effectiveness of regulatory standards and rules. Risk-based capital standards should remain at the center, but other approaches must complement them in areas where capital charges cannot adequately address problematic behavior among banks. Though I do not have time to elaborate, tough and effective supervision is also very, very important. The simple leverage ratio may be a good metric in some respects, and is a useful complement to risk-based capital ratios."

While the Governor praised and welcomed Basel III, he followed with a detailed critique expressing how other major economies have not caught up yet (due to delays), while Japan and many other economies are in full force with the new capital standard. With regards to the global regulatory approach, he compared the progress to "patching up leaks in a roof," and that the next steps are crucial. Figure 3.7 below shows how Japan stands out with regards to its high regulatory capital ratios in 2012, in comparison to other major economies in recent years.

Lessons Already Learned

The BOJ's Governor concluded that there needs to be a degree of harmonized standardization of regulations across borders, and how Japan should implement swift and fast responses reflecting the lessons learned from the Great Financial Crisis.He said that the BOJ was ready to contribute to improve the rules and standards surrounding domestic regulations, and how they tie into the global landscape.

The most recent financial statement from the BOJ for its latest fiscal year reflected net assets of nearly 164.8 trillion yen, and net assets of 3.2 trillion yen after liabilities. After gross operating profits of 1.13 trillion yen, 836 billion yen was attributed to net profits and 301 billion to a special loss listed as a transfer to provision for possible losses on foreign exchange transactions. After taxes, reserve deduction and dividend, a net income of 547 billion yen was appropriated back to the Government.

According to the WEO, the recovery in Japan has been spurred by Abenomics, but sustaining it will depend on meeting two major challenges. The first, reflected in the debate about increasing the consumption tax, is setting the right pace for fiscal consolidation; too slowly will compromise credibility, and moving too fast will kill growth. The second is implementing a credible set of structural reforms to transform what is now a cyclical recovery into sustained growth. Taro Aso, the Deputy Prime Minister of Japan also spoke over the weekend regarding revitalizing Japan's economy, at the International Monetary and Financial Committee during its 28th meeting on October 12, 2013 where he serves as Governor to the IMF for Japan.

Russia's BCS Puts US Stock CFDs in Main App as Group Deepens Retail Push

Featured Videos

FM Daily Brief - 24 April 2026

FM Daily Brief - 24 April 2026

FM Daily Brief - 24 April 2026

FM Daily Brief - 24 April 2026

It's Friday, the twenty-fourth of April 2026. You're listening to the Finance Magnates Daily Brief. Today's lead: Finance Magnates can exclusively report on ACCM's all-time Q1 volume record. Also ahead: the FCA's first coordinated crypto raids in the UK, and a major US day trading rule change. Listen to the full episode...

It's Friday, the twenty-fourth of April 2026. You're listening to the Finance Magnates Daily Brief. Today's lead: Finance Magnates can exclusively report on ACCM's all-time Q1 volume record. Also ahead: the FCA's first coordinated crypto raids in the UK, and a major US day trading rule change. Listen to the full episode...

It's Friday, the twenty-fourth of April 2026. You're listening to the Finance Magnates Daily Brief. Today's lead: Finance Magnates can exclusively report on ACCM's all-time Q1 volume record. Also ahead: the FCA's first coordinated crypto raids in the UK, and a major US day trading rule change. Listen to the full episode...

It's Friday, the twenty-fourth of April 2026. You're listening to the Finance Magnates Daily Brief. Today's lead: Finance Magnates can exclusively report on ACCM's all-time Q1 volume record. Also ahead: the FCA's first coordinated crypto raids in the UK, and a major US day trading rule change. Listen to the full episode...

It's Wednesday, the twenty-third of April 2026. You're listening to the Finance Magnates Daily Brief. Broker results first today: NAGA posts its first profitable quarter, and Hantec's Q1 volume hits one-point-two trillion. Also ahead: prop firm payout data and a three-hundred-million-dollar exchange deal.

Sponsored by FM Academy

It's Wednesday, the twenty-third of April 2026. You're listening to the Finance Magnates Daily Brief. Broker results first today: NAGA posts its first profitable quarter, and Hantec's Q1 volume hits one-point-two trillion. Also ahead: prop firm payout data and a three-hundred-million-dollar exchange deal.

Sponsored by FM Academy

It's Wednesday, the twenty-third of April 2026. You're listening to the Finance Magnates Daily Brief. Broker results first today: NAGA posts its first profitable quarter, and Hantec's Q1 volume hits one-point-two trillion. Also ahead: prop firm payout data and a three-hundred-million-dollar exchange deal.

Sponsored by FM Academy

It's Wednesday, the twenty-third of April 2026. You're listening to the Finance Magnates Daily Brief. Broker results first today: NAGA posts its first profitable quarter, and Hantec's Q1 volume hits one-point-two trillion. Also ahead: prop firm payout data and a three-hundred-million-dollar exchange deal.

Sponsored by FM Academy

It's Wednesday, the twenty-third of April 2026. You're listening to the Finance Magnates Daily Brief. Broker results first today: NAGA posts its first profitable quarter, and Hantec's Q1 volume hits one-point-two trillion. Also ahead: prop firm payout data and a three-hundred-million-dollar exchange deal.

Sponsored by FM Academy

It's Wednesday, the twenty-third of April 2026. You're listening to the Finance Magnates Daily Brief. Broker results first today: NAGA posts its first profitable quarter, and Hantec's Q1 volume hits one-point-two trillion. Also ahead: prop firm payout data and a three-hundred-million-dollar exchange deal.

Sponsored by FM Academy

FM Daily Brief: 21 April 2026

FM Daily Brief: 21 April 2026

FM Daily Brief: 21 April 2026

FM Daily Brief: 21 April 2026

FM Daily Brief: 21 April 2026

FM Daily Brief: 21 April 2026

It's Tuesday, the twenty-first of April, twenty twenty-six. You're listening to the Finance Magnates Daily Brief. Today's lead: the Bank for International Settlements has put dollar stablecoins on the regulatory hot seat. Also ahead: first quarter earnings from Capital.com and Plus500, Revolut pushes its IPO to twenty twenty-eight, and a look at where Singapore hedge funds are really moving.

It's Tuesday, the twenty-first of April, twenty twenty-six. You're listening to the Finance Magnates Daily Brief. Today's lead: the Bank for International Settlements has put dollar stablecoins on the regulatory hot seat. Also ahead: first quarter earnings from Capital.com and Plus500, Revolut pushes its IPO to twenty twenty-eight, and a look at where Singapore hedge funds are really moving.

It's Tuesday, the twenty-first of April, twenty twenty-six. You're listening to the Finance Magnates Daily Brief. Today's lead: the Bank for International Settlements has put dollar stablecoins on the regulatory hot seat. Also ahead: first quarter earnings from Capital.com and Plus500, Revolut pushes its IPO to twenty twenty-eight, and a look at where Singapore hedge funds are really moving.

It's Tuesday, the twenty-first of April, twenty twenty-six. You're listening to the Finance Magnates Daily Brief. Today's lead: the Bank for International Settlements has put dollar stablecoins on the regulatory hot seat. Also ahead: first quarter earnings from Capital.com and Plus500, Revolut pushes its IPO to twenty twenty-eight, and a look at where Singapore hedge funds are really moving.

It's Tuesday, the twenty-first of April, twenty twenty-six. You're listening to the Finance Magnates Daily Brief. Today's lead: the Bank for International Settlements has put dollar stablecoins on the regulatory hot seat. Also ahead: first quarter earnings from Capital.com and Plus500, Revolut pushes its IPO to twenty twenty-eight, and a look at where Singapore hedge funds are really moving.

It's Tuesday, the twenty-first of April, twenty twenty-six. You're listening to the Finance Magnates Daily Brief. Today's lead: the Bank for International Settlements has put dollar stablecoins on the regulatory hot seat. Also ahead: first quarter earnings from Capital.com and Plus500, Revolut pushes its IPO to twenty twenty-eight, and a look at where Singapore hedge funds are really moving.

In this video, we review @FundedNext a proprietary trading firm offering evaluation challenges for CFD and futures traders using simulated accounts.

We cover how the model works, including challenge types, profit targets, loss limits, and performance-based rewards. You’ll also learn about payout structures, supported platforms, and key features such as the firm’s 24-hour payout policy and flexible challenge formats.

Watch the full video to see if FundedNext fits your trading approach.

#FundedNext #PropFirm #PropTrading #FinanceMagnates #Trading #CFDTrading #FuturesTrading #TradingReview

In this video, we review @FundedNext a proprietary trading firm offering evaluation challenges for CFD and futures traders using simulated accounts.

We cover how the model works, including challenge types, profit targets, loss limits, and performance-based rewards. You’ll also learn about payout structures, supported platforms, and key features such as the firm’s 24-hour payout policy and flexible challenge formats.

Watch the full video to see if FundedNext fits your trading approach.

#FundedNext #PropFirm #PropTrading #FinanceMagnates #Trading #CFDTrading #FuturesTrading #TradingReview

In this video, we review @FundedNext a proprietary trading firm offering evaluation challenges for CFD and futures traders using simulated accounts.

We cover how the model works, including challenge types, profit targets, loss limits, and performance-based rewards. You’ll also learn about payout structures, supported platforms, and key features such as the firm’s 24-hour payout policy and flexible challenge formats.

Watch the full video to see if FundedNext fits your trading approach.

#FundedNext #PropFirm #PropTrading #FinanceMagnates #Trading #CFDTrading #FuturesTrading #TradingReview

In this video, we review @FundedNext a proprietary trading firm offering evaluation challenges for CFD and futures traders using simulated accounts.

We cover how the model works, including challenge types, profit targets, loss limits, and performance-based rewards. You’ll also learn about payout structures, supported platforms, and key features such as the firm’s 24-hour payout policy and flexible challenge formats.

Watch the full video to see if FundedNext fits your trading approach.

#FundedNext #PropFirm #PropTrading #FinanceMagnates #Trading #CFDTrading #FuturesTrading #TradingReview

In this video, we review @FundedNext a proprietary trading firm offering evaluation challenges for CFD and futures traders using simulated accounts.

We cover how the model works, including challenge types, profit targets, loss limits, and performance-based rewards. You’ll also learn about payout structures, supported platforms, and key features such as the firm’s 24-hour payout policy and flexible challenge formats.

Watch the full video to see if FundedNext fits your trading approach.

#FundedNext #PropFirm #PropTrading #FinanceMagnates #Trading #CFDTrading #FuturesTrading #TradingReview

In this video, we review @FundedNext a proprietary trading firm offering evaluation challenges for CFD and futures traders using simulated accounts.

We cover how the model works, including challenge types, profit targets, loss limits, and performance-based rewards. You’ll also learn about payout structures, supported platforms, and key features such as the firm’s 24-hour payout policy and flexible challenge formats.

Watch the full video to see if FundedNext fits your trading approach.

#FundedNext #PropFirm #PropTrading #FinanceMagnates #Trading #CFDTrading #FuturesTrading #TradingReview

TradingPro Winner Spotlight 🏆 | Global Best Overall Broker 2025

TradingPro Winner Spotlight 🏆 | Global Best Overall Broker 2025

TradingPro Winner Spotlight 🏆 | Global Best Overall Broker 2025

TradingPro Winner Spotlight 🏆 | Global Best Overall Broker 2025

TradingPro Winner Spotlight 🏆 | Global Best Overall Broker 2025

TradingPro Winner Spotlight 🏆 | Global Best Overall Broker 2025

TradingPro takes the spotlight as Global Best Overall Broker 2025 at the Finance Magnates Awards.

Yusna Yusman, Head of Global Marketing, describes the night as inspiring, elegant, and full of energy.

She also shares a message of appreciation to the clients and community whose support made this achievement possible.

👉 Be part of FM Awards 2026.

#FinanceMagnatesAwards #TradingPro #Trading #Fintech #Broker #WinnerSpotlight #Shorts

TradingPro takes the spotlight as Global Best Overall Broker 2025 at the Finance Magnates Awards.

Yusna Yusman, Head of Global Marketing, describes the night as inspiring, elegant, and full of energy.

She also shares a message of appreciation to the clients and community whose support made this achievement possible.

👉 Be part of FM Awards 2026.

#FinanceMagnatesAwards #TradingPro #Trading #Fintech #Broker #WinnerSpotlight #Shorts

TradingPro takes the spotlight as Global Best Overall Broker 2025 at the Finance Magnates Awards.

Yusna Yusman, Head of Global Marketing, describes the night as inspiring, elegant, and full of energy.

She also shares a message of appreciation to the clients and community whose support made this achievement possible.

👉 Be part of FM Awards 2026.

#FinanceMagnatesAwards #TradingPro #Trading #Fintech #Broker #WinnerSpotlight #Shorts

TradingPro takes the spotlight as Global Best Overall Broker 2025 at the Finance Magnates Awards.

Yusna Yusman, Head of Global Marketing, describes the night as inspiring, elegant, and full of energy.

She also shares a message of appreciation to the clients and community whose support made this achievement possible.

👉 Be part of FM Awards 2026.

#FinanceMagnatesAwards #TradingPro #Trading #Fintech #Broker #WinnerSpotlight #Shorts

TradingPro takes the spotlight as Global Best Overall Broker 2025 at the Finance Magnates Awards.

Yusna Yusman, Head of Global Marketing, describes the night as inspiring, elegant, and full of energy.

She also shares a message of appreciation to the clients and community whose support made this achievement possible.

👉 Be part of FM Awards 2026.

#FinanceMagnatesAwards #TradingPro #Trading #Fintech #Broker #WinnerSpotlight #Shorts

TradingPro takes the spotlight as Global Best Overall Broker 2025 at the Finance Magnates Awards.

Yusna Yusman, Head of Global Marketing, describes the night as inspiring, elegant, and full of energy.

She also shares a message of appreciation to the clients and community whose support made this achievement possible.

👉 Be part of FM Awards 2026.

#FinanceMagnatesAwards #TradingPro #Trading #Fintech #Broker #WinnerSpotlight #Shorts