CFD profits thrive on volatility. A shift to futures could permanently reshape broker earnings.

As EU regulators tighten OTC rules, brokers are rethinking how sustainable their revenue model really is.

CFD model profits vs. Futures & Options model profits

European CFD brokers are accelerating plans to add futures and options to their platforms. According to a recent Acuiti survey conducted for CME Group, four out of five firms that do not yet offer listed derivatives are either planning to or actively considering doing so.

What looks like product expansion is in fact a structural pivot. Moving from OTC CFDs to exchange-traded futures and options fundamentally changes how brokers generate revenues and what risks they are exposed to.

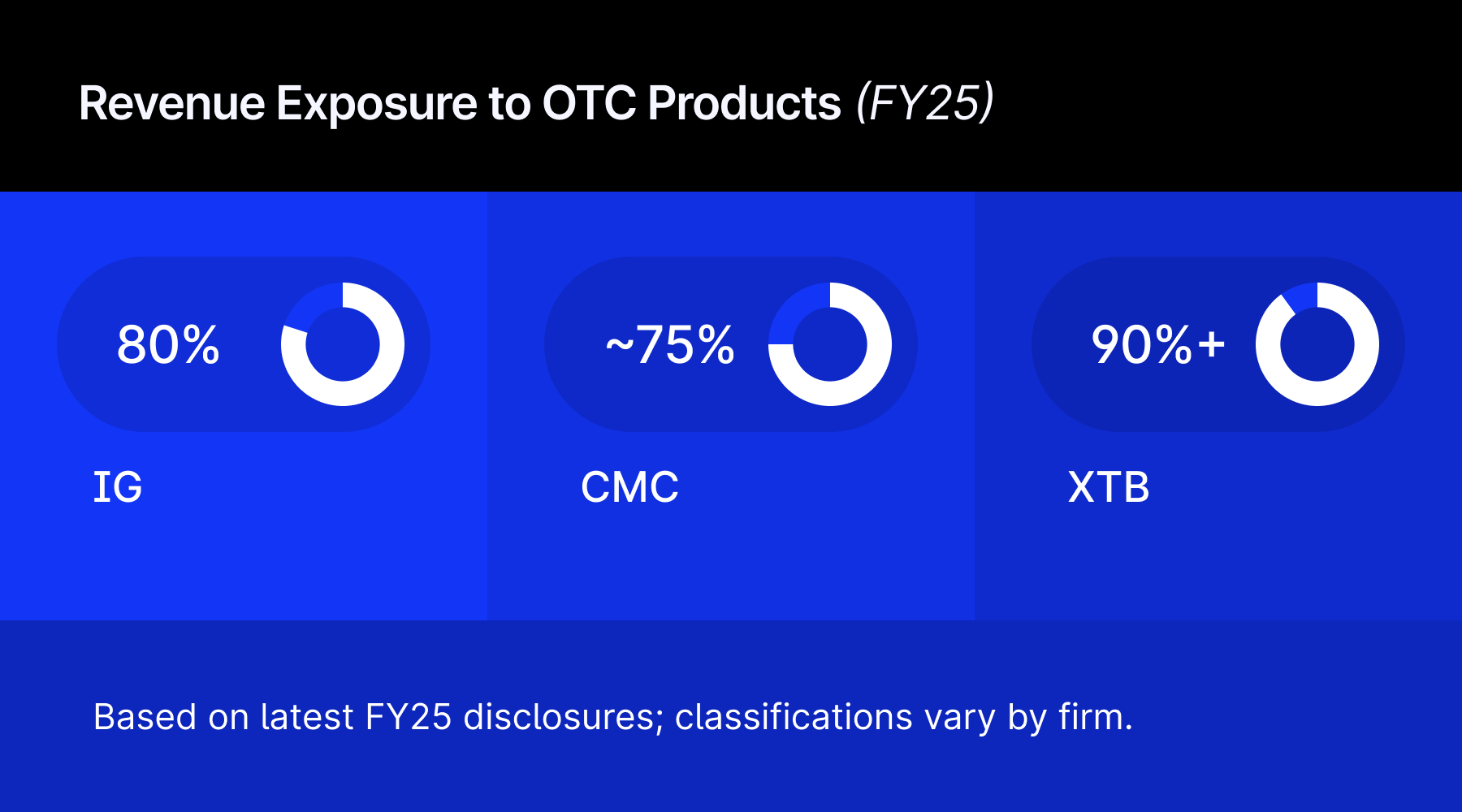

Public disclosures from major European retail brokers underline how heavily earnings remain concentrated in OTC and leveraged products.

In FY25, the majority of net trading income at IG, CMC Markets and XTB was still derived from CFDs and other internalised derivatives.

Swissquote represents a structural outlier. Unlike most CFD-centric peers, the Swiss-listed broker generates the majority of its trading revenues from securities and exchange-traded activity rather than leveraged OTC flow.

CFD brokers revenue exposure to OTC products (FY25)

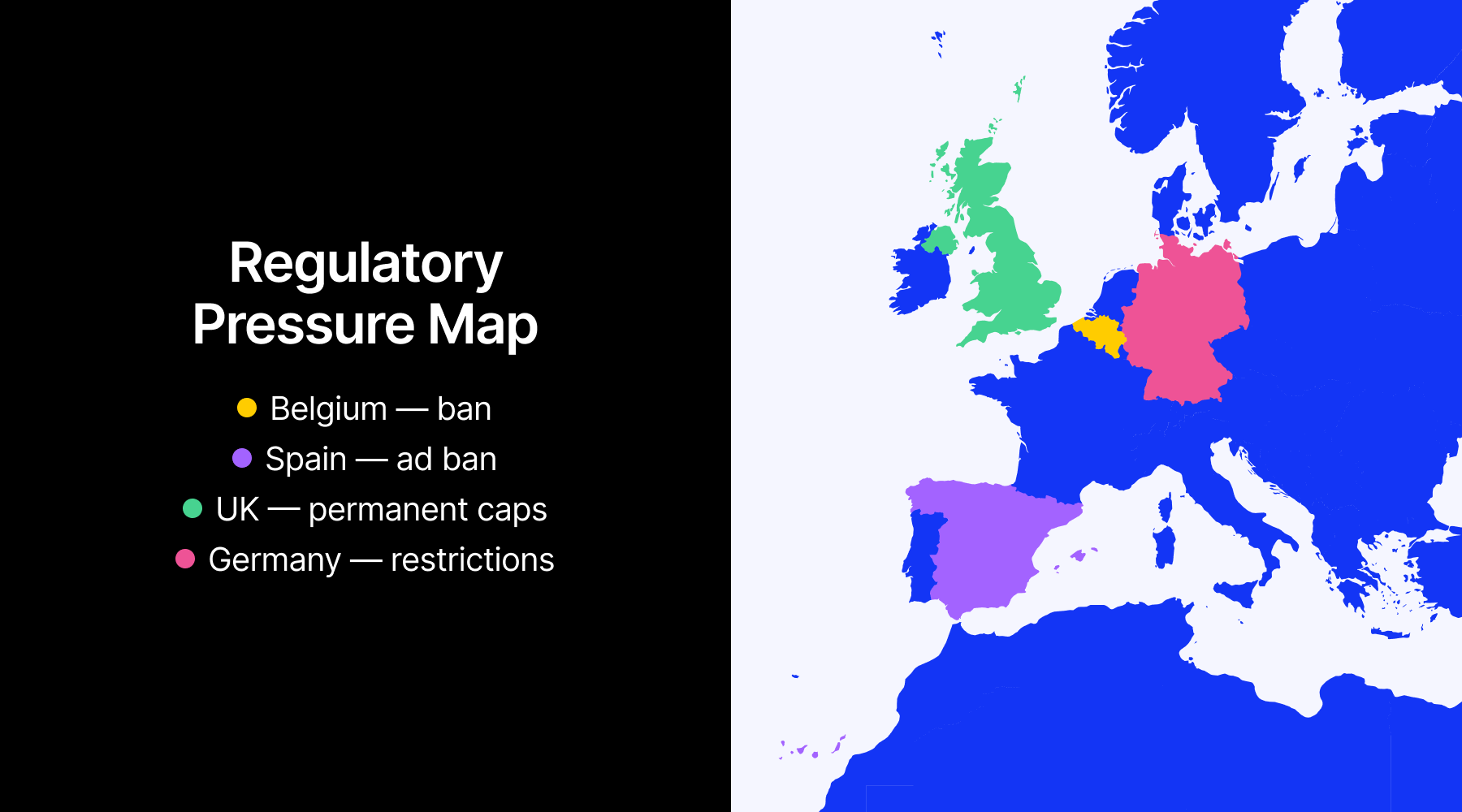

Why are CFD brokers under pressure?

European regulators have moved well beyond leverage caps and warning labels.

Belgium introduced an outright ban on leveraged CFDs and rolling spot FX for retail clients via electronic platforms.

Spain’s CNMV prohibited advertising CFDs to retail investors and tightened leverage and margin rules.

The UK’s FCA made ESMA’s temporary restrictions permanent, locking in leverage caps, strict margin close-out rules and aggressive risk warnings.

Regulators are no longer focused solely on marketing practices; they are questioning the structure of the OTC model itself. Issues such as opaque pricing, high leverage, and the inherent conflict of interest embedded in B-Book models are repeatedly highlighted.

When supervisors point out that the majority of retail CFD accounts lose money, the critique is structural rather than cosmetic.

That anxiety is mirrored inside firms.

In the Acuiti survey, regulatory compliance ranked as the top operational challenge for 89% of brokers offering CFDs, and 62% said they were very concerned about further regulatory tightening.

European regulators take tough stance towards CFD

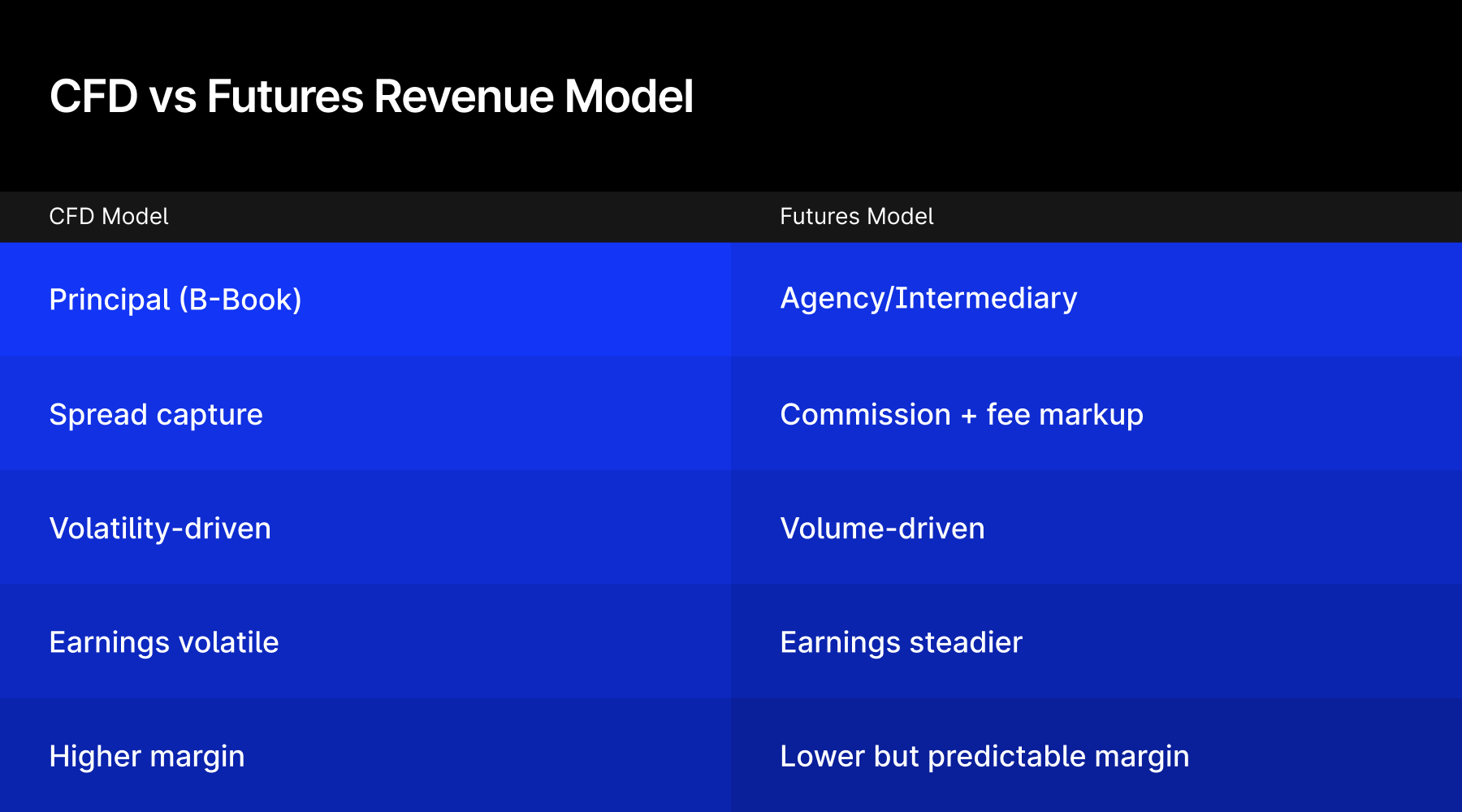

How does a CFD broker actually make money?

The economics of CFDs are closely linked to internalisation and principal risk. In a traditional B-Book setup, the broker is the counterparty to the client. Client losses over time translate into broker profits, subject to hedging costs.

As retail trading behaviour tends to be pro-cyclical and negatively convex, this P&L can be substantial during volatile periods.

Even where brokers hedge selectively, much of the flow is internalised.

Firms capture the bid-ask spread, benefit from asymmetries in execution, and net opposing client positions before deciding whether to hedge externally. Larger brokers typically run hybrid books, dynamically shifting exposure between internal warehousing and external liquidity providers.

This flexibility gives management discretion over how much market risk to carry and when.

The model is highly sensitive to volatility. Spikes in market turbulence increase volumes, widen spreads and accelerate stop-outs, all of which tend to support revenue.

CFDs are therefore structurally high-margin products, precisely because the broker controls pricing and internalisation. That control, however, is exactly what regulators have come to question.

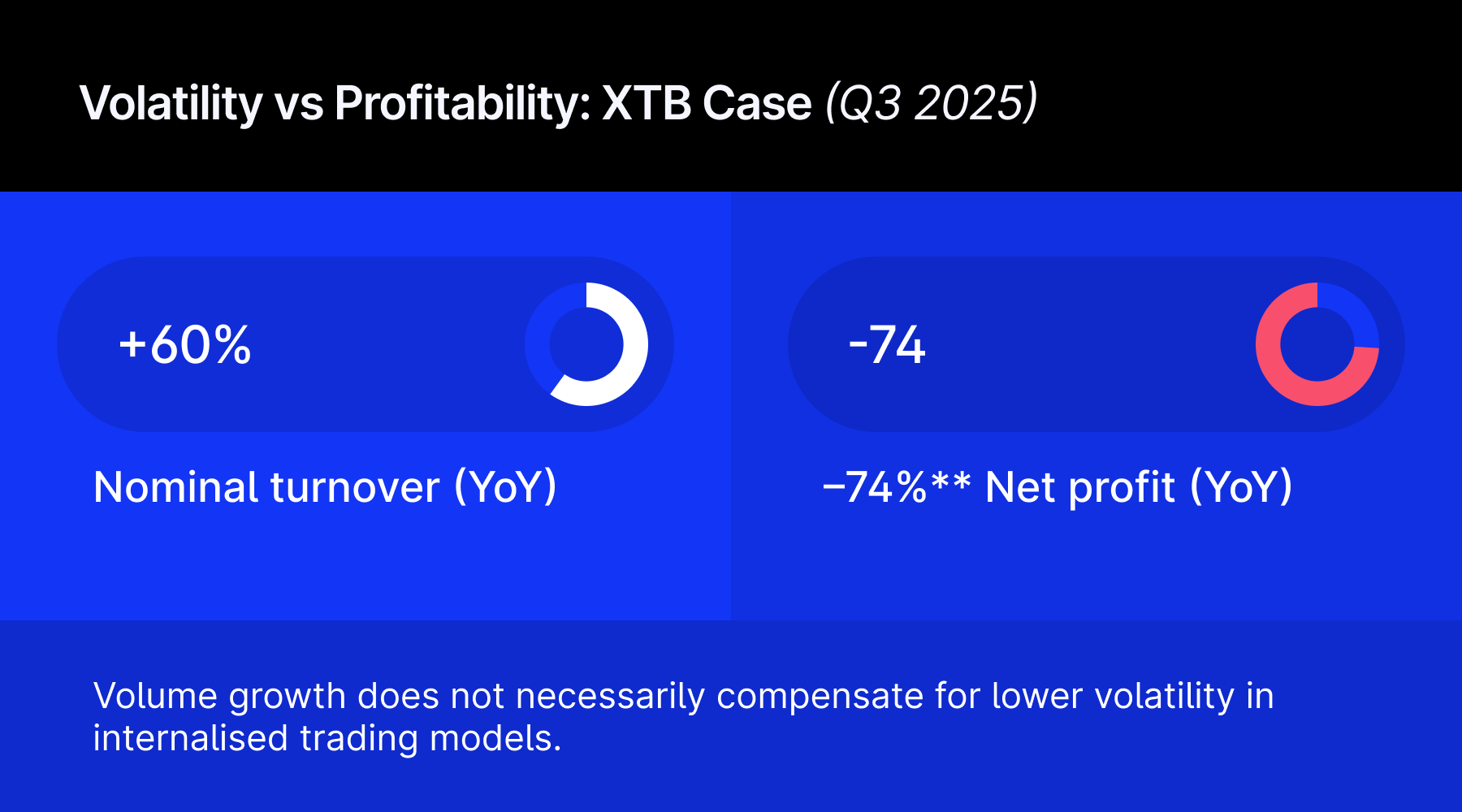

XTB’s third-quarter 2025 results illustrate how sensitive internalised models remain to volatility regimes. Despite a sharp increase in client activity and nominal turnover, lower market volatility reduced profitability per lot, leading to a significant drop in net earnings.

Volatility vs Profitability: XTB Case (Q3 2025)

How is the revenue model different in futures and options?

Listed futures and options fundamentally reframe the broker’s role. Instead of acting as principal, the broker operates primarily as an intermediary connected to an exchange and a clearinghouse.

Revenue is driven mainly by commissions and exchange fee mark-ups rather than by client trading losses.

Margins per contract are typically thinner but more predictable. Brokers do not control spreads in the same way as in OTC products because prices are formed in a central order book,

At the same time, listed derivatives open other revenue channels. Interest on client cash balances, margin financing for active accounts, and paid access to market data or advanced trading tools become increasingly important. The broker’s economics shift from warehousing risk to monetising infrastructure, scale and client engagement.

How is the revenue model different in futures and options

Does that mean revenues will fall?

In the near term, most firms should expect pressure. The reduction of B-Book P&L removes a high-margin, volatility-amplified revenue stream. Replacing it with commission income typically lowers revenue per active client, particularly in the early stages of transition. Competition in listed derivatives is transparent and fee-driven, limiting pricing power.

The medium-term picture, however, is more nuanced. Industry research and broker disclosures suggest that listed derivatives tend to attract a more engaged and better-capitalised segment of retail traders.

A 2025 Acuiti report for CME Group noted that active futures and options traders are more consistent in their activity and more willing to pay for data, analytics and professional tools than mass-market CFD clients.

While per-trade margins are thinner in exchange-traded products, higher engagement and more stable trading patterns can support improved lifetime value over time.

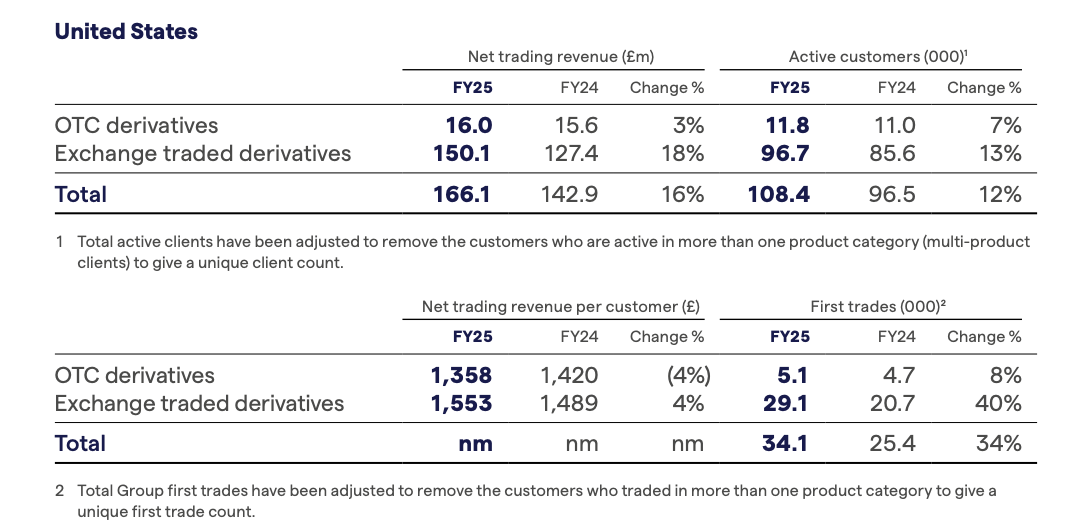

IG’s US division illustrates this divergence. Exchange-traded derivatives revenue grew 21% year-on-year in USD terms, with revenue per customer up 4%, while OTC revenue per customer declined. The data suggests stronger monetisation momentum in listed products relative to principal-based flow.

IG Group's annual repot (2025)

Listed derivatives also reduce regulatory tail risk. Revenue tied to centrally cleared products is less vulnerable to sudden product bans than income derived from high-leverage OTC contracts. That stability becomes increasingly important when firms commit capital to technology, marketing and balance sheet expansion.

For many firms, the shift toward listed derivatives is not purely opportunistic. In markets where high-leverage OTC products face increasing restrictions, futures and options offer a way to preserve a retail derivatives franchise within a more durable regulatory framework.

What is the biggest obstacle?

Technology integration and regulatory permissions are significant, but the primary constraint is client education. For more than a decade, retail traders in Europe were introduced to derivatives primarily through CFDs, which are perpetual, standardised and relatively simple to understand in notional terms.

Futures and options demand a more complex mental framework involving contract multipliers, margin variation, expiries and, in the case of options, volatility and time decay.

Bridging that gap requires sustained investment in structured education, simulation tools and support infrastructure. In the short term, these costs weigh on margins. In the longer term, they determine whether a broker can cultivate a stable, higher-value client base in listed derivatives.

The most plausible outcome is a hybrid model. Where regulation allows, CFDs will remain for smaller tickets and niche exposures, while futures and options anchor core index, rates and commodity trading.

The revenue mix will gradually shift away from principal risk and toward commissions, financing and services.

Margins per trade are likely to compress across the industry, making scale and cross-selling more important.

Smaller, pure-CFD operators may struggle to fund the infrastructure required for listed derivatives and could consolidate or pivot to introducing-broker models.

Larger, well-capitalised firms with multi-jurisdictional licences and strong technology stacks are positioned to capture share.

Over time, the share of group revenue derived from pure B-Book risk-taking is likely to decline.

The transition does not necessarily shrink revenues outright. Instead, it changes their composition and reduces their volatility. Firms that adapt early may end up with lower per-trade margins but more diversified and resilient earnings.

Those that remain heavily dependent on high-leverage OTC flow face an increasingly binary risk profile in a regulatory environment that shows little sign of softening.

European CFD brokers are accelerating plans to add futures and options to their platforms. According to a recent Acuiti survey conducted for CME Group, four out of five firms that do not yet offer listed derivatives are either planning to or actively considering doing so.

What looks like product expansion is in fact a structural pivot. Moving from OTC CFDs to exchange-traded futures and options fundamentally changes how brokers generate revenues and what risks they are exposed to.

Public disclosures from major European retail brokers underline how heavily earnings remain concentrated in OTC and leveraged products.

In FY25, the majority of net trading income at IG, CMC Markets and XTB was still derived from CFDs and other internalised derivatives.

Swissquote represents a structural outlier. Unlike most CFD-centric peers, the Swiss-listed broker generates the majority of its trading revenues from securities and exchange-traded activity rather than leveraged OTC flow.

CFD brokers revenue exposure to OTC products (FY25)

Why are CFD brokers under pressure?

European regulators have moved well beyond leverage caps and warning labels.

Belgium introduced an outright ban on leveraged CFDs and rolling spot FX for retail clients via electronic platforms.

Spain’s CNMV prohibited advertising CFDs to retail investors and tightened leverage and margin rules.

The UK’s FCA made ESMA’s temporary restrictions permanent, locking in leverage caps, strict margin close-out rules and aggressive risk warnings.

Regulators are no longer focused solely on marketing practices; they are questioning the structure of the OTC model itself. Issues such as opaque pricing, high leverage, and the inherent conflict of interest embedded in B-Book models are repeatedly highlighted.

When supervisors point out that the majority of retail CFD accounts lose money, the critique is structural rather than cosmetic.

That anxiety is mirrored inside firms.

In the Acuiti survey, regulatory compliance ranked as the top operational challenge for 89% of brokers offering CFDs, and 62% said they were very concerned about further regulatory tightening.

European regulators take tough stance towards CFD

How does a CFD broker actually make money?

The economics of CFDs are closely linked to internalisation and principal risk. In a traditional B-Book setup, the broker is the counterparty to the client. Client losses over time translate into broker profits, subject to hedging costs.

As retail trading behaviour tends to be pro-cyclical and negatively convex, this P&L can be substantial during volatile periods.

Even where brokers hedge selectively, much of the flow is internalised.

Firms capture the bid-ask spread, benefit from asymmetries in execution, and net opposing client positions before deciding whether to hedge externally. Larger brokers typically run hybrid books, dynamically shifting exposure between internal warehousing and external liquidity providers.

This flexibility gives management discretion over how much market risk to carry and when.

The model is highly sensitive to volatility. Spikes in market turbulence increase volumes, widen spreads and accelerate stop-outs, all of which tend to support revenue.

CFDs are therefore structurally high-margin products, precisely because the broker controls pricing and internalisation. That control, however, is exactly what regulators have come to question.

XTB’s third-quarter 2025 results illustrate how sensitive internalised models remain to volatility regimes. Despite a sharp increase in client activity and nominal turnover, lower market volatility reduced profitability per lot, leading to a significant drop in net earnings.

Volatility vs Profitability: XTB Case (Q3 2025)

How is the revenue model different in futures and options?

Listed futures and options fundamentally reframe the broker’s role. Instead of acting as principal, the broker operates primarily as an intermediary connected to an exchange and a clearinghouse.

Revenue is driven mainly by commissions and exchange fee mark-ups rather than by client trading losses.

Margins per contract are typically thinner but more predictable. Brokers do not control spreads in the same way as in OTC products because prices are formed in a central order book,

At the same time, listed derivatives open other revenue channels. Interest on client cash balances, margin financing for active accounts, and paid access to market data or advanced trading tools become increasingly important. The broker’s economics shift from warehousing risk to monetising infrastructure, scale and client engagement.

How is the revenue model different in futures and options

Does that mean revenues will fall?

In the near term, most firms should expect pressure. The reduction of B-Book P&L removes a high-margin, volatility-amplified revenue stream. Replacing it with commission income typically lowers revenue per active client, particularly in the early stages of transition. Competition in listed derivatives is transparent and fee-driven, limiting pricing power.

The medium-term picture, however, is more nuanced. Industry research and broker disclosures suggest that listed derivatives tend to attract a more engaged and better-capitalised segment of retail traders.

A 2025 Acuiti report for CME Group noted that active futures and options traders are more consistent in their activity and more willing to pay for data, analytics and professional tools than mass-market CFD clients.

While per-trade margins are thinner in exchange-traded products, higher engagement and more stable trading patterns can support improved lifetime value over time.

IG’s US division illustrates this divergence. Exchange-traded derivatives revenue grew 21% year-on-year in USD terms, with revenue per customer up 4%, while OTC revenue per customer declined. The data suggests stronger monetisation momentum in listed products relative to principal-based flow.

IG Group's annual repot (2025)

Listed derivatives also reduce regulatory tail risk. Revenue tied to centrally cleared products is less vulnerable to sudden product bans than income derived from high-leverage OTC contracts. That stability becomes increasingly important when firms commit capital to technology, marketing and balance sheet expansion.

For many firms, the shift toward listed derivatives is not purely opportunistic. In markets where high-leverage OTC products face increasing restrictions, futures and options offer a way to preserve a retail derivatives franchise within a more durable regulatory framework.

What is the biggest obstacle?

Technology integration and regulatory permissions are significant, but the primary constraint is client education. For more than a decade, retail traders in Europe were introduced to derivatives primarily through CFDs, which are perpetual, standardised and relatively simple to understand in notional terms.

Futures and options demand a more complex mental framework involving contract multipliers, margin variation, expiries and, in the case of options, volatility and time decay.

Bridging that gap requires sustained investment in structured education, simulation tools and support infrastructure. In the short term, these costs weigh on margins. In the longer term, they determine whether a broker can cultivate a stable, higher-value client base in listed derivatives.

The most plausible outcome is a hybrid model. Where regulation allows, CFDs will remain for smaller tickets and niche exposures, while futures and options anchor core index, rates and commodity trading.

The revenue mix will gradually shift away from principal risk and toward commissions, financing and services.

Margins per trade are likely to compress across the industry, making scale and cross-selling more important.

Smaller, pure-CFD operators may struggle to fund the infrastructure required for listed derivatives and could consolidate or pivot to introducing-broker models.

Larger, well-capitalised firms with multi-jurisdictional licences and strong technology stacks are positioned to capture share.

Over time, the share of group revenue derived from pure B-Book risk-taking is likely to decline.

The transition does not necessarily shrink revenues outright. Instead, it changes their composition and reduces their volatility. Firms that adapt early may end up with lower per-trade margins but more diversified and resilient earnings.

Those that remain heavily dependent on high-leverage OTC flow face an increasingly binary risk profile in a regulatory environment that shows little sign of softening.

Tanya Chepkova is a News Editor at Finance Magnates with more than 16 years of experience in financial journalism, covering forex, crypto, and digital asset markets. Her work spans daily industry reporting and data-driven, long-form explainers focused on market structure, trading models, and regulatory shifts.

Before joining Finance Magnates, she led the editorial team of a cryptocurrency-focused media outlet for six years. Her reporting combines analytical depth with clear storytelling, with particular attention to how structural changes in trading, stablecoin infrastructure, and emerging products such as prediction markets reshape the broader financial ecosystem. She covers global developments and provides additional insight into CIS markets.

Areas of Coverage:

Crypto and digital asset markets

Prediction markets

Stablecoins and cross-border payments

Industry analysis and long-form explainers

XTB Signs Olympique Lyonnais Shirt Deal Four Days After FC Porto Agreement

Featured Videos

CFD Activity Falls; MetaQuotes 1 Trillion AI Token Use

CFD Activity Falls; MetaQuotes 1 Trillion AI Token Use

CFD Activity Falls; MetaQuotes 1 Trillion AI Token Use

CFD Activity Falls; MetaQuotes 1 Trillion AI Token Use

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews