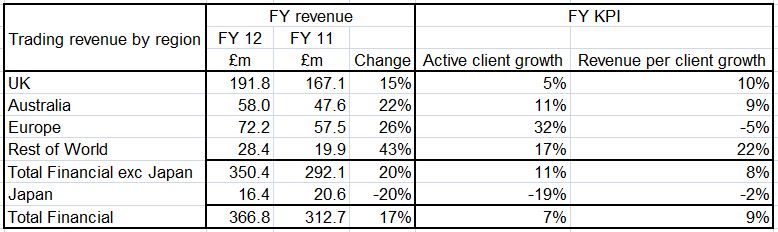

The Group expects to report trading revenue of £366.8m excluding the discontinued Sport business (2011: £312.7m), representing growth of 17% over the comparative period.

The UK had a strong quarter with revenue growth of 13%, primarily driven by growth in revenue per client which was the highest of any quarter during the year, resulting in revenue per client growth of 10% for the full year.

Very muted consumer sentiment in the final quarter in Australia led to reduced client activity and a fall of 1% in both revenue per client and active client numbers.

The Group's European businesses continued to deliver strong growth in active client numbers which, as expected, was slightly offset by the progressive fall in revenue per client as these businesses become more established and the impact of high value early adopters is diluted. The growth was primarily driven by Spain, Italy and France.

The continued positive performance from Rest of World was driven by strong growth in both Singapore and South Africa. Growth in Singapore was driven primarily by increased revenue per client while growth in South Africa was driven by higher active client numbers.

The Group continues to see progress from Nadex, which saw a steady increase in clients through the quarter, albeit this remains immaterial to the Group as a whole.

The Group's Japanese business continues to make progress with sequential improvement in revenue per client in each of the last three quarters. Active client numbers have stabilised in the last two quarters, but are lower than those achieved prior to the introduction of final Leverage restrictions in August 2011.