Retail prop trading faces regulatory scrutiny in the US, Canada, and Europe due to reliance on challenge fees more than actual trading. As scrutiny intensifies, prediction markets are drawing more traders. Are they the next stop for retail speculation, or something different?

Why Are Traditional Prop Firms Under Pressure?

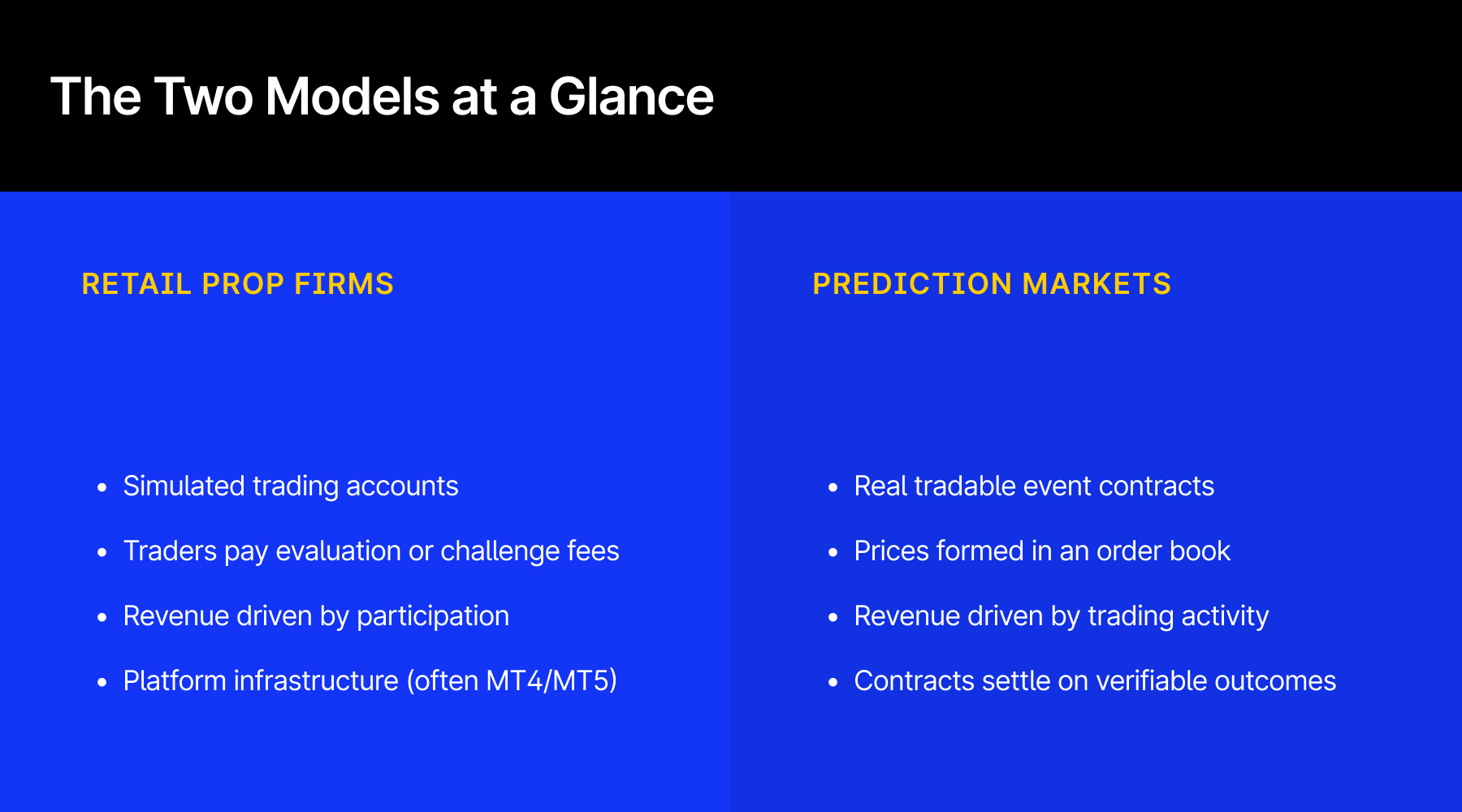

Retail prop trading expanded quickly in the early 2020s as firms began selling access to “funded” accounts through paid evaluation challenges. In most cases, traders operate on simulated accounts, while firms earn revenue from challenge fees rather than trading activity.

The model operates in a regulatory gray zone. Because firms typically do not hold client funds or execute trades on real markets, many operate without the licenses required for brokers or investment firms.

Regulators have started paying closer attention to the sector, particularly when platforms market large funded accounts to retail traders. In the United States, enforcement actions such as the case against MyForexFunds have already signaled that authorities are willing to intervene.

Operational vulnerabilities have also become clear. Many prop firms rely on MetaTrader infrastructure through white-label arrangements. When MetaQuotes tightened licensing policies in 2024, an estimated 80–100 prop firms shut down, roughly 13–14% of global operators.

What Makes Prediction Markets Look Like an Alternative?

Prediction markets have expanded quickly. A 2025 analysis by Keyrock and Dune estimated global trading volume at roughly $44 billion, with Polymarket accounting for about $21.5 billion and Kalshi for $17.1 billion.

Unlike most prop platforms, prediction markets operate through tradable contracts tied to real-world outcomes. Each contract pays a fixed amount if the event occurs and expires at zero if it does not. Prices move between those two outcomes and reflect the market’s implied probability.

This structure also changes how platforms earn revenue, shifting the focus from participation fees toward trading activity.

For companies operating in the retail trading ecosystem, this model has clear appeal. It replaces simulated trading with real contracts and ties revenue more directly to trading activity. That is why prediction markets are increasingly discussed not only as a new asset class, but also as a possible structural pivot for parts of the retail trading industry.

Are Prediction Markets a New Asset Class — or Just a Different Wrapper?

The rapid growth of event trading has revived a familiar debate in retail finance. When a new speculative market appears, the key question is whether it represents a genuinely new financial instrument or simply a familiar model presented in a different form.

Prediction markets are built around a simple structure. Contracts are tied to clearly defined outcomes and settle automatically once the event occurs. Prices trade in an order book and represent the market’s implied probability of that outcome.

Yet the behaviour of traders looks familiar. Retail traders are speculating on short-term outcomes around elections, economic releases, or major sports events.

As the contracts resolve in a simple yes-or-no result, some observers see parallels with earlier retail products built around binary outcomes. Others argue the comparison misses an important distinction.

Unlike many earlier retail trading products, prediction markets link trading directly to verifiable real-world events rather than to internally priced derivatives.

How regulators answer that question will shape the market’s future. If event contracts are treated as financial derivatives, prediction markets may evolve into a new class of tradable instruments. If they are regulated primarily as betting products, the industry could develop along a very different path.

Feature | Prediction Markets | Binary Options (2010s) | Retail Prop Trading |

|---|---|---|---|

Core instrument | Event contract tied to a real-world outcome | Binary option priced by broker | Simulated trading account |

Price formation | Order book and market participants | Set by platform | Based on simulated market prices |

Settlement | Determined by event outcome | Determined by broker pricing | Based on trading rules and evaluation |

Revenue model | Trading fees and spreads | Client losses / platform pricing | Evaluation and challenge fees |

Market exposure | Direct exposure to event probability | Synthetic derivative | Often simulated trading |

Could Prop Firms Pivot to Event Trading?

If pressure on the traditional prop model continues, some firms may begin exploring prediction markets as a possible direction for expansion. The idea would not necessarily be to abandon prop trading entirely, but to adapt the business model around real event contracts instead of simulated trading accounts.

Industry surveys suggest that interest among professional traders is already emerging. A 2025 study by Acuiti found that 10% of proprietary traders were already trading prediction contracts, while 35% expressed interest. Among U.S. firms, 75% said they were trading or planning to trade them.

- Inside the Prediction Markets: When the Real World Hits the Markets

- US Military Action Against Iran Exposes Split Between Polymarket and Kalshi Models

- Inside the Prediction Markets: Building the Broker Stack

One option is to treat prediction markets as an additional product. Firms that already operate trading platforms or communities could allow their users to trade event contracts alongside other speculative instruments.

In that scenario, the firm shifts from selling evaluation challenges to earning revenue from trading activity. Another possibility is deeper integration. Some companies in the retail trading ecosystem could move closer to the infrastructure layer by partnering with existing prediction market exchanges or providing liquidity and trading tools for those markets.

A more ambitious path would involve building proprietary platforms for event trading. In that case, the firm effectively transitions from a prop challenge provider to an operator of a trading venue centred on event contracts.

Whether any of these paths will materialise depends on several factors, including regulation, liquidity, and the willingness of traders to move from simulated accounts to real-money event trading.

What Are Regulators Actually Worried About?

For regulators, the central question is how to classify event contracts. Depending on the jurisdiction, they may be treated as financial derivatives, betting products, or something that sits between the two.

That classification determines which rules apply and which authorities oversee the market. Some industry participants argue that clearer regulation would help bring prediction markets onshore rather than pushing them into offshore platforms.

Great to see bipartisan support for federally-regulated prediction markets in the US. Without CFTC oversight, these markets will only exist offshore - completely unregulated. Important work being done here and glad to be a part of it. https://t.co/AyKAlMKXGI

— Kris | ai.com (@kris) January 13, 2026

Regulators are also concerned about retail participation. Prediction markets often revolve around highly visible events such as elections, economic releases, or major sports competitions, which can attract large numbers of retail traders. Authorities, therefore, pay close attention to marketing practices, risk disclosures, and whether speculative trading is presented as entertainment.

Market integrity is another concern. Because contracts settle on specific outcomes, regulators worry about the misuse of non-public information or attempts to influence the events on which contracts are based.

Structural Shift — or a Familiar Cycle?

Retail trading has a history of reinventing itself when existing models come under pressure. Over the past two decades, the industry has moved through several phases—from FX and CFD brokers to binary options, and more recently to retail prop trading platforms.

Binary options alone generated billions in retail trading volume before regulators shut down much of the industry in the late 2010s.

Prediction markets may represent the next stage in that evolution. They combine elements of financial trading and event-based speculation while operating through tradable contracts rather than simulated accounts. However, Some market observers remain skeptical.

Are prediction markets slowing down?

— LunarCrush (@LunarCrush) March 1, 2026

$94B total volume sounds massive. But $436M in the last 24 hours is the new daily reality, down 80%+ from peak days during the election cycle.

And the most viral prediction market story this week isn't about some brilliant crowd-sourced… pic.twitter.com/LzjukrJ1RV

At the same time, the underlying dynamic has not changed. Retail traders are still drawn to markets that offer clear outcomes, simple structures, and the possibility of quick gains around high-profile events.

A 2026 survey by Coalition Greenwich found that 43% of financial professionals viewed prediction markets positively, while 60% said their data could complement traditional macro indicators.

Whether prediction markets become a durable new asset class or simply another format for retail speculation will depend on how the industry develops over the next few years. Regulation, liquidity, and platform design will all play a role in determining which path the market takes.

One thing is already becoming clear: as the traditional prop model faces increasing scrutiny, parts of the retail trading ecosystem are beginning to explore what might come next.