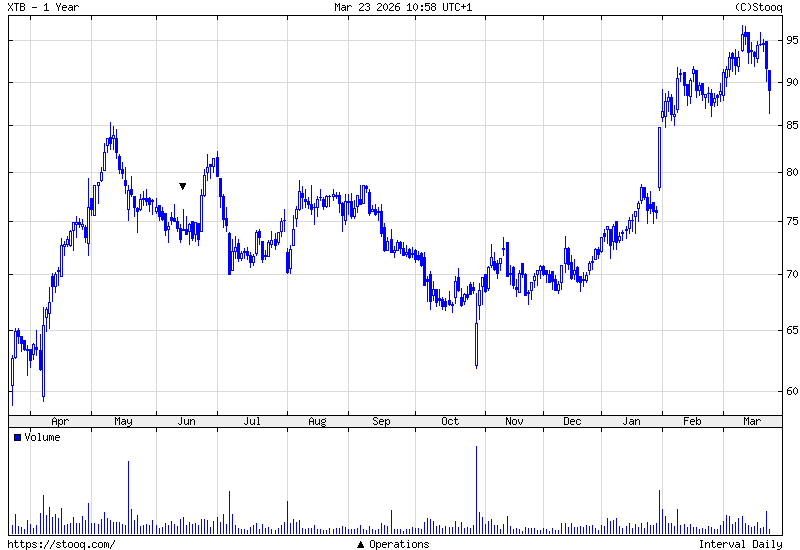

XTB shares fell for a second consecutive session today (Monday), sliding to an intraday low of 86.40 PLN before recovering to around 89.22 PLN, a decline of roughly 2.5% on the day. The pullback, which stretches over two trading sessions, has taken the Warsaw-listed broker (WSE: XTB) to its lowest level since February 24, and represents a roughly 9% retreat from the stock's all-time high of 96.94 PLN reached just two weeks ago on March 10.

Join the inaugural Finance Magnates Singapore Summit 2026, which will bring together brokers, fintechs, banks, EMIs, wealth managers, and hedge funds across APAC.

The pressure dates back to March 19, when XTB published its consolidated annual report for 2025, showing record revenues that masked a sharp deterioration in profitability. Trading the following day opened with heavy selling, with shares dropping from around 94.98 PLN to an intraday low of 90.10 PLN before closing at 91.58 PLN, the steepest single-session decline the stock had seen since November 2025.

XTB’s Record Revenue, Shrinking Profits

The numbers at the top of the income statement were unambiguously strong. Total operating income rose 14.6% year-over-year to PLN 2.15 billion in 2025, a company record, according to the annual report.

KPI | 2024 | 2025 | Change |

Total Operating Revenue | PLN 1,873.4 mln | PLN 2,146.1 mln | +14.6% |

New Clients | 498,438 | 864,286 | +73.4% |

Active Clients | 701,089 | 1,189,422 | +69.7% |

CFD Trading Volume (lots) | 6,274,177 | 8,866,381 | +41.3% |

Stocks & ETF Revenue | PLN 30.7 mln | PLN 78.3 mln | +155.5% |

But operating costs rose nearly three times faster, up 48.2% to PLN 1.31 billion, leaving net profit at PLN 644.2 million, down 24.8% from PLN 856.9 million in 2024. Earnings per share fell from PLN 7.29 to PLN 5.48 over the same period.

- XTB Sells FSCA Unit Five Years After No Operations

- XTB Posts Record Revenue but Net Profit Falls 25% as Marketing Bill Balloons

- XTB Adds a Kill Switch to Its Investment App to Lock Out Hackers

The single largest driver of the cost increase was marketing. XTB's marketing bill rose 69.6% to PLN 584.9 million in 2025, including PLN 405 million in online spending alone, up from PLN 262.3 million a year earlier. Staff costs followed, rising 32.6% to PLN 413 million, while IT and licensing expenses nearly doubled to PLN 73 million from PLN 39.4 million. The net profit margin contracted from roughly 46% in 2024 to around 30% in 2025, a shift investors are struggling to look past.

Two further line items stand out from the report. Financial costs surged from PLN 1.1 million in 2024 to PLN 94.6 million in 2025, driven almost entirely by foreign exchange losses of PLN 93.1 million, primarily the result of PLN strengthening against the dollar and euro. Revenue per active client also fell 32.5%, from PLN 2.7 thousand to PLN 1.8 thousand, a metric that reflects the dilutive effect of bringing in large volumes of lower-activity accounts.

KPI | 2024 | 2025 | Change |

Net Profit | PLN 856.9 mln | PLN 644.2 mln | -24.8% |

Net Profit Margin | 45.7% | 30.0% | -15.7 pp |

Revenue per Active Client | PLN 2,700 | PLN 1,800 | -32.5% |

Profitability per Lot | PLN 275 | PLN 215 | -21.8% |

Return on Equity (ROE) | 45.8% | 32.2% | -13.6 pp |

The Cost Guidance That Unnerved Markets

If the 2025 numbers were the catalyst, it is the company's own forward-looking commentary in the annual report that has kept sellers engaged. The management board states directly in the report: "In 2026, total operating costs may be up to approximately 30% higher compared to what we observed in 2025.

The Management Board's priority is the continued growth of the client base and building a global brand. As a result, marketing expenditures may increase by approximately 50% compared to the previous year," according to the 2025 annual report. The company adds that in the medium term, meaning the 2027 to 2029 horizon, marketing costs could grow 30% to 40% annually, with the assumption that the average cost of client acquisition remains broadly in line with the 2023 to 2026 range.

For investors who had priced in both growth and margin recovery, that kind of guidance leaves little room for optimism in the near term. The firm had forecast full-year 2025 net profit of around PLN 673 million back in January, a figure that ultimately proved reasonably close to the mark, though the context of the cost trajectory heading into 2026 has shifted the picture considerably.

The Client Bet

CEO Omar Arnaout has been consistent in framing client acquisition as the company's defining priority, and the 2025 numbers bear that strategy out. XTB added 864,286 new clients during the year, a 73% jump from 498,438 in 2024, pushing the total base past 2.16 million. In an interview published in February, Arnaout called reaching two million new clients annually "completely realistic" within a few years, noting that "it took us 20 years to have a million clients" and that "in 2025, we acquired over 860,000 clients."

Moreover, asked in an April 2025 interview at XTB's Warsaw headquarters which KPIs matter more, revenue and profit or client acquisition, Arnaout did not hedge:

"I would be lying if I said profit wasn't important to us. But I'll be honest. Even when we present slightly worse financial results to institutional investors, if we see that our client acquisition was very high, clients are actively using our application and are satisfied with it, and deposits were strong with significant increases in trading volumes, personally, that's more important to me than the financial results. It builds a base for a significant increase in profits over time. The end goal will always be reaching the highest level of profits."

That view is difficult to reconcile with the market's reaction, and the tension is a familiar one for XTB investors. The company keeps delivering on client growth, while the market keeps discounting the earnings that growth produces.

The average cost per new client acquisition was PLN 677 in 2025, broadly in line with prior years, but that efficiency metric does not, on its own, resolve the question of whether the aggressive spend is a temporary investment or a structural shift in the cost base.

Profitability per lot, a key operating metric, also deteriorated, falling 21.8% to PLN 215 from PLN 275 in 2024. Volume grew sharply but at diminishing returns. On a quarterly basis, Q4 2025 was the weakest period of the year, with net profit of just PLN 160.3 million, compared to a peak of PLN 302.7 million in Q2.

Africa Exit and Institutional Weakness

The annual report also disclosed the sale of XTB's South African subsidiary for $645,000 to an unnamed buyer, closing out an eight-year attempt to enter the African continent that never generated a single client transaction. The deal, signed on February 17, 2026, and still pending FSCA regulatory approval, represents a minor write-off in financial terms, but it underscores a pattern of geographic retreats outside XTB's European core.

Separately, the company's institutional segment, operated under the X Open Hub brand, saw revenues fall 48.3% year-over-year to PLN 42.5 million in 2025, a notable reversal from the PLN 82.3 million generated in 2024. The segment, which provides liquidity and trading technology to other financial institutions, is known for revenue volatility, but the scale of the decline adds another layer of nuance to what was otherwise a strong top-line year.

Technicals Remain Strong

From a technical perspective, the picture remains within a broader consolidation range. The stock has been trading between approximately 86 PLN, a support level defined by the gap formed during the January and February rally, and approximately 96 PLN, the vicinity of the all-time high.

At 89.22 PLN, the shares sit closer to the lower end of that range than the upper, but remain well above the early 2025 lows that preceded the strong rally now partially reversing. XTB shares have experienced sharp pullbacks before, including a 25% decline from peak to trough in mid-2025, only to recover fully and push to new highs.

Whether this episode follows a similar path depends on whether investors conclude that the company's aggressive spending is building lasting franchise value, or eating into the very earnings that justified the stock's premium valuation in the first place.