We look at three fintech trends that are slated to grow during 2015 but that also have their risks. The uniform theme of each is that they use technology to bring efficiency to the financial markets.

Finance Magnates

Fintech was a great sector to be in during 2014, being the beneficiary of hundreds of millions, if not billions, of dollars of venture capital. The year ended with a bang, with alternative non-bank lenders LendingClub and OnDeck both going public. Overall, the forces of momentum guiding the fintech sector are based on a perfect storm of emerging technology, public desire for financial transparency as well as government regulation beginning to favor capital market alternatives following the global financial crisis.

Looking towards 2015, there are a few trends that are worth watching within the industry, as they could become either huge opportunities or stumbling blocks. Along with them we present reasons why the trend may not create the pot of gold expected of it.

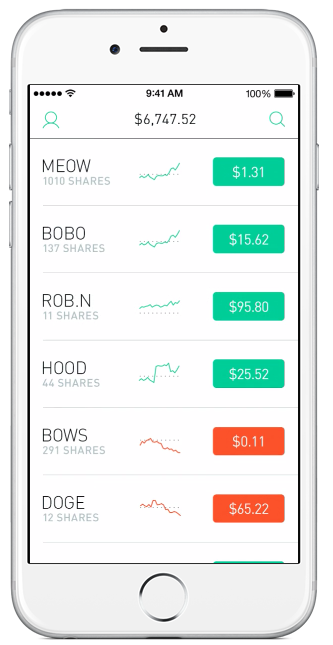

1) "Service-based investing" – If you haven’t heard of this term yet, it's for good reason, since it's being made up now (idea first appeared when we reviewed Simply Wall St). "Service-based investing" or perhaps better termed "low-cost service-based investing" is a term I am coining for an upcoming industry of paid services around low cost investing.

The idea isn’t new, though, with other brokers like Zecco having tried a commission-free model in the past only to scrap it later. In RobinHood’s case, an area of friction is that their target audience for maximum revenues are speculative investors who will be routinely using margin. Those customers, though, don’t seem like candidates to trust their investing choices to a mobile app.

This is where the "service-based" companies come in. Along with its brokerage services, RobinHood will be providing developer access for the creation of trading apps like charts, signals, fundamental analysis, etc. It’s these "paid" products that might ultimately attract experienced traders and speculators to RobinHood. The combination of paid apps with commission-free investing could result in a combination of sophisticated trading products in an environment that costs less than what one or two trades would cost at a competing online broker.

Why it won’t work – One of my childhood memories is seeing a movie which was abruptly stopped when the sound system at the theater failed. In addition to ticket reimbursement, the movie theater offered free food from the concession stand, with the announcement being followed by two dudes saying loudly, "IF IT'S FOR FREE IT'S FOR ME."

On this note, service-based investing has to look no further than the forex industry to see why it won’t work. Unlike in other asset classes, customers are provided free everything. From platforms to analysis to webinars, there are plenty of free offerings to seduce forex customers. As such, getting clients to pay for added services and third party offerings is rarely an effective business model. The result is that the best products tend to be licensed by brokers and offered for free to their customers, while paid offerings are limited to get-rich-quick-scheme items like signals and expert advisors, where the majority aren’t marketed by the broker.

A similar fate could take place among RobinHood customers and any other similar model that copies it. Like in the forex industry, stock traders that are attracted to "free" may be adverse to paying for premium products.

2) Robo investing – Unlike service-based investing, robo investing is a topic that has appeared on our pages and many others during 2014. I like to think of robo investing as the anti-social trading. With social trading, the big buzz word is democratization of investing, where anybody can develop a track record and become trade leaders.

With robo investing, the edge rests with the fact that managed investments underperform over the long term when taking fees into account. Therefore, why not build low cost portfolios that simply invest in indexes. The year 2014 was a breakout year for robo investing with the leaders in the space, Wealthfront, Betterment and Nutmeg, probably now having reached around three billion in assets.

The total figure of assets under management is still a drop in the bucket compared to actively managed funds. But the low cost and simple approach makes sense for many long-term savers who don’t want to ruffle through pages of prospectuses and understand terms like Net Asset Values, Performance Fees and Up-front Charges. With robo investing, users enter information such as their age, risk tolerance, years until retirement and expected savings amount. The platforms then automatically invest funds in ETFs that track indexes. This is all done for fees at a fraction of those charged at actively managed mutual funds and professional financial advisors.

Why it won’t work – There is little doubt that the products work and hitting a hundred billion dollars in managed robo-invested assets is an easy bet to make. Nonetheless, the fear here is that incumbents like Charles Schwab, Fidelity and Vanguard will enter the market and commoditize robo investing. It will remain a high-growth sector, but the already tight margins will get even smaller. The early players, though, stand to do well as the market grows and could be compensated handsomely as buyout candidates when (and if) existing financial-advisor behemoths decide to buy their way into the market. But, smaller players and new firms may find it too tough to scale large enough to become profitable.

Why it won’t work – With digital crowdfunding, at this point there remain more questions than answers. Nothing stands in the way more than regulation. Selling company shares is a highly regulated process, with restrictions on how a stock sale is marketed, who can be a shareholder, etc. Fiat-based equity crowdfunding platforms have been able to carve a niche in the UK and US by becoming broker dealers and pre-vetting who can raise funds and invest.

With digital crowdfunding, one of the current appeals is that it is borderless and small increments can be sold at a time. As such, there isn’t much about it yet that fits into the existing financial framework of stock sales. But it may not be illegal either as stocks can be offered as digital coins purchases, with their real ownership being decided on at a later date when regulatory rules become known.

Another issue is how to buy digital shares. As decentralized exchanges, digital crowdfunding platforms rely on pricing shares based on bitcoin. This presents a stumbling block for anyone that doesn’t have bitcoins. However, this is an easier barrier than regulation, as third-party companies can be created that accept fiat, convert them to bitcoins and use custodial services such as Bitreserve to remove bitcoin price risk.

Fintech was a great sector to be in during 2014, being the beneficiary of hundreds of millions, if not billions, of dollars of venture capital. The year ended with a bang, with alternative non-bank lenders LendingClub and OnDeck both going public. Overall, the forces of momentum guiding the fintech sector are based on a perfect storm of emerging technology, public desire for financial transparency as well as government regulation beginning to favor capital market alternatives following the global financial crisis.

Looking towards 2015, there are a few trends that are worth watching within the industry, as they could become either huge opportunities or stumbling blocks. Along with them we present reasons why the trend may not create the pot of gold expected of it.

1) "Service-based investing" – If you haven’t heard of this term yet, it's for good reason, since it's being made up now (idea first appeared when we reviewed Simply Wall St). "Service-based investing" or perhaps better termed "low-cost service-based investing" is a term I am coining for an upcoming industry of paid services around low cost investing.

The idea isn’t new, though, with other brokers like Zecco having tried a commission-free model in the past only to scrap it later. In RobinHood’s case, an area of friction is that their target audience for maximum revenues are speculative investors who will be routinely using margin. Those customers, though, don’t seem like candidates to trust their investing choices to a mobile app.

This is where the "service-based" companies come in. Along with its brokerage services, RobinHood will be providing developer access for the creation of trading apps like charts, signals, fundamental analysis, etc. It’s these "paid" products that might ultimately attract experienced traders and speculators to RobinHood. The combination of paid apps with commission-free investing could result in a combination of sophisticated trading products in an environment that costs less than what one or two trades would cost at a competing online broker.

Why it won’t work – One of my childhood memories is seeing a movie which was abruptly stopped when the sound system at the theater failed. In addition to ticket reimbursement, the movie theater offered free food from the concession stand, with the announcement being followed by two dudes saying loudly, "IF IT'S FOR FREE IT'S FOR ME."

On this note, service-based investing has to look no further than the forex industry to see why it won’t work. Unlike in other asset classes, customers are provided free everything. From platforms to analysis to webinars, there are plenty of free offerings to seduce forex customers. As such, getting clients to pay for added services and third party offerings is rarely an effective business model. The result is that the best products tend to be licensed by brokers and offered for free to their customers, while paid offerings are limited to get-rich-quick-scheme items like signals and expert advisors, where the majority aren’t marketed by the broker.

A similar fate could take place among RobinHood customers and any other similar model that copies it. Like in the forex industry, stock traders that are attracted to "free" may be adverse to paying for premium products.

2) Robo investing – Unlike service-based investing, robo investing is a topic that has appeared on our pages and many others during 2014. I like to think of robo investing as the anti-social trading. With social trading, the big buzz word is democratization of investing, where anybody can develop a track record and become trade leaders.

With robo investing, the edge rests with the fact that managed investments underperform over the long term when taking fees into account. Therefore, why not build low cost portfolios that simply invest in indexes. The year 2014 was a breakout year for robo investing with the leaders in the space, Wealthfront, Betterment and Nutmeg, probably now having reached around three billion in assets.

The total figure of assets under management is still a drop in the bucket compared to actively managed funds. But the low cost and simple approach makes sense for many long-term savers who don’t want to ruffle through pages of prospectuses and understand terms like Net Asset Values, Performance Fees and Up-front Charges. With robo investing, users enter information such as their age, risk tolerance, years until retirement and expected savings amount. The platforms then automatically invest funds in ETFs that track indexes. This is all done for fees at a fraction of those charged at actively managed mutual funds and professional financial advisors.

Why it won’t work – There is little doubt that the products work and hitting a hundred billion dollars in managed robo-invested assets is an easy bet to make. Nonetheless, the fear here is that incumbents like Charles Schwab, Fidelity and Vanguard will enter the market and commoditize robo investing. It will remain a high-growth sector, but the already tight margins will get even smaller. The early players, though, stand to do well as the market grows and could be compensated handsomely as buyout candidates when (and if) existing financial-advisor behemoths decide to buy their way into the market. But, smaller players and new firms may find it too tough to scale large enough to become profitable.

Why it won’t work – With digital crowdfunding, at this point there remain more questions than answers. Nothing stands in the way more than regulation. Selling company shares is a highly regulated process, with restrictions on how a stock sale is marketed, who can be a shareholder, etc. Fiat-based equity crowdfunding platforms have been able to carve a niche in the UK and US by becoming broker dealers and pre-vetting who can raise funds and invest.

With digital crowdfunding, one of the current appeals is that it is borderless and small increments can be sold at a time. As such, there isn’t much about it yet that fits into the existing financial framework of stock sales. But it may not be illegal either as stocks can be offered as digital coins purchases, with their real ownership being decided on at a later date when regulatory rules become known.

Another issue is how to buy digital shares. As decentralized exchanges, digital crowdfunding platforms rely on pricing shares based on bitcoin. This presents a stumbling block for anyone that doesn’t have bitcoins. However, this is an easier barrier than regulation, as third-party companies can be created that accept fiat, convert them to bitcoins and use custodial services such as Bitreserve to remove bitcoin price risk.

90% Adoption: How AI Is Reshaping French Investment Firms

Featured Videos

CMC Markets’ Artur Delijergijevs on Metals Demand, Volatility, & Stable Execution

CMC Markets’ Artur Delijergijevs on Metals Demand, Volatility, & Stable Execution

CMC Markets’ Artur Delijergijevs on Metals Demand, Volatility, & Stable Execution

CMC Markets’ Artur Delijergijevs on Metals Demand, Volatility, & Stable Execution

In this exclusive Executive Interview, Finance Magnates speaks with Artur Delijergijevs, Head of Systematic Market Making at CMC Markets, about the current state of metals demand and market volatility.

Delijergijevs offers a desk-level view on:

- Metals Demand: Why metals are seeing the strongest demand from both retail and institutional clients right now.

- The Safe-Haven Debate: Questioning whether gold still fits the classic safe-haven definition given large daily price movements.

- Volatile Market Prep: How a market-making desk prepares its systems and pricing for stressed market conditions and high-impact economic events.

- Hybrid Execution: Why the best execution model combines electronic speed with human relationship support, especially during volatility.

- AI in Workflow: Where CMC Markets is integrating machine learning for risk management and pricing, and the limitations of AI during stressed markets.

- Dubai's Role: The strategic importance of Dubai’s location for covering global trading sessions across Asia, Europe, and the US.

Watch to understand how CMC Markets maintains stable pricing and reliable execution quality in high-volatility environments.

#CMCmarkets #forex #metals #gold #trading #volatility #MarketMaking #iFXDubai #FinanceMagnates #Finance #Fintech #Execution #AlgorithmicTrading #RiskManagement

In this exclusive Executive Interview, Finance Magnates speaks with Artur Delijergijevs, Head of Systematic Market Making at CMC Markets, about the current state of metals demand and market volatility.

Delijergijevs offers a desk-level view on:

- Metals Demand: Why metals are seeing the strongest demand from both retail and institutional clients right now.

- The Safe-Haven Debate: Questioning whether gold still fits the classic safe-haven definition given large daily price movements.

- Volatile Market Prep: How a market-making desk prepares its systems and pricing for stressed market conditions and high-impact economic events.

- Hybrid Execution: Why the best execution model combines electronic speed with human relationship support, especially during volatility.

- AI in Workflow: Where CMC Markets is integrating machine learning for risk management and pricing, and the limitations of AI during stressed markets.

- Dubai's Role: The strategic importance of Dubai’s location for covering global trading sessions across Asia, Europe, and the US.

Watch to understand how CMC Markets maintains stable pricing and reliable execution quality in high-volatility environments.

#CMCmarkets #forex #metals #gold #trading #volatility #MarketMaking #iFXDubai #FinanceMagnates #Finance #Fintech #Execution #AlgorithmicTrading #RiskManagement

In this exclusive Executive Interview, Finance Magnates speaks with Artur Delijergijevs, Head of Systematic Market Making at CMC Markets, about the current state of metals demand and market volatility.

Delijergijevs offers a desk-level view on:

- Metals Demand: Why metals are seeing the strongest demand from both retail and institutional clients right now.

- The Safe-Haven Debate: Questioning whether gold still fits the classic safe-haven definition given large daily price movements.

- Volatile Market Prep: How a market-making desk prepares its systems and pricing for stressed market conditions and high-impact economic events.

- Hybrid Execution: Why the best execution model combines electronic speed with human relationship support, especially during volatility.

- AI in Workflow: Where CMC Markets is integrating machine learning for risk management and pricing, and the limitations of AI during stressed markets.

- Dubai's Role: The strategic importance of Dubai’s location for covering global trading sessions across Asia, Europe, and the US.

Watch to understand how CMC Markets maintains stable pricing and reliable execution quality in high-volatility environments.

#CMCmarkets #forex #metals #gold #trading #volatility #MarketMaking #iFXDubai #FinanceMagnates #Finance #Fintech #Execution #AlgorithmicTrading #RiskManagement

In this exclusive Executive Interview, Finance Magnates speaks with Artur Delijergijevs, Head of Systematic Market Making at CMC Markets, about the current state of metals demand and market volatility.

Delijergijevs offers a desk-level view on:

- Metals Demand: Why metals are seeing the strongest demand from both retail and institutional clients right now.

- The Safe-Haven Debate: Questioning whether gold still fits the classic safe-haven definition given large daily price movements.

- Volatile Market Prep: How a market-making desk prepares its systems and pricing for stressed market conditions and high-impact economic events.

- Hybrid Execution: Why the best execution model combines electronic speed with human relationship support, especially during volatility.

- AI in Workflow: Where CMC Markets is integrating machine learning for risk management and pricing, and the limitations of AI during stressed markets.

- Dubai's Role: The strategic importance of Dubai’s location for covering global trading sessions across Asia, Europe, and the US.

Watch to understand how CMC Markets maintains stable pricing and reliable execution quality in high-volatility environments.

#CMCmarkets #forex #metals #gold #trading #volatility #MarketMaking #iFXDubai #FinanceMagnates #Finance #Fintech #Execution #AlgorithmicTrading #RiskManagement

Finance Magnates Awards 2026 – Nominations Now Open

Finance Magnates Awards 2026 – Nominations Now Open

Finance Magnates Awards 2026 – Nominations Now Open

Finance Magnates Awards 2026 – Nominations Now Open

Finance Magnates Awards 2026 – Nominations Now Open

Finance Magnates Awards 2026 – Nominations Now Open

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech