The Aite Group has released its most recent look at the global FX market in a report titled Global FX Market Update 2015: Growth Spurts and Electronification Roadblocks and written by Javier Paz and Howard Tai. According to the report, Aite Group believes that increases in activity during the last four months of the year have boosted overall volumes to achieve record trading during 2014.

For the year, Aite Group expects the industry to have achieved average daily volumes (ADV) of $5.5 trillion, 3.8% above figures reported by the Bank of International Settlements in its Triennial FX Survey published in September 2013. Volume growth is attributed to an increase of electronic trading taking place in all aspects of the FX market.

As reported several times by Forex Magnates, electronic trading has made it easier for FX participants to source tight pricing. But this has resulted in increased competition among dealers over price, with falling FX trading margins being mitigated by volume growth.

Other key points of the report:

Electronification winners and losers: Winners include non-bank market makers, third party terminals such as Bloomberg and Reuters, and both single dealer and multi dealer platform providers. Losers are what they call “other banks” (i.e. non-reporting banks), electronic broking duopolies.

Electronification friction: Voice and chat tools continue to be used in the market for price discovery, which has driven relationship-based trades to remain strong.

UK vs US electronification: The UK accounts for 40% of global FX turnover but lags the US in uptake of electronic trading.

Retail FX: Forecasts of double digit growth for 2014 for the non-Japanese retail market, with volumes slightly below “a very good 2013” this year. Overall retail industry FX turnover is estimated at $413 billion ADV.

Volume trends: FX volumes grow but in spurts. This means that the market has periods of flat trading to negative growth followed by spikes in activity (a great example is 2014’s lackluster trading until September’s Volatility rolled along).

$7.8 trillion estimate for 2019: Aite Group estimates FX volumes to near $8 trillion a day in 2019. The bulk of the growth is expected to come from swaps and spot trading.

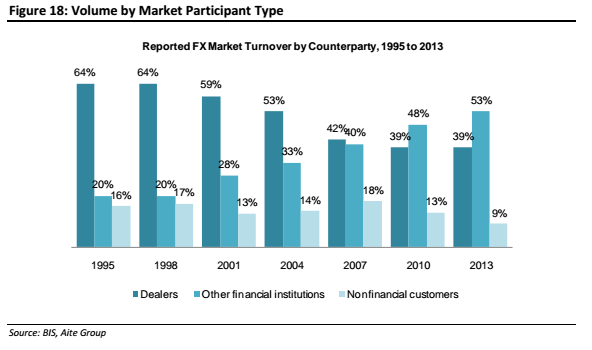

Market participants: The “Other Financial Institutions” category that is defined by the BIS as smaller banks, retail aggregators, HFT firms and hedge funds accounted for 55% of trading volumes in 2013. The Aite Group explains this due to FX being accepted as an asset class, adoption of electronic execution tools and legitimization of the retail industry.