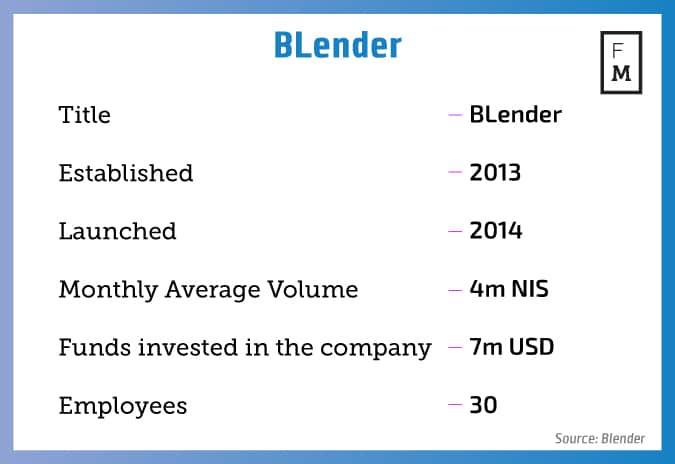

Established in 2013 by three physicists, Israeli peer to peer lending start-up BLender gains strength in the local market. With $7 million invested, a recent investment by leading local investment house and over 270 million NIS in requested loans, CEO and founder Dr. Gal Aviv speaks with Finance Magnates about the growing trends in non-banking lending system landscape.

The peer to peer lending industry is seeing steady growth. What does BLender have to offer to clients that your competitors don’t have?

The P2P lending industry is definitely growing, and we are proud to be a disruptive leader. In Israel, we are the largest and fastest growing platform. Globally we are able to address countries with big potential and lack of competition due to our unique technology.

When we started, we were asking ourselves how come some countries have many online lenders, while others, like Israel, don't. The answer was – lack of credit information and a high fraud rate. With the business goal of targeting these untouched territories, we started developing our technology.

We understand that lenders want to see online lending just like any bond they purchase in the Stock Exchange – liquid and reliable

Today, with our technology, we able to address Latin America, Asia and Africa – a blue ocean, with very little competition, but very interesting markets. These markets are dominated by banks that due to high operating costs cannot provide competitive offerings to their customers.

Take the lead from today’s leaders. FM London Summit, 14-15 November, 2016. Register here!

In order to analyze our potential borrowers’ credit and information, we have created Rating. This feature allows us to receive a broad overview of the borrowers’ repayment ability. After an initial assessment, we use our own automatic matching feature to optimize matching between borrowers and lenders.

We understand that lenders want to see online lending just like any bond they purchase in the stock Exchange – liquid and reliable. So we offer a secondary market for buying and selling loan portfolios.

Furthermore, lenders want to know that their money is safe. We provide our lenders comfort using our SafeGuard fund that minimizes the lender’s risk of the borrowers’ default. It provides an additional layer of protection for the lenders, enabling them to invest money with the peace of mind many look for, while receiving high returns on investments that are vary scares these days.

Tell us a bit about BLender’s unique method of risk assessment. What kind of parameters are you looking for in an accountable lender/borrower?

Dr. Gal Aviv. (Sivan Farag)

While we all use the internet, we tend to forget about the trail we leave behind – just like Hansel and Gretel, our systems collect the little pieces of candy left behind by people, and through machine learning we are able to profile borrowers and determinate their ability to repay their loans. Our risk assessment methods have proven themselves over time, and are only getting better and better.

In terms of lenders, people often think you need to be very rich or a master of investments to have access to relatively safe assets with above average returns. We allow everyday investors to lend in either a fully automatic process, or a flexible selection. The system is easy to use, having both non-techy and sophisticated traders use it.

What are the main advantages and shortcomings of peer to peer lending in comparison to bank loans?

Peer to peer lending is fast, reliable and much less expensive. Because our process is almost fully automatic, our running costs are very low in comparison with banks. These savings are directly related to the offerings we are able to give to borrowers.

We have customers that during a bus ride from work to home, have filled a loan application and had it funded during the next business day. We make sure to use everyday language to prevent any misunderstandings and unnecessary legal phrases that are commonly used by the banks.

On the other hand, banks have a long relationship with the customer as everyone has a bank account. They provide all the financial needs but at a cost. They kind of remind us of the travel agent that used to book our flight tickets and hotel rooms. There are still many travel agents, but today we know that we can do many things faster and cheaper online.

What are the most common reasons that people ask for a loan, and is there a dominant trend?

Our borrowers normally take loans for 'lifestyle needs' - vacations, education, weddings, debt consolidation and home renovations, are the most dominant reasons.

Today, a loan is simply a means of growth and expansion for the common household

Today, a loan is simply a means of growth and expansion for the common household. A loan is no longer a testimony of a financial difficulty, it’s as common as a home mortgage. The biggest trend we have noticed is that customers are seeking technological financial solutions and are no longer satisfied with traditional banking solutions.

They expect to resolve all their financial needs over their smartphones. That’s why many banks are trying to catch up with the technology and are starting to offer services over an app or online. But still, at the end of the day, with the banks you will always have to pay a visit to the clerk.

In which countries is BLender regulated, where does BLender expect to expand to, and why?

We are assessing risk in territories where there is a lack of credit information or a risk of high fraud. We are able to offer consumer loans and credit accessibility in places where credit is expensive, not competitive and simply insufficient.

We target Latin America, Asia and Africa. Having a fully online process also allows us to provide offerings to clients that are in remote areas, away from a local bank or simply far from our headquarters.

Currently we are regulated in Israel and several countries in Europe, but you will have to wait for our upcoming press conference, where we will announce the launch of our new international operations.

What are your main goals over the next 5 years?

Becoming the Leading Multi-Continental Consumer Lending P2P Platform. Our ultimate vision is to enable borrowers to obtain direct access to consumer credit.

We are building a new asset class, enabling lenders and investors to fund consumer loans directly, on a multi-continental basis, via a singular and harmonized platform.