According to a new report from CB Insights, developing markets and consolidation are key to the development of fintech.

FM

Late last week, a new report from technology trend software firm CB Insights made a big splash on the fintech scene: the report, which focused on developments in the fintech industry throughout 2019.

The number most cited by the press was the total sum of fundraising by fintech companies throughout 2019: $34.5 billion.

On its face, it appeared as though there was a significant decrease in fintech funding from the prior year, which saw a sum of $40.8 billion in funding.

However (as the report pointed out), when we exclude Ant Financial's massive $14 billion round from 2018's sum, there is actually a significant increase between the two years: excluding Ant Financial, funding rose from $26.8 billion to $34.5 billion year-over-year, an increase of nearly 30 percent.

In other words, fintech is growing--and fast. But the industry has already started to evolve, with a greater focus on later-stage startups, consolidation, and developing markets.

A shift away from early-stage startups

A number of these trends that seem to suggest maturation in the fintech industry--a movement away from the creation of many singularly-focused startups, and toward supporting relatively more-established companies that are seeking to scale their businesses.

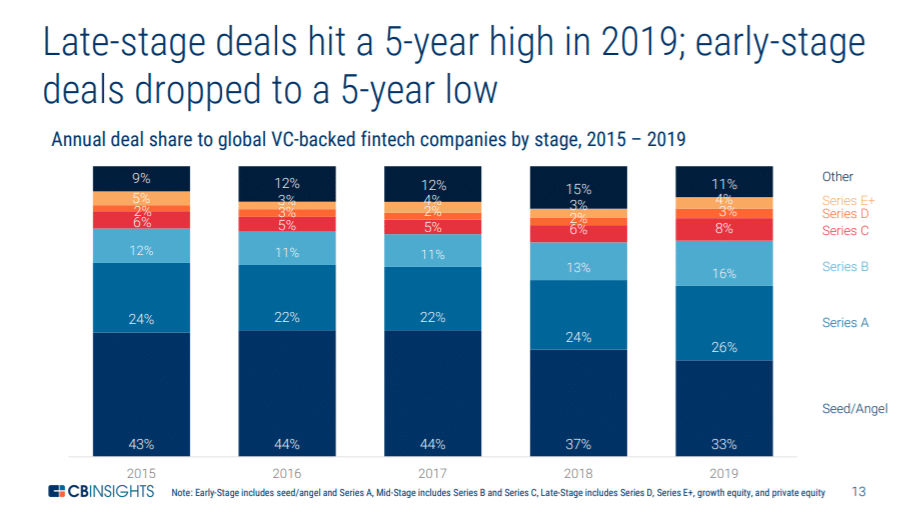

For example, there was an important shift in where this funding was being directed towards: in 2019, funding for early-stage startups reached a five-year low, while funding for later-stage startups hit a five-year high. Early-stage companies received $5.3 billion last year, down from $6.5 billion in 2018.

There were also fewer deals overall from 2018 to 2019; the total number of fundraising rounds decreased roughly 7 percent from 2049 to 1913.

Part of the reason for this particular decline was the fact that there were simply fewer fintech startup companies being launched. For example, only three new insurtech companies were launched in the first three quarters of last year, while 12 had been launched in 2018, and a whopping 109 had been launched in 2017.

Maturation and consolidation

In other words, the fintech industry seems to be trending toward consolidation: fewer companies and fewer funding rounds--but higher rewards for companies who have managed to prove themselves over the last two years.

This, of course, has been accompanied by more merging and acquisition activity: Sandeep Todi, co-founder and chief business officer at Remitr, told Finance Magnates that he has also seen a movement toward consolidation in fintech: "we're now at a place of clutter with too many singular solutions, which is why there's so much activity in acquisitions," he said.

Sandeep Todi, co-founder and chief business officer at Remitr.

For example, in the three months that have passed since the year began, "we've seen [mergers and acquisitions] like Lending Club's purchase of Radius, and Visa's [purchase of] Plaid," Mr. Todi explained. "The most recent is the [news that] Intuit is acquiring CreditKarma."

All of this represents an important shift in the way that the fintech industry is conceptualized: "the incumbents no longer see the value of fintech," Mr. Todi said; rather, "they know it, which is why we'll continue to see a 'rebundling' in financial technology."

As such, "these acquisitions point towards later stage fintechs reaching maturity, making a significant impact, and therefore attracting more investor attention and funding."

Activity in the fintech arena is drawing more and more companies into financial services

Therefore, Mr. Todi believes that this shift toward consolidation and industry maturity "bodes well for any fintech that has integration with other financial services in its DNA, thus giving it an inherent scale and ready to accept funding."

For example, this push toward fintech has manifested in the form of Google's checking accounts, which will allegedly be available sometime in the next year, and Apple's partnership with Goldman Sachs in 2018 to launch the Apple Card, which has now facilitated the lending of over $10 billion to users. In late 2018, Uber launched "Uber Cash," a feature that the company branded as "[allowing] you to plan ahead by adding funds upfront for a seamless payment experience across Uber's service."

In the longer term, this trend toward adding financial services could bring even more companies into the fintech arena. Peter R. Deans, creator and founder of Australian-based 52 Risks, explained to Finance Magnates that, therefore, "despite the drop in overall funding...we are continuing to see an increasing proliferation of fintech entrants in every market around the world."

Peter R. Deans, creator and founder of Australian-based 52 Risks.

Proliferation and discrimination

In addition to the scaling opportunities that fintech integration presents, Mr. Dean said that the trend toward fintech "reflects a number of factors."

Specifically, Mr. Deans named "continued strong in interest in fintech as a segment," and "market acceptance and traction of fintech offerings." Another important fueling factor to the fintech industry, however, is the fact that increasingly, "regulators [are] encouraging new entrants through more accommodating legislation and regulatory changes."

Mr. Deans pointed out that the forces pushing the proliferation of fintech may also be fueling discretion among investors: "there are a lot of investment opportunities and we are seeing angel, seed, and [venture capital] investors being somewhat more discriminating."

"In addition, financial services groups are becoming more adept at identifying the 'right' fintech firms to partner with but usually at a later stage."

A smaller number of fintech funding deals, but the average size of each deal increased from 2018

And when the "right" fintech firms are found--both by potential partners and investors--the cash starts to flow.

"I think both the VC investors and Financial Services firms investing in fintech firms are getting better at identifying the true disruptors," Peter Deans said, "and are directing larger amounts of money at getting these businesses scaled up quickly."

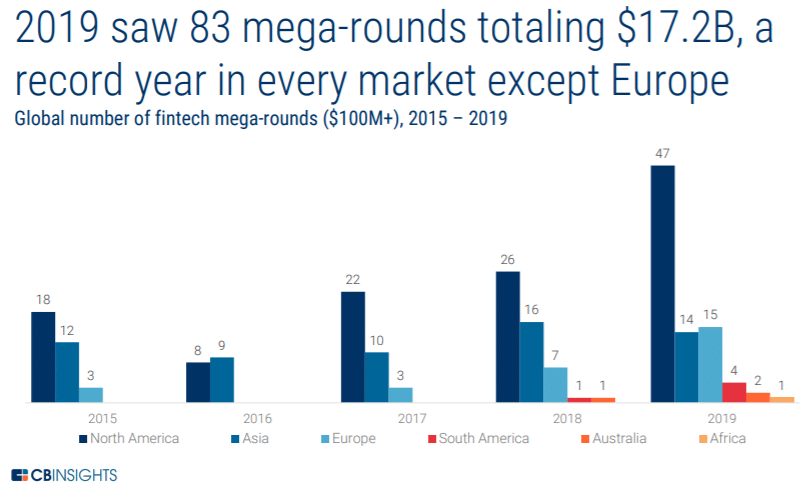

Indeed, another important funding trend that developed throughout 2019 is the proliferation of so-called "mega-rounds": fundraising rounds worth $100 million or more. Eighty-three--a record-breaking number of these rounds--were held throughout 2019.

This increase in mega-rounds also resulted in an increased number of "Unicorns" in the space: CB Insights' report said that by the end of 2019, there were "67 VC-backed fintech unicorns worth a combined $244.6B." The year also "saw a record of 24 unicorn births, 8 of which occurred in Q4'19."

Meet the world's #unicorn herd and get information on their investors, funding history, and more. Check out the complete Unicorn #Startup Market Map right here: https://t.co/gicTQbvt2X

Why did this happen? Mohammad Mazen, chief executive of crypto and blockchain advocacy firm Burency, explained to Finance Magnates that one reason for the increase in mega-rounds could be that in the short term-sense, funding begets funding: "when a company convinces a large investment fund, it opens doors with other investment funds," he said. "The bigger the financing, the bigger the valorization."

Mohammad Mazen, chief executive of crypto and blockchain advocacy firm Burency.

However, in the longer term, there is no guarantee of future success: Mr. Mazen explained that a number of fintech companies have lost their unicorn status over the last several years "mainly because of lower valuations following new funding rounds."

In other words, the performance of these heavily-funded companies and newly-birthed unicorns will have important consequences over the next two years. While the funding that was received during 2019 may have been impressive, these companies cannot rest on their laurels.

In the spirit of #failure, we dug into the data on #startup death and found that 70% of upstart tech companies fail — usually around 20 months after first raising financing. See what's behind the mortality rate in these 290+ startup post-mortems: https://t.co/1QkCtf7vgS

Sandeep Todi, however, still sees room for growth: for him, the presence of so many new unicorns in the space signifies that "the need for better financial and banking services has been proven."

"Consumers and businesses are ready for digital solutions and the current wave is only the beginning for larger disruption in financial services," Mr. Todi explained.

"[...] We will see larger disruptions happening in the B2B space, where the stakes are even higher and consumerization of banking and financial services has begun. The significance is that the future of money is changing. Accessibility and convenience are no longer 'nice to have', they're product table stakes."

Developing and emerging markets are quickly gaining traction

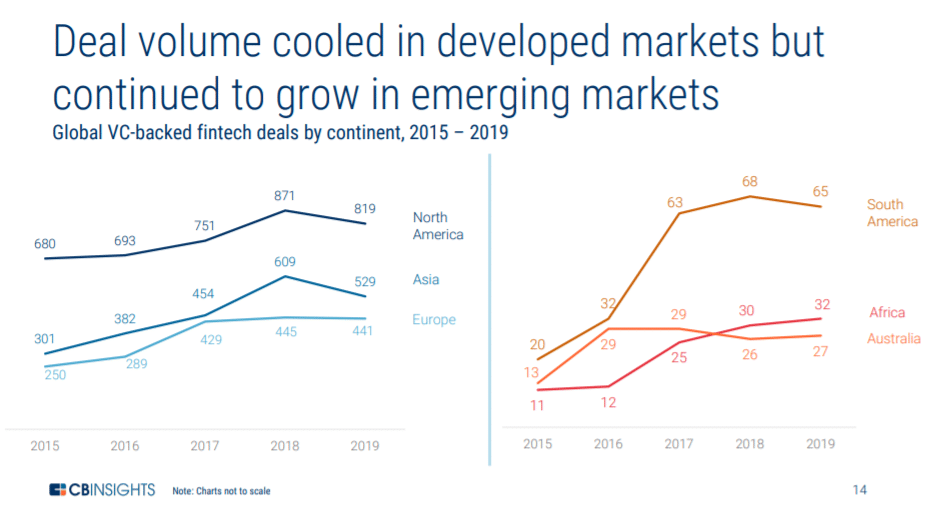

Business Insiderpointed out that another reason for the increase in mega-rounds could be the fact that "developing countries [are] increasingly enhancing their fintech ecosystems"--indeed, 2019 also saw the first time that a mega-funding round occurred on every populated continent, including--for the first time--Africa.

This kind of geographical proliferation can be counted as evidence that the growth of fintech is truly a global trend, rather than just being confined to countries like the United States and the United Kingdom.

Indeed, African fintechs raised $282.5 million in funding in 2019, up more than 150 percent from the $110.6 million raised in 2018. At the same time, South American fintech funding more than double from $552.8 million to $1.4 billion.

Asia also surpassed Europe in terms of capital raised and number of deals completed in the second half of the year: $1.8 billion was raised in 157 deals throughout Asia during Q3 of 2019, while European startups raised $1.6 billion through just 95 deals; in Q4, 100 fundraising rounds held by European startups raised just $1.2 billion, while Asian companies raised $2.14 billion was raised through 125 deals.

Specifically, Southeast Asia raised $993 million in 124 rounds throughout the year, making 2019 the region's best year yet.

Indeed, "the technological gap between developed and emerging countries is narrowing year by year," Mr. Mazen commented.

"These emerging countries now have much more resources than they did 10 years ago," including "access to business loans, the number of fast and secure internet servers, workforce, and other resources make it easier for them to innovate."

Indeed, the 1.7 billion "unbanked" individuals located throughout the developing world have been identified as a major source of profit for fintech companies. Businesses see an opportunity to provide mobile-based financial services to individuals in remote areas that brick-and-mortar financial institutions never bothered to invest in reaching.

Despite progress, there's still big potential for growth in developing markets

These emerging markets present a huge amount of potential for the fintech industry. Despite the progress that seems to have been made in 2019, "financial inclusion is still an [unsolved] problem," Sandeep Todi said, adding that the sheer extent of the problem "goes largely unrecognized."

Specifically, Mr. Todi cited a 2017 report by philanthropic investment firm Omidyar entitled "Innovating for the Next Half Billion".

"They reported that over 200 million people in India access the internet through mobile phones," Mr. Todi explained, which is "roughly five times more than than the Canadian population. This isn't a small problem."

"Fintech industry products are giving [these individuals] more access and control over their money,' he continued. Therefore, "the early gains of investing in frontier economies are obvious as early mover advantages accrue to investors and startups."

"As competition increases and the fintech ecosystem opens up due to open banking and other regulatory changes in developed economies, significant shifts will start emerging in these countries as newer opportunities become viable and scalable."

What do you think the most important fundraising trend in fintech was throughout 2019? What are your predictions for 2020? Let us know in the comments below.

Late last week, a new report from technology trend software firm CB Insights made a big splash on the fintech scene: the report, which focused on developments in the fintech industry throughout 2019.

The number most cited by the press was the total sum of fundraising by fintech companies throughout 2019: $34.5 billion.

On its face, it appeared as though there was a significant decrease in fintech funding from the prior year, which saw a sum of $40.8 billion in funding.

However (as the report pointed out), when we exclude Ant Financial's massive $14 billion round from 2018's sum, there is actually a significant increase between the two years: excluding Ant Financial, funding rose from $26.8 billion to $34.5 billion year-over-year, an increase of nearly 30 percent.

In other words, fintech is growing--and fast. But the industry has already started to evolve, with a greater focus on later-stage startups, consolidation, and developing markets.

A shift away from early-stage startups

A number of these trends that seem to suggest maturation in the fintech industry--a movement away from the creation of many singularly-focused startups, and toward supporting relatively more-established companies that are seeking to scale their businesses.

For example, there was an important shift in where this funding was being directed towards: in 2019, funding for early-stage startups reached a five-year low, while funding for later-stage startups hit a five-year high. Early-stage companies received $5.3 billion last year, down from $6.5 billion in 2018.

There were also fewer deals overall from 2018 to 2019; the total number of fundraising rounds decreased roughly 7 percent from 2049 to 1913.

Part of the reason for this particular decline was the fact that there were simply fewer fintech startup companies being launched. For example, only three new insurtech companies were launched in the first three quarters of last year, while 12 had been launched in 2018, and a whopping 109 had been launched in 2017.

Maturation and consolidation

In other words, the fintech industry seems to be trending toward consolidation: fewer companies and fewer funding rounds--but higher rewards for companies who have managed to prove themselves over the last two years.

This, of course, has been accompanied by more merging and acquisition activity: Sandeep Todi, co-founder and chief business officer at Remitr, told Finance Magnates that he has also seen a movement toward consolidation in fintech: "we're now at a place of clutter with too many singular solutions, which is why there's so much activity in acquisitions," he said.

Sandeep Todi, co-founder and chief business officer at Remitr.

For example, in the three months that have passed since the year began, "we've seen [mergers and acquisitions] like Lending Club's purchase of Radius, and Visa's [purchase of] Plaid," Mr. Todi explained. "The most recent is the [news that] Intuit is acquiring CreditKarma."

All of this represents an important shift in the way that the fintech industry is conceptualized: "the incumbents no longer see the value of fintech," Mr. Todi said; rather, "they know it, which is why we'll continue to see a 'rebundling' in financial technology."

As such, "these acquisitions point towards later stage fintechs reaching maturity, making a significant impact, and therefore attracting more investor attention and funding."

Activity in the fintech arena is drawing more and more companies into financial services

Therefore, Mr. Todi believes that this shift toward consolidation and industry maturity "bodes well for any fintech that has integration with other financial services in its DNA, thus giving it an inherent scale and ready to accept funding."

For example, this push toward fintech has manifested in the form of Google's checking accounts, which will allegedly be available sometime in the next year, and Apple's partnership with Goldman Sachs in 2018 to launch the Apple Card, which has now facilitated the lending of over $10 billion to users. In late 2018, Uber launched "Uber Cash," a feature that the company branded as "[allowing] you to plan ahead by adding funds upfront for a seamless payment experience across Uber's service."

In the longer term, this trend toward adding financial services could bring even more companies into the fintech arena. Peter R. Deans, creator and founder of Australian-based 52 Risks, explained to Finance Magnates that, therefore, "despite the drop in overall funding...we are continuing to see an increasing proliferation of fintech entrants in every market around the world."

Peter R. Deans, creator and founder of Australian-based 52 Risks.

Proliferation and discrimination

In addition to the scaling opportunities that fintech integration presents, Mr. Dean said that the trend toward fintech "reflects a number of factors."

Specifically, Mr. Deans named "continued strong in interest in fintech as a segment," and "market acceptance and traction of fintech offerings." Another important fueling factor to the fintech industry, however, is the fact that increasingly, "regulators [are] encouraging new entrants through more accommodating legislation and regulatory changes."

Mr. Deans pointed out that the forces pushing the proliferation of fintech may also be fueling discretion among investors: "there are a lot of investment opportunities and we are seeing angel, seed, and [venture capital] investors being somewhat more discriminating."

"In addition, financial services groups are becoming more adept at identifying the 'right' fintech firms to partner with but usually at a later stage."

A smaller number of fintech funding deals, but the average size of each deal increased from 2018

And when the "right" fintech firms are found--both by potential partners and investors--the cash starts to flow.

"I think both the VC investors and Financial Services firms investing in fintech firms are getting better at identifying the true disruptors," Peter Deans said, "and are directing larger amounts of money at getting these businesses scaled up quickly."

Indeed, another important funding trend that developed throughout 2019 is the proliferation of so-called "mega-rounds": fundraising rounds worth $100 million or more. Eighty-three--a record-breaking number of these rounds--were held throughout 2019.

This increase in mega-rounds also resulted in an increased number of "Unicorns" in the space: CB Insights' report said that by the end of 2019, there were "67 VC-backed fintech unicorns worth a combined $244.6B." The year also "saw a record of 24 unicorn births, 8 of which occurred in Q4'19."

Meet the world's #unicorn herd and get information on their investors, funding history, and more. Check out the complete Unicorn #Startup Market Map right here: https://t.co/gicTQbvt2X

Why did this happen? Mohammad Mazen, chief executive of crypto and blockchain advocacy firm Burency, explained to Finance Magnates that one reason for the increase in mega-rounds could be that in the short term-sense, funding begets funding: "when a company convinces a large investment fund, it opens doors with other investment funds," he said. "The bigger the financing, the bigger the valorization."

Mohammad Mazen, chief executive of crypto and blockchain advocacy firm Burency.

However, in the longer term, there is no guarantee of future success: Mr. Mazen explained that a number of fintech companies have lost their unicorn status over the last several years "mainly because of lower valuations following new funding rounds."

In other words, the performance of these heavily-funded companies and newly-birthed unicorns will have important consequences over the next two years. While the funding that was received during 2019 may have been impressive, these companies cannot rest on their laurels.

In the spirit of #failure, we dug into the data on #startup death and found that 70% of upstart tech companies fail — usually around 20 months after first raising financing. See what's behind the mortality rate in these 290+ startup post-mortems: https://t.co/1QkCtf7vgS

Sandeep Todi, however, still sees room for growth: for him, the presence of so many new unicorns in the space signifies that "the need for better financial and banking services has been proven."

"Consumers and businesses are ready for digital solutions and the current wave is only the beginning for larger disruption in financial services," Mr. Todi explained.

"[...] We will see larger disruptions happening in the B2B space, where the stakes are even higher and consumerization of banking and financial services has begun. The significance is that the future of money is changing. Accessibility and convenience are no longer 'nice to have', they're product table stakes."

Developing and emerging markets are quickly gaining traction

Business Insiderpointed out that another reason for the increase in mega-rounds could be the fact that "developing countries [are] increasingly enhancing their fintech ecosystems"--indeed, 2019 also saw the first time that a mega-funding round occurred on every populated continent, including--for the first time--Africa.

This kind of geographical proliferation can be counted as evidence that the growth of fintech is truly a global trend, rather than just being confined to countries like the United States and the United Kingdom.

Indeed, African fintechs raised $282.5 million in funding in 2019, up more than 150 percent from the $110.6 million raised in 2018. At the same time, South American fintech funding more than double from $552.8 million to $1.4 billion.

Asia also surpassed Europe in terms of capital raised and number of deals completed in the second half of the year: $1.8 billion was raised in 157 deals throughout Asia during Q3 of 2019, while European startups raised $1.6 billion through just 95 deals; in Q4, 100 fundraising rounds held by European startups raised just $1.2 billion, while Asian companies raised $2.14 billion was raised through 125 deals.

Specifically, Southeast Asia raised $993 million in 124 rounds throughout the year, making 2019 the region's best year yet.

Indeed, "the technological gap between developed and emerging countries is narrowing year by year," Mr. Mazen commented.

"These emerging countries now have much more resources than they did 10 years ago," including "access to business loans, the number of fast and secure internet servers, workforce, and other resources make it easier for them to innovate."

Indeed, the 1.7 billion "unbanked" individuals located throughout the developing world have been identified as a major source of profit for fintech companies. Businesses see an opportunity to provide mobile-based financial services to individuals in remote areas that brick-and-mortar financial institutions never bothered to invest in reaching.

Despite progress, there's still big potential for growth in developing markets

These emerging markets present a huge amount of potential for the fintech industry. Despite the progress that seems to have been made in 2019, "financial inclusion is still an [unsolved] problem," Sandeep Todi said, adding that the sheer extent of the problem "goes largely unrecognized."

Specifically, Mr. Todi cited a 2017 report by philanthropic investment firm Omidyar entitled "Innovating for the Next Half Billion".

"They reported that over 200 million people in India access the internet through mobile phones," Mr. Todi explained, which is "roughly five times more than than the Canadian population. This isn't a small problem."

"Fintech industry products are giving [these individuals] more access and control over their money,' he continued. Therefore, "the early gains of investing in frontier economies are obvious as early mover advantages accrue to investors and startups."

"As competition increases and the fintech ecosystem opens up due to open banking and other regulatory changes in developed economies, significant shifts will start emerging in these countries as newer opportunities become viable and scalable."

What do you think the most important fundraising trend in fintech was throughout 2019? What are your predictions for 2020? Let us know in the comments below.

Rachel is a self-taught crypto geek and a passionate writer. She believes in the power that the written word has to educate, connect and empower individuals to make positive and powerful financial choices. She is the Podcast Host and a Cryptocurrency Editor at Finance Magnates.

ESMA Didn’t Say How Lithuania’s Cross-Border Clients Jumped 5,000x. Is It Because of Revolut?

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.