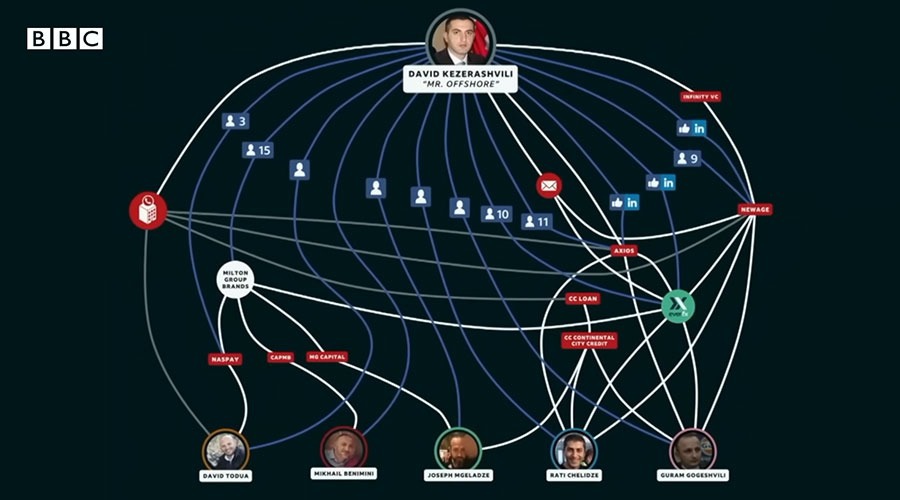

The recent BBC expose on the ripples of the Milton Group Scandal, which involve mass fraud of trading scams especially of the elderly, has set the UK media into a frenzy. The scamming network has allegedly robbed elderly people, not just, via boiler room scams, but via cryptocurrencies and FIAT currencies, in a worldwide attempt for unjust enrichment. Yet, this is not the first time that fraud has popped up in the EU, UK or other states such as Israel. The Milton scandal surfaced in 2020, and since then the same operatives have continued with their daily illegal business as if nothing has changed.

This has led many consumers and international regulators to scrutinize the Member State regulators to see whether the liability of non-detection falls upon the central banks. This also leads to the question, who are the central banks accountable to? The public or their own respective regulators?

Last week, we witnessed the approval of MiCA, the Markets in Crypto Assets Regulation of the EU by the European Parliament, which means that finally, some of the uncertainty when it comes to crypto assets will be resolved on a pan-European level. With that said, the majority of crypto fraud that has taken place during the past few years has stemmed from unregulated CFD trading platforms that have evolved from binary options schemes. A significant watchful eye and criticism have been placed upon regulators worldwide that have not sufficiently tackled these issues.

Central banks and financial intelligence units (FIUs), which are in charge of licensing trading platforms and crypto exchanges, have been scrutinized not just by the European Securities and Markets Agency (ESMA) but by consumers that were targeted by CFD boiler rooms and other crypto-forex fraud. This leads to the question of accountability and traceability by regulators.

The compliance teams that form the licensing and inspection of the licenses are caught in a severe case of Catch-22. On the one hand, the compliance teams need to examine an infinite amount of data submitted to the regulator, without an option to screen or detect unusual or suspicious transactions due to the high volume of material submitted. This issue was raised by the Estonian FIU back in August 2020 when the amount of fraudulent crypto exchanges surpassed the amount of legitimate financial institutions, and, as such, the Estonian FIU decided to cancel the majority of licenses and increased the regulatory threshold to an alarming degree.

Yet, this is not the response many have wished for. The consumers of the platforms and the international regulators (not on a Member State level) are under the impression that sufficient safeguards were not taken. Hence, the issue of digitalization of the AML process has become a much-needed resource of FIUs. In cases where the FIU were stuck with the detection of anomalies in the AML quarterly reports by the financial institutions, it was presumed that the FIUs will at least try and find a solution, and not a post-mortem one, that will enable any sort of detection of fraudulent activity from FIAT currency to cryptocurrency and vice versa.

This is the same case for liquidity providers and for market makers, who have been highlighted for money laundering and terrorist financing cases. A similar argument was raised by the Egmont Group in their last meeting and in the FATF Recommendations and has been highlighted by the recent updates to the EBA Recommendations.

Thus, the recent scandals, the recommendations of the international organizations and the market conditions all lead to the inescapable conclusion that there is an inherent need for AML AI technologies to solve the overload on the regulators and their respective compliance teams as well as to minimize the amount of duress on the regulators.

Just as much as the binary options schemes have evolved into CFD frauds, which in turn evolved into crypto liquidity frauds, the criticism pouring over the regulators' heads may be solved by implementing the correct AML AI technology that should detect the problematic transactions, prior to the approval of the quarterly or yearly license, and not in retrospect.

Technologies are now available in the market, yet regulators are hesitant to involve private companies' technology, white-labeled or not. This approach should change, mainly because it is not humanly possible to assess the amount of regulatory material received. Regulators may be of the impression that they are accountable to their respective states only. Yet, in today’s market, regulators are accountable to their respective end-clients, the financial institution’s clients who are left at the mercy of the financial institution.