After years of regulating crypto largely through lawsuits and overlapping agency claims, the United States has finally moved closer to a formal market structure framework.

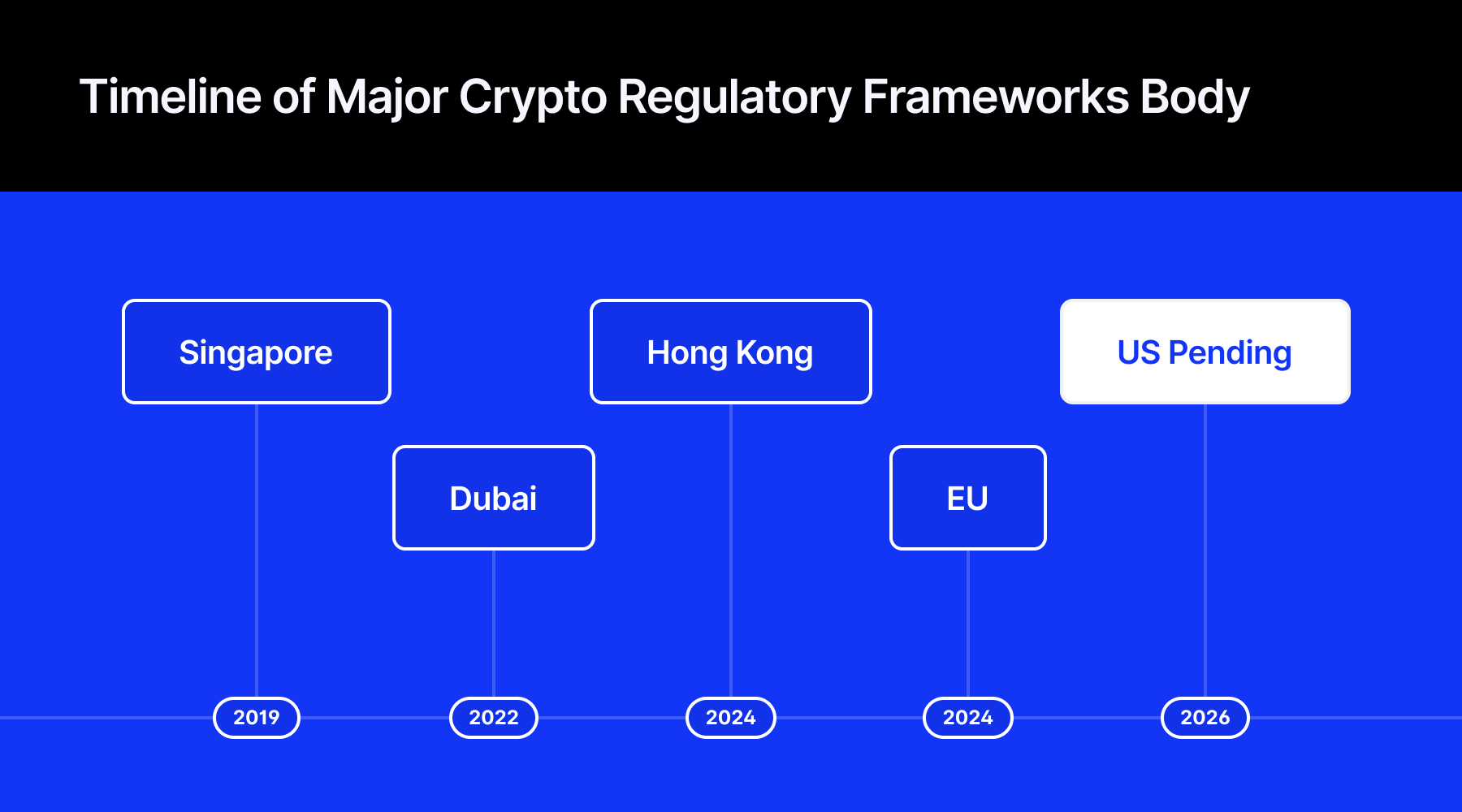

Should the CLARITY Act pass the Senate and be signed into law, the US would join jurisdictions such as the European Union, Singapore, the UAE, and Hong Kong, all of which already operate under dedicated crypto regulatory regimes.

Read our full explainer for a detailed breakdown of the CLARITY Act and how it could reshape US crypto regulation.

But while the legislation would represent the biggest shift in US crypto policy in years, the comparison also shows how much ground Washington still needs to cover before it reaches the level of operational clarity already seen elsewhere.

Senator Cynthia Lummis called the committee vote “a historic step forward for digital asset innovation,” arguing that the markup sent “an unmistakable signal that the United States is not ceding the future of digital finance to anyone.”

One small step for the Clarity Act and one giant leap for digital assets 🚀 pic.twitter.com/g9rk9A6nNX

— Senator Cynthia Lummis (@SenLummis) May 14, 2026

What’s at Stake for Exchanges and Institutional Firms

For exchanges such as Coinbase, Kraken, and Robinhood, the biggest advantage of CLARITY would be a clearer federal framework for crypto spot markets. Institutional firms, including ETF issuers, custodians, broker-dealers, and banks, could also gain more certainty around which assets fall under securities regulation and which would instead be treated as digital commodities.

Coinbase CEO Brian Armstrong described the committee-approved version as a “big improvement” from earlier drafts, particularly around stablecoin rewards, tokenization, DeFi, and CFTC authority.

The crypto market structure bill has PASSED the Senate Banking Committee with a bi-partisan vote!

— Brian Armstrong (@brian_armstrong) May 14, 2026

Historic day for crypto and for the future of digital assets in America. Grateful for the countless hours from lawmakers and staff to strengthen this legislation. Big improvement…

At the same time, the comparison with MiCA, MAS, VARA, and Hong Kong's regime shows that regulatory clarity alone is no longer enough. Other jurisdictions already operate mature licensing systems with established custody rules, stablecoin frameworks, and enforcement practices.

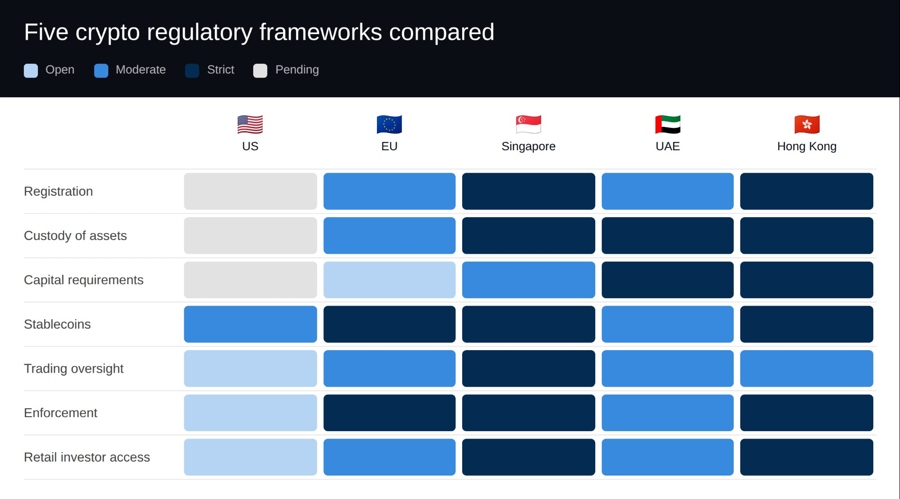

How the US Crypto Framework Compares Globally

The breakdown below compares seven regulatory dimensions across the US, EU, Singapore, UAE, and Hong Kong. Where the US framework is still pending, cells are marked accordingly.

Registration

How firms gain the legal right to operate is the most basic test of any regulatory framework, and the biggest dividing line between the US and its peers.

- US (CLARITY Act): Crypto firms would register with the CFTC under one of three categories: exchange, broker, or dealer. The SEC would retain authority over certain token offerings classified as securities. The framework is not yet in force and would require additional joint SEC-CFTC rulemaking after Senate approval.

- EU (MiCA): Crypto firms must obtain authorization from a national regulator in one EU member state. That license can then be passported across the entire EU market. Companies must establish a legal entity inside the EU. The full MiCA regime has been operational since December 2024.

- Singapore (MAS): Crypto firms must obtain a license from MAS under the Payment Services Act. Singapore applies one of the strictest licensing regimes globally, with limited transitional relief and close AML supervision. The regime has been in force since 2019 and tightened further in 2025.

- UAE (VARA): Crypto firms must obtain separate VARA licenses for each activity type, including trading, custody, brokerage, and advisory services. Dubai launched VARA in 2022 and expanded the framework nationwide through federal coordination in 2024.

- Hong Kong (SFC): All crypto trading platforms must be licensed by the SFC. Firms must establish a Hong Kong entity, appoint approved Responsible Officers, and complete an independent external assessment during the licensing process. Hong Kong's current VATP regime became fully mandatory in 2024.

Custody of Client Assets

Keeping customer money safe is the foundational obligation of any financial intermediary. Across all five jurisdictions, the rules point in the same direction, but the specifics vary considerably.

- US (CLARITY Act): Client assets must be held by a qualified custodian and kept strictly separate from firm funds. Co-mingling is prohibited. Custodian qualification standards are not yet finalized.

- EU (MiCA): Client assets must be kept strictly separate from firm assets and cannot be used for company purposes. Firms must comply with operational security and cybersecurity standards under ESMA guidance.

- Singapore (MAS): Segregation of client assets is mandatory. MAS requires monthly independent checks and annual audits of custody arrangements. Platforms may not use customer assets for lending or staking activities.

- UAE (VARA): Each client's assets must be held in a separate wallet, and mixing client and firm funds is prohibited. Firms must comply with formal cybersecurity and cryptographic key-management standards.

- Hong Kong (SFC): Custody must be handled by the platform's wholly owned subsidiary rather than a third-party provider. At least 98% of client assets must be held in cold storage, with the remaining assets fully insured.

Bitget CEO Gracy Chen said delays in US market structure legislation would likely prolong uncertainty around licensing, custody, and trading infrastructure. These are the areas where other jurisdictions already operate under fully implemented frameworks. If the bill is moved forward, regulated cryptocurrency activity in the US may increase dramatically due to stronger institutional adoption.

Capital Requirements

Minimum capital rules determine who can realistically enter a market. They signal how seriously a regulator treats the risk of firm failure. The US is the only jurisdiction here that has not yet set a number.

- US (CLARITY Act): The law directs the CFTC and SEC to set minimum capital thresholds, but no specific figures have been published. Not yet in force.

- EU (MiCA): Tiered by service type — €50,000 for advisory, €125,000 for custody or exchange services, €150,000 for a trading platform. Stablecoin issuers face higher thresholds.

- Singapore (MAS): Minimum capital starts at S$250,000 for licensed platforms. Stablecoin issuers must maintain at least S$1,000,000 and meet additional reserve and solvency requirements under MAS supervision.

- UAE (VARA): Tiered by activity — AED 100,000 for advisory, AED 600,000–1,000,000 for broker-dealers, AED 4,000,000 for custody, AED 5,000,000 for exchanges. Firms must also hold 3–6 months of operating costs in liquid reserves.

- Hong Kong (SFC): Paid-up capital of HK$5M for dealing or HK$10M for custody. Firms must also maintain liquid assets covering 12 months of operating expenses.

Stablecoins

Stablecoins have become one of the most closely watched areas of crypto regulation globally. All five jurisdictions now have rules in place, and the differences are narrowing fast.

- US (CLARITY Act / GENIUS Act): Stablecoins must maintain 1:1 reserves backed by cash, Treasuries, or deposits, with monthly public reserve disclosures. Algorithmic stablecoins are prohibited. Foreign issuers must pass a regulatory comparability test before operating in the US market.

- EU (MiCA): Stablecoins require prior authorization, 1:1 liquid reserves, and regular audits. Large issuers are supervised directly by the EBA. Algorithmic stablecoins are effectively prohibited, and non-compliant tokens have already been delisted by some EU platforms.

- Singapore (MAS): Stablecoins pegged to SGD or G10 currencies must be fully reserve-backed and redeemable within five business days. MAS grants a special "MAS-Regulated Stablecoin" designation to compliant issuers. Algorithmic stablecoins do not qualify under the framework.

- UAE (VARA): AED-backed stablecoins are permitted for payments. Foreign stablecoins such as USDC are limited to licensed trading platforms and cannot be used in retail shops. Algorithmic stablecoins and privacy tokens are banned.

- Hong Kong (SFC / HKMA): Stablecoin issuers must obtain an HKMA license and meet minimum capital requirements. Only licensed stablecoins may be offered to retail investors, while algorithmic stablecoins are not eligible for approval.

Banking groups remain concerned that some stablecoin provisions could blur the line between crypto products and traditional deposits. In a joint statement following the committee vote, major US banking associations warned that “without the necessary guardrails, stablecoin offerings are expected to draw away bank deposits and threaten local lending and economic activity across the country.”

Trading Oversight

Who watches the markets, and whether that responsibility is shared between agencies shapes how consistently rules are applied in practice.

- US (CLARITY Act): The CFTC oversees spot crypto markets; the SEC retains anti-fraud authority on its own platforms. Derivatives remain with the CFTC. A formal inter-agency coordination agreement is still pending.

- EU (MiCA): National regulators supervise platforms in their home country; ESMA coordinates cross-border oversight. Crypto derivatives remain governed by MiFID II.

- Singapore (MAS): MAS oversees all crypto activity — both spot and derivatives — with no split between agencies, making it one of the most unified regulatory frameworks globally.

- UAE (VARA): VARA regulates spot trading in Dubai. Platforms in the DIFC financial district fall under the DFSA. Since August 2025, VARA and the national regulator CMA mutually recognize each other's licenses.

- Hong Kong (SFC): The SFC oversees both spot trading platforms and crypto derivatives under separate licensing regimes. The HKMA has concurrent oversight where platforms interact with banking infrastructure.

Enforcement

Rules matter only as much as the willingness to enforce them. The gap between jurisdictions here is arguably wider than anywhere else in the comparison.

- US (CLARITY Act): No enforcement exists under the CLARITY framework yet because the law is still pending. Before 2025, the SEC pursued aggressive litigation against firms including Ripple, Coinbase, Binance, and Kraken. Since 2025, the federal tone has shifted toward a more industry-friendly approach.

- EU (MiCA): Enforcement has accelerated rapidly since MiCA took effect, with €540M+ in fines and 50+ license revocations reported through 2025. Operating without authorization can trigger penalties of up to 5% of annual turnover.

- Singapore (MAS): MAS applies a selective but strict enforcement approach focused heavily on AML compliance, licensing standards, and consumer protection. Firms failing licensing or compliance requirements face rapid shutdown orders with limited regulatory tolerance.

- UAE (VARA): VARA has become increasingly assertive, issuing 36 enforcement notices between August 2024 and August 2025. Financial penalties reached up to AED 600,000, while cease-and-desist orders have been used against unlicensed operators.

- Hong Kong (SFC): Operating without a license became a criminal offense in 2024. Following the 2023 JPEX fraud scandal, Hong Kong significantly tightened enforcement against unlicensed platforms and expanded investor-protection oversight.

Retail Investor Access

How much protection or restriction ordinary investors face is one of the sharpest points of divergence across the five frameworks.

- US (CLARITY Act): No formal suitability tests or retail restrictions exist for spot crypto under the proposed law. The GENIUS Act gives all stablecoin holders the right to redeem at any time.

- EU (MiCA): Retail access is open on licensed platforms. Risk warnings are mandatory in all marketing materials. Suitability assessments are required for complex products. Leverage may be restricted under national rules.

- Singapore (MAS): Retail investors must pass a mandatory Risk Awareness Quiz before they can trade. Lending or staking of client assets is prohibited. Crypto advertising in public spaces such as ATMs and bus stops is banned.

- UAE (VARA): Retail trading is permitted with mandatory risk disclosures and suitability checks. Foreign stablecoins cannot be used for everyday payments. FOMO-based advertising and influencer promotions are strictly regulated.

- Hong Kong (SFC): Retail investors can only trade large-cap tokens with a minimum 12-month track record. Only HKMA-licensed stablecoins are eligible for retail. Margin trading and lending of client assets are prohibited.

Key Takeaways

The comparison points to several patterns that go beyond any single jurisdiction: how frameworks are structured, where rules are tightening, and where the biggest gaps remain.

Global Crypto Regulation Is Starting to Converge

Despite major political and regulatory differences, the five frameworks are beginning to converge around the same core principles. Every jurisdiction covered in the comparison now requires some combination of licensing for crypto intermediaries, segregation of customer assets, reserve backing for stablecoins, and formal anti-money-laundering controls.

Asheesh Birla, CEO of Evernorth, argued that the longer the US delays building a formal framework, the more crypto infrastructure shifts offshore.

81% of crypto developers now work outside the US. 58% of crypto hedge funds are domiciled in the Caymans.

— Asheesh Birla | CEO at Evernorth (@ashgoblue) May 14, 2026

That isn't a regulatory victory. It's a transfer of authority.

The CLARITY Act is the most credible effort yet to bring on-chain finance home. My take:…

Algorithmic stablecoins also face either outright bans or practical exclusion across nearly all major regimes. The differences increasingly come down to retail access and enforcement rules.

Singapore focuses heavily on consumer protection, the EU prioritizes passporting and harmonization, Dubai emphasizes activity-based licensing, while the US still relies on a split SEC-CFTC structure that remains unfinished.

For the industry, that marks a broader shift away from the early “wild west” phase of crypto markets toward something that increasingly resembles traditional financial regulation.

Questions around compliance infrastructure, identity verification, and institutional adoption are also becoming increasingly central to the debate around crypto regulation and financial integration.

- What Is the CLARITY Act? The US Crypto Bill That Could Reshape Digital Asset Regulation This Week

- Clarity Without Complacency: Why the SEC-CFTC Framework Is a Start, Not a Finish Line

Europe Has the Most Complete Framework in Force

Among the jurisdictions compared, MiCA remains the most comprehensive live crypto framework. The EU combines licensing, passporting rights, stablecoin supervision, capital requirements, custody rules, and enforcement powers inside a single cross-border regime.

Once licensed in one member state, a crypto company can operate across the EU. That level of harmonization still does not exist in the United States, where state licensing rules would continue alongside federal oversight even after CLARITY.

But the framework is also beginning to reshape the structure of the European crypto market itself. In May 2026, the European Commission reopened MiCA for formal review to assess its market impact ahead of the July 1 deadline ending transitional treatment for pre-MiCA operators.

Industry estimates cited by Finance Magnates suggest that only a fraction of previously active crypto firms have secured MiCA authorization so far, pointing to growing consolidation pressure across the sector.

MiCA’s stablecoin provisions are also already reshaping the EU crypto landscape. Several major exchanges, including Kraken and Coinbase, have restricted USDT access for EU users following the bloc’s tighter reserve and authorization requirements.

Singapore Is the Strictest on Retail Access

Singapore’s framework is notable for how aggressively it separates institutional innovation from retail speculation. Retail users must pass risk-awareness tests before trading, public crypto advertising is heavily restricted, and platforms are prohibited from lending or staking customer assets.

That contrasts sharply with the proposed US framework, which contains few formal retail suitability restrictions for spot crypto trading.

Dubai Focuses on Flexible, Activity-Based Licensing

VARA stands out for its highly granular licensing model. Instead of a single umbrella approval, firms must obtain separate licenses for activities such as custody, brokerage, trading, lending, and advisory services.

Dubai has also positioned itself as comparatively business-friendly while simultaneously increasing enforcement activity against unlicensed firms. The result is a framework many crypto companies view as commercially flexible, even if the broader regulatory structure remains complex.

The regime continues attracting large international players. In May 2026, Kraken parent Payward received preliminary authorization from VARA to operate as a virtual-asset broker-dealer and investment platform in the UAE. The move expanded Kraken’s regional footprint across spot trading, OTC services, staking, and institutional products.

Kraken is now authorized by VARA in Dubai.

— Kraken (@krakenfx) May 21, 2026

Authorization covers spot, margin, OTC, staking, and institutional access through Kraken Prime.$AED funding follows later this year.

Full details: https://t.co/EUChz8IOQo

Crypto Is Increasingly Being Treated Like Traditional Finance

A few years ago, the global debate around crypto regulation centered on whether governments would regulate the industry at all. The comparison now shows that the debate has largely moved beyond that point.

The major jurisdictions are building versions of financial market infrastructure with supervision, licensing, disclosure obligations, consumer protections, and stablecoin controls increasingly resembling traditional finance.

The debate now centers on how crypto should fit into the broader financial system and how strict that integration should become.