A year ago today, one of the most dramatic moments in crypto's history set a chain of events into action.

FM

It has officially been a year.

A year of the 'new norm'. A year of quarantining, of remote work, N19 masks, and social distancing. For many, a year of financial stress, mental health challenges, a year of loss. One year of COVID-19.

While the exact dates that quarantines began in the western world vary from country to country, this week marks the week when the whole world became serious about the coronavirus. Europe and North America had been watching reports on the spread of COVID from China and other parts of Asia for weeks; the World Health Organization (WHO) was warning that a global pandemic may be imminent.

Then, on Friday, March 13th, 2020, US President Donald Trump declared a state of emergency in the country; the same day, World Health Organization officials declared that Europe had become the new epicentre of the COVID-19 pandemic.

In the days leading up to the declarations, financial market crashes, the likes of which have not been seen in over a decade, began to wreak havoc on capital markets around the globe. Oil prices turned negative; the Dow Jones Industrial Average (DJIA) plunged 6,400 points, roughly 26% in just four trading days.

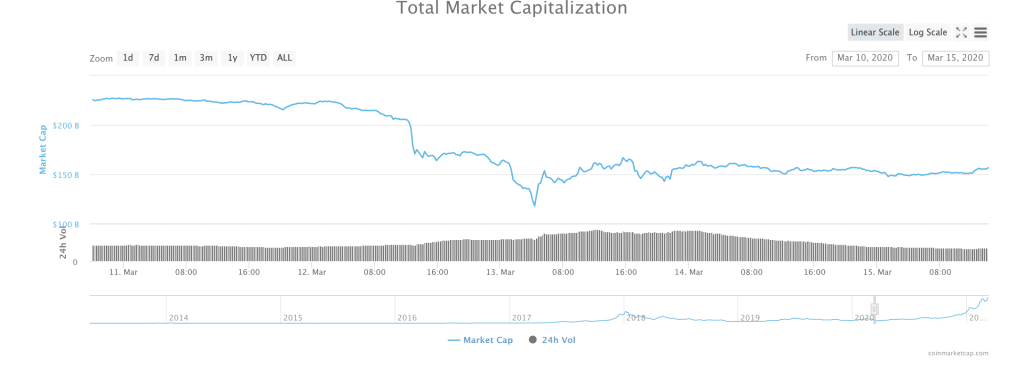

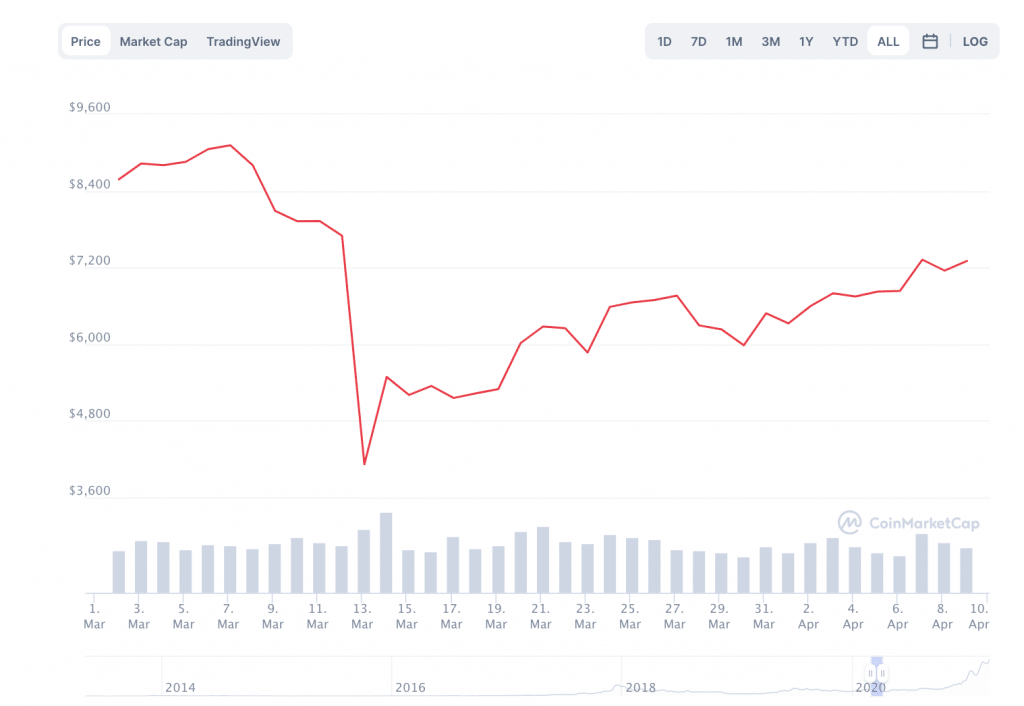

One of the starkest crashes hit the cryptocurrency markets. On the second Thursday in March 2020, the price of Bitcoin fell nearly 40 percent, crashing from nearly $8000 to around $4,700 in a matter of hours. Simultaneously, crypto’s total market cap lost approximately $30 billion, also dropping a total of 40 percent.

Today, March 11th is the second Thursday in March 2021, one year since the day that eventually came to be known as 'Crypto’s Black Thursday'.

When the crash occurred on March 12th, Bloombergcompared the price drop to the bursting of the crypto bubble in late 2017. In addition, a number of crypto critics said that the moment was proof that Bitcoin was not, in fact, the 'safe haven', 'hedge against inflation' asset that so many Bitcoin 'believers' said that it was.

On March 12th, 2020, renowned Bitcoin bear and Founder of EuroPacific Capital, Peter Schiff told Kitco News that Bitcoin is “not a safe haven asset. It is a very risky asset. The price of bitcoin has collapsed by more than the stock market during the last several weeks and in fact, it's not even a non-correlated asset.”

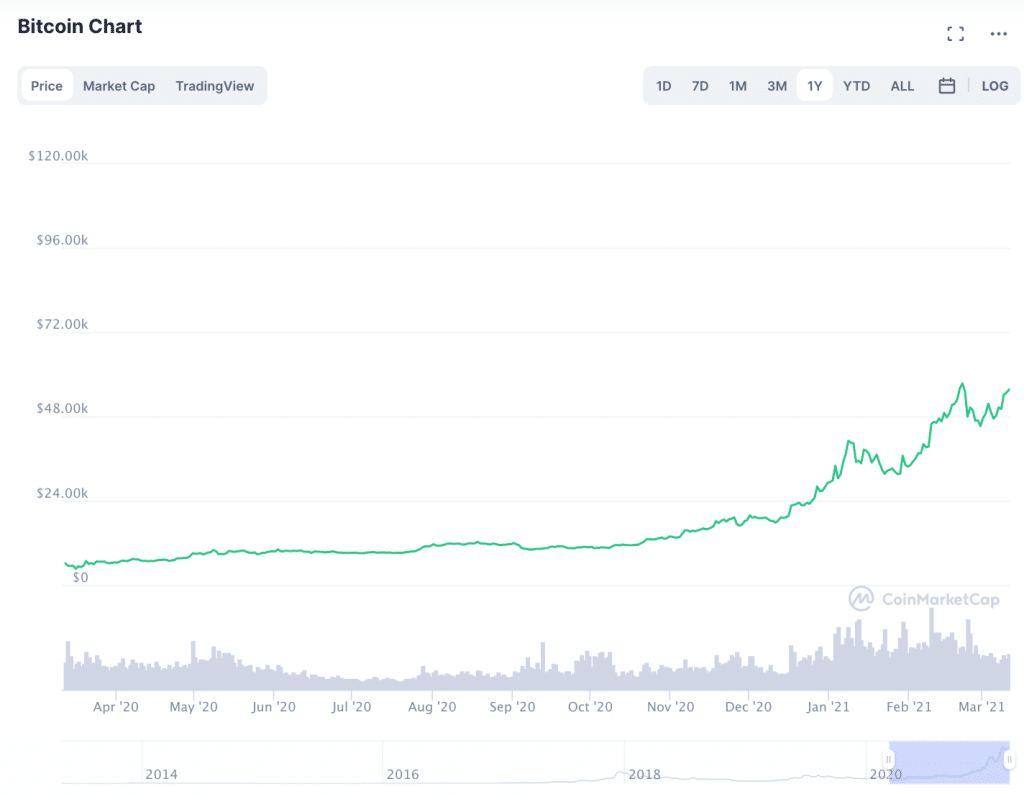

However, while Black Thursday may have cast doubt on Bitcoin’s long-term viability, BTC quickly made a remarkable comeback. By May of 2020, BTC was back up to nearly $10K a pop and maintained levels above $8K for the rest of the year. Today, the price of a single BTC is nearly $55,000, which is a rise of more than 1000 percent.

What Happened on Crypto’s Black Thursday?

Do Kwon, Co-Founder and CEO of Terraform Labs (TFL), explained that the primary factor that drove financial markets to crash across the board last March was fear.

“March 12th, 2020 was when the S&P 500 and markets around the world crashed from the fear and economic chaos induced by COVID-19,” Kwon told Finance Magnates.

However, Steve Ehrlich, Chief Executive of Voyager Digital, explained that while Black Thursday was certainly a moment of reckoning for Bitcoin, it may have also marked a pivot point for the future of the digital economy.

Steve Ehrlich, Chief Executive Officer and Co-founder of crypto trading platform, Voyager.

“As real clarity around the implications of the pandemic set-in, it became apparent that lockdowns would go into effect, the digital economy would become quintessential, and that economic stimulus would become necessary to keep the economy afloat,” he told Finance Magnates.

Doug Schwenk, Chairman of Digital Asset Research, told Finance Magnates that the Black Thursday Crash had an important psychological effect on crypto markets.

“[Black Thursday] has provided, in a sense, a psychological floor to build on,” Schwenk told Finance Magnates. “The shock and uncertainty of that moment led markets to regroup… and lowered volatility.” This momentum to rebuild initially consolidated “around $10k for BTC and then pushed higher as continued positive or clarifying news brought buyers into crypto markets.”

After Black Thursday, ”Bitcoin Reached an Inflection Point of Adoption from Institutions."

Beyond the effects of fear and doubt, the market crash that took place in March of 2020 led to important changes in monetary policy that have had profound effects on the price of Bitcoin.

“Over the course of 2020, a deluge of fiscal stimulus helped contribute to Bitcoin’s store-of-value or ‘digital gold’ narrative that increased awareness of its long-term potential.”

After Black Thursday, “what followed was months of news of the U.S. Government printing trillions of dollars to stimulate the economy and provide economic relief. In fact, 20% of all dollars ever printed since the origins of the U.S. Dollar were printed in 2020,” Kwon explained.

“This massive influx of U.S. dollars into the economy at a rapidly increasing velocity due to lower interest rates, left investors rushing to find the best place to invest their dollars to combat inflation.”

This is what led a growing number of institutional investors into BTC. “Bitcoin, being a scarce digital asset, with a strict 21-million hard cap supply, and its rapid rate of adoption led Bitcoin’s value to sky-rocket and continue hitting all-time highs, far surpassing its previous 2017 peak,” Kwon explained.

Do Kwon, Co-Founder, and CEO of Terraform Labs (TFL).

“[...] Bitcoin reached an inflexion point of adoption from institutions, who began pouring in money as a long-term hedge against inflation. With the halving occurring in May 2020 after the crash, the supply of Bitcoin issued by the protocol was reduced by 50 percent, which also reduced the liquid supply available to the market, making BTC more scarce.”

Marie Tatibouet, Chief Marketing Officer at Gate.io, told Finance Magnates that this scarcity is making Bitcoin increasingly attractive to large investors. “Every company now wants to dedicate their balance sheet to Bitcoin,” she said.

“Microstrategy, Tesla, Square, Ruffers, and others have all gone in on Bitcoin. Other Fortune 500 companies will probably follow suit and buy chunks of Bitcoin, as well. Now, even Ethereum has become a major investment option, with companies like Meitubuying $22M worth of ETH.”

Retail Investors Also Came for Crypto Markets in 2020

But, it was not just institutional investors that came in droves for cryptocurrency in 2020. Steve Ehrlich, Chief Executive of Voyager Digital, explained to Finance Magnates that: “as people across the world were restricted to their homes, many small businesses had to reduce their operations, retail investors were looking for new avenues to invest and trade for supplemental income - causing a surge into cryptocurrency investing.”

Ehlrich says that similar to institutional investors, retail investors in Bitcoin began to see BTC as a hedge against inflation. Verdictreported in January 2021 that retail investors who put their government stimulus checks into BTC were one of the driving factors behind Bitcoin’s massive price increase. Notably, investors who put their first $1400 stimulus check into Bitcoin now have approximately $9000 in BTC.

“These retail investors also see the world becoming more digital, and the digital gold narrative of Bitcoin has never been stronger,” Steve Ehrlich said.

Marie Tatibouet, Chief Marketing Officer at Gate.io.

“In order for Bitcoin to reach a market cap similar to gold, it will have to hit an $11 trillion dollar market cap. Bitcoin now hovers around a $1 trillion dollar market cap, as it continues to gobble up Global liquidity. And, many Bitcoin enthusiasts believe BTC surpassing Gold’s market cap is only a matter of time,” Ehrlich said.

A “Wave of Positive Regulatory Events” Acted as a Boon for Bitcoin

Digital Asset Research’s Doug Scwhenk pointed out that in addition to monetary policy changes and an increasing pool of BTC buyers, crypto has been positively affected by “a wave of positive regulatory events that give institutional investors comfort.”

For example, “the new US administration has nominated a chair of the SEC with prior crypto experience, ETF's have launched in Canada and Bermuda, and the OCC clarified banks can hold these assets.”

Additionally, "storied institutions such as Bank of New York Mellon and Northern Trust have declared public plans and offerings in the space. All of this has served as tremendous tailwinds after an initial shock and great unknown about how our lives would be affected by COVID.”

A New Financial Paradigm in 2022?

If these positive regulatory trends continue in 2022, Bitcoin’s explosive growth could continue. Now that it has been twelve months since Black Thursday, what could crypto markets look like twelve months in the future?

Do Kwon said that while, “it’s impossible to know,” what the future will hold, “at the current rate, it wouldn’t be surprising if we begin to see accelerated adoption of Bitcoin and DeFi by more mainstream investors.”

“Better UX, more capital, better infrastructure, and broader awareness are all ingredients for onboarding more users to a new financial system, one that is more inclusive and open,” Kwon said.

Though it might not arrive in 2022, Steve Ehrlich sees a financial paradigm shift in the future. “More than just a new monetary technology, Bitcoin is an entirely new economic paradigm: an uncompromisable base money protocol for a global, digital, non-state economy,” he said. “It promises to mark the separation of money and state.”

“Bitcoin presents us with an opportunity to reinvent gold and rethink money for the digital future in a more globalized, internet-native way. For those, and many more reasons, Bitcoin and cryptocurrency will continue to enjoy progress and pursuit of a new economic reality.”

Therefore, Bitcoin could reach unprecedented levels in the twelve months ahead: “originally, the idea of a $100,000 Bitcoin seemed like a complete stretch of the imagination, but has now become like a seemingly reasonable target for the rising digital asset,” he said.

“We see cryptocurrency and digital assets going completely mainstream, disrupting traditional financial institutions, and giving economic empowerment to people all over the world in need.”

It has officially been a year.

A year of the 'new norm'. A year of quarantining, of remote work, N19 masks, and social distancing. For many, a year of financial stress, mental health challenges, a year of loss. One year of COVID-19.

While the exact dates that quarantines began in the western world vary from country to country, this week marks the week when the whole world became serious about the coronavirus. Europe and North America had been watching reports on the spread of COVID from China and other parts of Asia for weeks; the World Health Organization (WHO) was warning that a global pandemic may be imminent.

Then, on Friday, March 13th, 2020, US President Donald Trump declared a state of emergency in the country; the same day, World Health Organization officials declared that Europe had become the new epicentre of the COVID-19 pandemic.

In the days leading up to the declarations, financial market crashes, the likes of which have not been seen in over a decade, began to wreak havoc on capital markets around the globe. Oil prices turned negative; the Dow Jones Industrial Average (DJIA) plunged 6,400 points, roughly 26% in just four trading days.

One of the starkest crashes hit the cryptocurrency markets. On the second Thursday in March 2020, the price of Bitcoin fell nearly 40 percent, crashing from nearly $8000 to around $4,700 in a matter of hours. Simultaneously, crypto’s total market cap lost approximately $30 billion, also dropping a total of 40 percent.

Today, March 11th is the second Thursday in March 2021, one year since the day that eventually came to be known as 'Crypto’s Black Thursday'.

When the crash occurred on March 12th, Bloombergcompared the price drop to the bursting of the crypto bubble in late 2017. In addition, a number of crypto critics said that the moment was proof that Bitcoin was not, in fact, the 'safe haven', 'hedge against inflation' asset that so many Bitcoin 'believers' said that it was.

On March 12th, 2020, renowned Bitcoin bear and Founder of EuroPacific Capital, Peter Schiff told Kitco News that Bitcoin is “not a safe haven asset. It is a very risky asset. The price of bitcoin has collapsed by more than the stock market during the last several weeks and in fact, it's not even a non-correlated asset.”

However, while Black Thursday may have cast doubt on Bitcoin’s long-term viability, BTC quickly made a remarkable comeback. By May of 2020, BTC was back up to nearly $10K a pop and maintained levels above $8K for the rest of the year. Today, the price of a single BTC is nearly $55,000, which is a rise of more than 1000 percent.

What Happened on Crypto’s Black Thursday?

Do Kwon, Co-Founder and CEO of Terraform Labs (TFL), explained that the primary factor that drove financial markets to crash across the board last March was fear.

“March 12th, 2020 was when the S&P 500 and markets around the world crashed from the fear and economic chaos induced by COVID-19,” Kwon told Finance Magnates.

However, Steve Ehrlich, Chief Executive of Voyager Digital, explained that while Black Thursday was certainly a moment of reckoning for Bitcoin, it may have also marked a pivot point for the future of the digital economy.

Steve Ehrlich, Chief Executive Officer and Co-founder of crypto trading platform, Voyager.

“As real clarity around the implications of the pandemic set-in, it became apparent that lockdowns would go into effect, the digital economy would become quintessential, and that economic stimulus would become necessary to keep the economy afloat,” he told Finance Magnates.

Doug Schwenk, Chairman of Digital Asset Research, told Finance Magnates that the Black Thursday Crash had an important psychological effect on crypto markets.

“[Black Thursday] has provided, in a sense, a psychological floor to build on,” Schwenk told Finance Magnates. “The shock and uncertainty of that moment led markets to regroup… and lowered volatility.” This momentum to rebuild initially consolidated “around $10k for BTC and then pushed higher as continued positive or clarifying news brought buyers into crypto markets.”

After Black Thursday, ”Bitcoin Reached an Inflection Point of Adoption from Institutions."

Beyond the effects of fear and doubt, the market crash that took place in March of 2020 led to important changes in monetary policy that have had profound effects on the price of Bitcoin.

“Over the course of 2020, a deluge of fiscal stimulus helped contribute to Bitcoin’s store-of-value or ‘digital gold’ narrative that increased awareness of its long-term potential.”

After Black Thursday, “what followed was months of news of the U.S. Government printing trillions of dollars to stimulate the economy and provide economic relief. In fact, 20% of all dollars ever printed since the origins of the U.S. Dollar were printed in 2020,” Kwon explained.

“This massive influx of U.S. dollars into the economy at a rapidly increasing velocity due to lower interest rates, left investors rushing to find the best place to invest their dollars to combat inflation.”

This is what led a growing number of institutional investors into BTC. “Bitcoin, being a scarce digital asset, with a strict 21-million hard cap supply, and its rapid rate of adoption led Bitcoin’s value to sky-rocket and continue hitting all-time highs, far surpassing its previous 2017 peak,” Kwon explained.

Do Kwon, Co-Founder, and CEO of Terraform Labs (TFL).

“[...] Bitcoin reached an inflexion point of adoption from institutions, who began pouring in money as a long-term hedge against inflation. With the halving occurring in May 2020 after the crash, the supply of Bitcoin issued by the protocol was reduced by 50 percent, which also reduced the liquid supply available to the market, making BTC more scarce.”

Marie Tatibouet, Chief Marketing Officer at Gate.io, told Finance Magnates that this scarcity is making Bitcoin increasingly attractive to large investors. “Every company now wants to dedicate their balance sheet to Bitcoin,” she said.

“Microstrategy, Tesla, Square, Ruffers, and others have all gone in on Bitcoin. Other Fortune 500 companies will probably follow suit and buy chunks of Bitcoin, as well. Now, even Ethereum has become a major investment option, with companies like Meitubuying $22M worth of ETH.”

Retail Investors Also Came for Crypto Markets in 2020

But, it was not just institutional investors that came in droves for cryptocurrency in 2020. Steve Ehrlich, Chief Executive of Voyager Digital, explained to Finance Magnates that: “as people across the world were restricted to their homes, many small businesses had to reduce their operations, retail investors were looking for new avenues to invest and trade for supplemental income - causing a surge into cryptocurrency investing.”

Ehlrich says that similar to institutional investors, retail investors in Bitcoin began to see BTC as a hedge against inflation. Verdictreported in January 2021 that retail investors who put their government stimulus checks into BTC were one of the driving factors behind Bitcoin’s massive price increase. Notably, investors who put their first $1400 stimulus check into Bitcoin now have approximately $9000 in BTC.

“These retail investors also see the world becoming more digital, and the digital gold narrative of Bitcoin has never been stronger,” Steve Ehrlich said.

Marie Tatibouet, Chief Marketing Officer at Gate.io.

“In order for Bitcoin to reach a market cap similar to gold, it will have to hit an $11 trillion dollar market cap. Bitcoin now hovers around a $1 trillion dollar market cap, as it continues to gobble up Global liquidity. And, many Bitcoin enthusiasts believe BTC surpassing Gold’s market cap is only a matter of time,” Ehrlich said.

A “Wave of Positive Regulatory Events” Acted as a Boon for Bitcoin

Digital Asset Research’s Doug Scwhenk pointed out that in addition to monetary policy changes and an increasing pool of BTC buyers, crypto has been positively affected by “a wave of positive regulatory events that give institutional investors comfort.”

For example, “the new US administration has nominated a chair of the SEC with prior crypto experience, ETF's have launched in Canada and Bermuda, and the OCC clarified banks can hold these assets.”

Additionally, "storied institutions such as Bank of New York Mellon and Northern Trust have declared public plans and offerings in the space. All of this has served as tremendous tailwinds after an initial shock and great unknown about how our lives would be affected by COVID.”

A New Financial Paradigm in 2022?

If these positive regulatory trends continue in 2022, Bitcoin’s explosive growth could continue. Now that it has been twelve months since Black Thursday, what could crypto markets look like twelve months in the future?

Do Kwon said that while, “it’s impossible to know,” what the future will hold, “at the current rate, it wouldn’t be surprising if we begin to see accelerated adoption of Bitcoin and DeFi by more mainstream investors.”

“Better UX, more capital, better infrastructure, and broader awareness are all ingredients for onboarding more users to a new financial system, one that is more inclusive and open,” Kwon said.

Though it might not arrive in 2022, Steve Ehrlich sees a financial paradigm shift in the future. “More than just a new monetary technology, Bitcoin is an entirely new economic paradigm: an uncompromisable base money protocol for a global, digital, non-state economy,” he said. “It promises to mark the separation of money and state.”

“Bitcoin presents us with an opportunity to reinvent gold and rethink money for the digital future in a more globalized, internet-native way. For those, and many more reasons, Bitcoin and cryptocurrency will continue to enjoy progress and pursuit of a new economic reality.”

Therefore, Bitcoin could reach unprecedented levels in the twelve months ahead: “originally, the idea of a $100,000 Bitcoin seemed like a complete stretch of the imagination, but has now become like a seemingly reasonable target for the rising digital asset,” he said.

“We see cryptocurrency and digital assets going completely mainstream, disrupting traditional financial institutions, and giving economic empowerment to people all over the world in need.”

Rachel is a self-taught crypto geek and a passionate writer. She believes in the power that the written word has to educate, connect and empower individuals to make positive and powerful financial choices. She is the Podcast Host and a Cryptocurrency Editor at Finance Magnates.

Bybit Splits Crypto and Payments Into Two Austrian Entities. Bybit.eu Will Run Both Under One Login

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.