The cryptocurrency industry just had a major victory in India. But are there obstacles on the path to adoption?

FM

Amid all the recent chaos brought about by the coronavirus, there has been perhaps some light for certain aspects of the cryptocurrency world. Following a landmark supreme court victory for the cryptocurrency industry in India, cryptocurrency exchange Binance decided to inject $50 million into India's cryptocurrency ecosystem.

CoinDCX, another Indian cryptocurrency exchange, also announced last week that it would be allocating $1.3 million in funding toward increasing awareness, and thereby, adoption of cryptocurrencies throughout the country as part of 'TryCrypto,' a project that seeks to acquaint 50 million people with cryptocurrency.

Our CEO @smtgpt spoke to @Cointelegraph - "Only 5 million people in India hold crypto.

— CoinDCX: Making Crypto Accessible to Indians (@CoinDCX) March 17, 2020

Other crypto companies have also shown increased interest in establishing themselves in India--and not just since the supreme court victory. In early October of last year, Bithumb Global announced that it would be opening a regulated crypto exchange in India; just over a month ago, crypto trading platform OKEx expanded into India via a partnership with CoinDCX.

Additionally, Huobi announced its intention to launch a peer-to-peer crypto trading platform in India all the way back in July of 2018. US-based cryptocurrency exchange Paxful began working in India last year, running campaigns with Indian media platforms and influencers to build an online community.

With an unbanked population of 190 million people and a massive, $60+ billion dollar remittance industry, the country could be on the brink of becoming crypto's biggest market.

However, although the recent legal battle turned out to be favorable toward crypto, some analysts are saying that crypto's legal war isn't over yet.

The Indian supreme court decided to allow banks to have working relationships with crypto platforms

The supreme court victory for the cryptocurrency industry in India specifically had to do with the country's policy on interactions between banks and cryptocurrency-related businesses.

Before the conclusion of the court case, banks were not allowed to have working relationships with cryptocurrency businesses in India. This was the result of a sweeping ban placed by the Reserve Bank of India (RBI) in April of 2018.

At the time that the ban went into effect, India's budding cryptocurrency industry was all but forced to shut down completely. While a handful of Indian cryptocurrency exchanges managed to stay in business by modifying their business models and becoming peer-to-peer cryptocurrency exchanges, many--if not most--cryptocurrency exchanges in the country were either forced to relocate or close down operations entirely.

The peril that the ban suddenly put the Indian cryptocurrency industry into caused a number of platforms to challenge the ban. Almost immediately after the ban went into effect, cryptocurrency exchanges filed petitions with India's Supreme Court in an attempt to overturn it.

— Nischal (WazirX) ⚡️ (@NischalShetty) March 4, 2020

However, things got worse before they got better. Over the course of the two years that followed, cryptocurrency exchanges in India continuously shut down, and even more severe pieces of legislation made their way through India's legal system. One bill even proposed that the usage of cryptocurrency should be punished with up to 10 years in prison.

By the time the ban was overturned last month, there were only a handful of cryptocurrency exchanges that were still in operation in India.

And hopes are high--" the uplifting of the ban by Supreme Court is going to open new opportunities for India in terms of investments, economy and a market as a whole," said Sumit Gupta, founder and chief executive of CoinDCX to CoinDesk. "As few of the surviving petitioners of the case, we are thankful to the Supreme Court for hearing our side of the story. We have always seen crypto as a potential to unlock India's dream of becoming a $5 trillion economy."

Short- and long-term effects of the overturning of the ban

And even though so little time has passed since the ban was overturned, there have already been some immediate effects.

#Breaking: The Supreme Court of India has struck off the Reserve Bank of India's (RBI) banking ban against #Crypto!

Artur Schaback, chief operating officer and co-founder of cryptocurrency exchange Paxful.

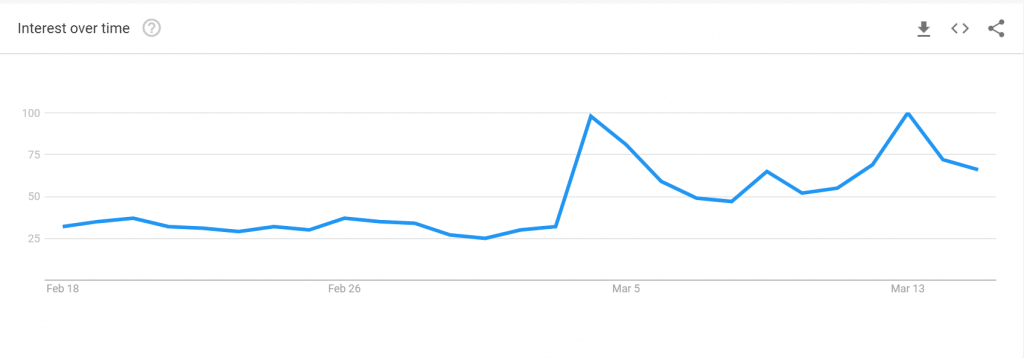

Indeed, in addition to the capital injections from Binance and CoinDCX into various aspects of the industry, Artur Schaback, chief operating officer and co-founder of cryptocurrency exchange Paxful, told Finance Magnates that these effects range "from exchanges offering banking services within hours after the decision was made, to an increase in bitcoin searches online in India."

Indeed, there was a massive increase in the number of searches of the word "bitcoin" immediately following the lift of the ban; less than six hours after the ban was lifted, CoinDCX announced that users could begin purchasing cryptocurrencies with INR as the exchange, becoming the first platform in India to fully integrate bank account transfers post-ban.

The Economic Times, a local financial news outlet, also reported that "several cryptocurrency platforms that had shifted base to Singapore and elsewhere after the RBI circular that was issued on April 6, 2018, are now looking to move back to India."

RBI is reportedly moving to re-instate the ban

However, Manish Kataria, chief operating officer and co-founder of Quadency, said that true change as a result of the ban's overturning would likely take more time.

"The immediate effects are quite limited," Kataria said. "This blanket ban and associated regulatory uncertainty has been stifling innovation for so long that we're just starting to get insights into how exchanges and other providers are planning to scale not just their Indian market presence, but also adoption itself."

And there's also the fact that just as soon as the ban was overturned, the RBI made swift movements to appeal the decision. Within days after the ruling, the Economic Timesreported that the bank was planning on returning to the Supreme Court to fight the decision.

And the bank may have a good deal of support behind it. Despite the fact that some Indian banks have already made moves to work with cryptocurrency firms, some of the country's major banks--including HDFC and Indusind Bank--have chosen to ignore the court's overturning of the ban, saying that they are waiting for the official word from the RBI itself before they begin providing services to crypto companies.

Certain banks have chosen to continue not to serve cryptocurrency firms

The Economic Times reported that in an attempt to address the continuous denial of services, Mohammed Danish of Indian law firm Fintech Lawyers sent a letter to Finance Secretary Ajay Bhushan Pandey and two RBI officers.

Since the case has been ostensibly closed, "the banks (RBI regulated entities) must comply with the order of the supreme court and start providing banking services for sale/purchase of crypto assets impartially as they provide services for all other legitimate transactions," Danish wrote.

However, Danish acknowledged that "it is pertinent to mention that the order of the Hon'ble Supreme Court has given no specific direction to RBI for issuing a separate notification to the banks for compliance of the said order." In other words, RBI has not officially instructed banks to re-open services to crypto platforms, even though the court has made its official decision.

Still, Danish argued in his letter that "Banks' refusal to provide services for sale/purchase of crypto assets is absolutely illegal, unjust and arbitrary in the eyes of [the] law and the same amounts to wilful disobedience to the order of the Hon'ble Supreme Court."

But some banks are still refusing to act until they hear directly from RBI. "We will be guided by RBI's directions on the matter and once we get clarity we will act appropriately," an unnamed senior banker told the Economic Times.

Banks still have concerns over crypto

This is allegedly because the banks still feel as though their concerns regarding the usage of cryptocurrency have not been addressed: "as banks, some of the concerns we had on cryptocurrencies were around security, use of money and traceability," the banker said.

And indeed, while the overturning of the ban was a big victory for India's cryptocurrency industry, the country still has not passed any more general legislation regarding the regulation of cryptocurrencies.

In fact, some analysts have argued that this lack of legislation--in spite of the overturning of the ban--has left the industry vulnerable. In fact, Business Insider India reported shortly after the ban was overturned that the "Banning of Cryptocurrency and Regulation of Official Digital Currency Bill," which is currently making its way through the Indian legislative system, has the potential to hinder the industry.

Siddarth Mahajan, a partner at law firm Athena Legal, told the publication that "it remains to be seen if the government will rethink the proposed bill in light of the Supreme Court judgment. This regulatory uncertainty in India is probably the biggest concern for the government."

"[...] It remains to be seen if the cryptocurrency business in India is positioned as a financial instrument or commodity with underlying value," Mahajan explained. "The biggest fear of the RBI is the proliferation of unregulated financial instruments which are not backed by the state."

India's number of cryptocurrency users is still relatively low, but that could quickly change

And if "proliferation" of these as-yet unregulated currencies is a serious concern for Indian banks, it seems that there's still a long way to go before cryptocurrency becomes anything close to ubiquitous.

Indeed, the estimated number of cryptocurrency users in India ranges quite a bit, depending on who you ask. "I've seen experts' estimations of crypto adoption in India ranging from .02% to .06%," Kataria told Finance Magnates.

Similarly, Artur Schaback said that "Some official figures state that India has 1.7 million crypto investors, while others indicate over 5 million."

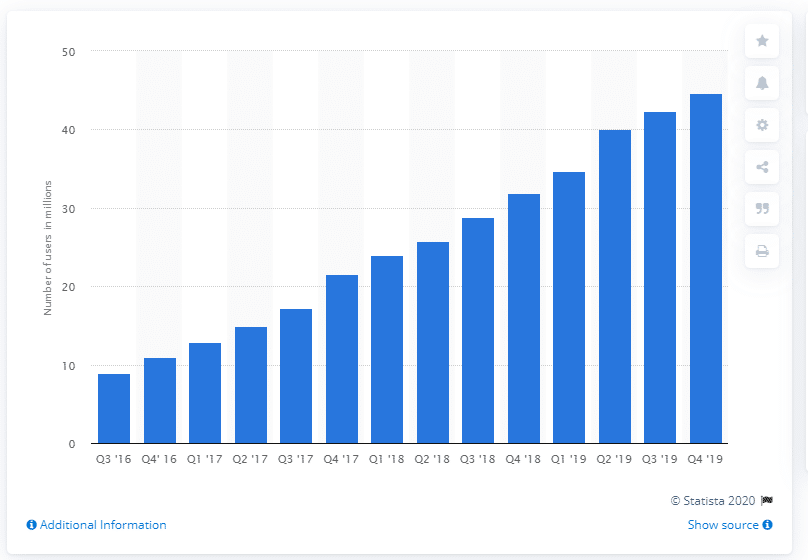

On the other hand, the industry in the rest of the world does seem to be growing at a rapid pace. Data from German-based statistics company Statista shows that in Q1 of 2016, there were roughly 8.95 million blockchain wallet users worldwide; by Q1 of 2018, that figure had climbed to 25.76 million. By the end of 2019, there were 44.69 million.

Number of Blockchain wallet users worldwide from 3rd quarter 2016 to 4th quarter 2019 (in millions).

Because India's population is so large (1.339 billion as of 2017), Kataria pointed out that "even a fractional percentage increase brings millions of new consumers into crypto."

Is India waiting to regulate until the industry is better understood?

Alternatively, however, the fact that a concrete set of regulations for crypto in India doesn't exist yet could also mean that the government is willing to observe the growth of the industry for a while before making any hard and fast decisions about how appropriate regulation might look in India.

Indeed, Srinivas Katta, partner at IndusLaw, told Business Insider that policymakers should consider how cryptocurrencies could be used to build India's economy before acting.

"Cryptocurrency and tokens are an important development and can enable further formalization of the economy if properly implemented," he said. "They can also promote new industries and bring in a lot of investment [as well as] promote the ease of doing business, which is very important."

And even if there isn't a concrete set of regulations for India's crypto industry just yet, the government is still taking steps toward improving the hygiene of the space. On Monday, a filing submitted to the country's lower parliament revealed investigations into two bitcoin companies, Zeb IT Services, and Unocoin Technologies, for a number of allegedly fraudulent practices.

What do you think about the current legal situation surrounding cryptocurrency in India? Let us know in the comments below.

Amid all the recent chaos brought about by the coronavirus, there has been perhaps some light for certain aspects of the cryptocurrency world. Following a landmark supreme court victory for the cryptocurrency industry in India, cryptocurrency exchange Binance decided to inject $50 million into India's cryptocurrency ecosystem.

CoinDCX, another Indian cryptocurrency exchange, also announced last week that it would be allocating $1.3 million in funding toward increasing awareness, and thereby, adoption of cryptocurrencies throughout the country as part of 'TryCrypto,' a project that seeks to acquaint 50 million people with cryptocurrency.

Our CEO @smtgpt spoke to @Cointelegraph - "Only 5 million people in India hold crypto.

— CoinDCX: Making Crypto Accessible to Indians (@CoinDCX) March 17, 2020

Other crypto companies have also shown increased interest in establishing themselves in India--and not just since the supreme court victory. In early October of last year, Bithumb Global announced that it would be opening a regulated crypto exchange in India; just over a month ago, crypto trading platform OKEx expanded into India via a partnership with CoinDCX.

Additionally, Huobi announced its intention to launch a peer-to-peer crypto trading platform in India all the way back in July of 2018. US-based cryptocurrency exchange Paxful began working in India last year, running campaigns with Indian media platforms and influencers to build an online community.

With an unbanked population of 190 million people and a massive, $60+ billion dollar remittance industry, the country could be on the brink of becoming crypto's biggest market.

However, although the recent legal battle turned out to be favorable toward crypto, some analysts are saying that crypto's legal war isn't over yet.

The Indian supreme court decided to allow banks to have working relationships with crypto platforms

The supreme court victory for the cryptocurrency industry in India specifically had to do with the country's policy on interactions between banks and cryptocurrency-related businesses.

Before the conclusion of the court case, banks were not allowed to have working relationships with cryptocurrency businesses in India. This was the result of a sweeping ban placed by the Reserve Bank of India (RBI) in April of 2018.

At the time that the ban went into effect, India's budding cryptocurrency industry was all but forced to shut down completely. While a handful of Indian cryptocurrency exchanges managed to stay in business by modifying their business models and becoming peer-to-peer cryptocurrency exchanges, many--if not most--cryptocurrency exchanges in the country were either forced to relocate or close down operations entirely.

The peril that the ban suddenly put the Indian cryptocurrency industry into caused a number of platforms to challenge the ban. Almost immediately after the ban went into effect, cryptocurrency exchanges filed petitions with India's Supreme Court in an attempt to overturn it.

— Nischal (WazirX) ⚡️ (@NischalShetty) March 4, 2020

However, things got worse before they got better. Over the course of the two years that followed, cryptocurrency exchanges in India continuously shut down, and even more severe pieces of legislation made their way through India's legal system. One bill even proposed that the usage of cryptocurrency should be punished with up to 10 years in prison.

By the time the ban was overturned last month, there were only a handful of cryptocurrency exchanges that were still in operation in India.

And hopes are high--" the uplifting of the ban by Supreme Court is going to open new opportunities for India in terms of investments, economy and a market as a whole," said Sumit Gupta, founder and chief executive of CoinDCX to CoinDesk. "As few of the surviving petitioners of the case, we are thankful to the Supreme Court for hearing our side of the story. We have always seen crypto as a potential to unlock India's dream of becoming a $5 trillion economy."

Short- and long-term effects of the overturning of the ban

And even though so little time has passed since the ban was overturned, there have already been some immediate effects.

#Breaking: The Supreme Court of India has struck off the Reserve Bank of India's (RBI) banking ban against #Crypto!

Artur Schaback, chief operating officer and co-founder of cryptocurrency exchange Paxful.

Indeed, in addition to the capital injections from Binance and CoinDCX into various aspects of the industry, Artur Schaback, chief operating officer and co-founder of cryptocurrency exchange Paxful, told Finance Magnates that these effects range "from exchanges offering banking services within hours after the decision was made, to an increase in bitcoin searches online in India."

Indeed, there was a massive increase in the number of searches of the word "bitcoin" immediately following the lift of the ban; less than six hours after the ban was lifted, CoinDCX announced that users could begin purchasing cryptocurrencies with INR as the exchange, becoming the first platform in India to fully integrate bank account transfers post-ban.

The Economic Times, a local financial news outlet, also reported that "several cryptocurrency platforms that had shifted base to Singapore and elsewhere after the RBI circular that was issued on April 6, 2018, are now looking to move back to India."

RBI is reportedly moving to re-instate the ban

However, Manish Kataria, chief operating officer and co-founder of Quadency, said that true change as a result of the ban's overturning would likely take more time.

"The immediate effects are quite limited," Kataria said. "This blanket ban and associated regulatory uncertainty has been stifling innovation for so long that we're just starting to get insights into how exchanges and other providers are planning to scale not just their Indian market presence, but also adoption itself."

And there's also the fact that just as soon as the ban was overturned, the RBI made swift movements to appeal the decision. Within days after the ruling, the Economic Timesreported that the bank was planning on returning to the Supreme Court to fight the decision.

And the bank may have a good deal of support behind it. Despite the fact that some Indian banks have already made moves to work with cryptocurrency firms, some of the country's major banks--including HDFC and Indusind Bank--have chosen to ignore the court's overturning of the ban, saying that they are waiting for the official word from the RBI itself before they begin providing services to crypto companies.

Certain banks have chosen to continue not to serve cryptocurrency firms

The Economic Times reported that in an attempt to address the continuous denial of services, Mohammed Danish of Indian law firm Fintech Lawyers sent a letter to Finance Secretary Ajay Bhushan Pandey and two RBI officers.

Since the case has been ostensibly closed, "the banks (RBI regulated entities) must comply with the order of the supreme court and start providing banking services for sale/purchase of crypto assets impartially as they provide services for all other legitimate transactions," Danish wrote.

However, Danish acknowledged that "it is pertinent to mention that the order of the Hon'ble Supreme Court has given no specific direction to RBI for issuing a separate notification to the banks for compliance of the said order." In other words, RBI has not officially instructed banks to re-open services to crypto platforms, even though the court has made its official decision.

Still, Danish argued in his letter that "Banks' refusal to provide services for sale/purchase of crypto assets is absolutely illegal, unjust and arbitrary in the eyes of [the] law and the same amounts to wilful disobedience to the order of the Hon'ble Supreme Court."

But some banks are still refusing to act until they hear directly from RBI. "We will be guided by RBI's directions on the matter and once we get clarity we will act appropriately," an unnamed senior banker told the Economic Times.

Banks still have concerns over crypto

This is allegedly because the banks still feel as though their concerns regarding the usage of cryptocurrency have not been addressed: "as banks, some of the concerns we had on cryptocurrencies were around security, use of money and traceability," the banker said.

And indeed, while the overturning of the ban was a big victory for India's cryptocurrency industry, the country still has not passed any more general legislation regarding the regulation of cryptocurrencies.

In fact, some analysts have argued that this lack of legislation--in spite of the overturning of the ban--has left the industry vulnerable. In fact, Business Insider India reported shortly after the ban was overturned that the "Banning of Cryptocurrency and Regulation of Official Digital Currency Bill," which is currently making its way through the Indian legislative system, has the potential to hinder the industry.

Siddarth Mahajan, a partner at law firm Athena Legal, told the publication that "it remains to be seen if the government will rethink the proposed bill in light of the Supreme Court judgment. This regulatory uncertainty in India is probably the biggest concern for the government."

"[...] It remains to be seen if the cryptocurrency business in India is positioned as a financial instrument or commodity with underlying value," Mahajan explained. "The biggest fear of the RBI is the proliferation of unregulated financial instruments which are not backed by the state."

India's number of cryptocurrency users is still relatively low, but that could quickly change

And if "proliferation" of these as-yet unregulated currencies is a serious concern for Indian banks, it seems that there's still a long way to go before cryptocurrency becomes anything close to ubiquitous.

Indeed, the estimated number of cryptocurrency users in India ranges quite a bit, depending on who you ask. "I've seen experts' estimations of crypto adoption in India ranging from .02% to .06%," Kataria told Finance Magnates.

Similarly, Artur Schaback said that "Some official figures state that India has 1.7 million crypto investors, while others indicate over 5 million."

On the other hand, the industry in the rest of the world does seem to be growing at a rapid pace. Data from German-based statistics company Statista shows that in Q1 of 2016, there were roughly 8.95 million blockchain wallet users worldwide; by Q1 of 2018, that figure had climbed to 25.76 million. By the end of 2019, there were 44.69 million.

Number of Blockchain wallet users worldwide from 3rd quarter 2016 to 4th quarter 2019 (in millions).

Because India's population is so large (1.339 billion as of 2017), Kataria pointed out that "even a fractional percentage increase brings millions of new consumers into crypto."

Is India waiting to regulate until the industry is better understood?

Alternatively, however, the fact that a concrete set of regulations for crypto in India doesn't exist yet could also mean that the government is willing to observe the growth of the industry for a while before making any hard and fast decisions about how appropriate regulation might look in India.

Indeed, Srinivas Katta, partner at IndusLaw, told Business Insider that policymakers should consider how cryptocurrencies could be used to build India's economy before acting.

"Cryptocurrency and tokens are an important development and can enable further formalization of the economy if properly implemented," he said. "They can also promote new industries and bring in a lot of investment [as well as] promote the ease of doing business, which is very important."

And even if there isn't a concrete set of regulations for India's crypto industry just yet, the government is still taking steps toward improving the hygiene of the space. On Monday, a filing submitted to the country's lower parliament revealed investigations into two bitcoin companies, Zeb IT Services, and Unocoin Technologies, for a number of allegedly fraudulent practices.

What do you think about the current legal situation surrounding cryptocurrency in India? Let us know in the comments below.

Rachel is a self-taught crypto geek and a passionate writer. She believes in the power that the written word has to educate, connect and empower individuals to make positive and powerful financial choices. She is the Podcast Host and a Cryptocurrency Editor at Finance Magnates.

Prometheum Lands First Disclosed Client for SEC-Regulated Omnibus Crypto Clearing Service

Featured Videos

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

The FX & CFD Market Is Changing Fast. Here's What's Coming Next (2026)

The FX & CFD Market Is Changing Fast. Here's What's Coming Next (2026)

The FX & CFD Market Is Changing Fast. Here's What's Coming Next (2026)

The FX & CFD Market Is Changing Fast. Here's What's Coming Next (2026)

The FX & CFD Market Is Changing Fast. Here's What's Coming Next (2026)

The FX & CFD Market Is Changing Fast. Here's What's Coming Next (2026)

Where is the FX & CFD industry really heading in 2026?

In this free Finance Magnates Intelligence masterclass, industry experts explore the latest data shaping the global FX & CFD market, how regulation and regional demand influence expansion planning, and how brokerages benchmark performance across 265 firms on the FM Intelligence Portal.

In this session you'll learn:

✔ Where the FX/CFD industry is heading in H2 2026

✔ Why compliance should guide regional expansion decisions

✔ How internal performance compares when benchmarked against 265 brokers

✔ Regional demand shifts across Europe, APAC, and LATAM

✔Broker volume rankings, verification, and FM Intelligence Portal data

Speakers:

• Ramzi Ahmad, Director of Intelligence, Finance Magnates

• Sylwester Majewski, Head of Insights & Reporting Hub, Finance Magnates

• Philios Petrides, Data & Business Intelligence Consultant

If you work in brokerage, fintech, compliance, business development or market strategy, this session offers practical insights backed by verified industry data.

Access the FM Intelligence Portal at: https://datalab.financemagnates.com/

🔔 Subscribe to Finance Magnates for more webinars, interviews and market intelligence covering the global online trading industry.

#FinanceMagnates #FX #CFD #Fintech #Trading #Brokerage #MarketIntelligence #RegTech #Compliance #Forex

Where is the FX & CFD industry really heading in 2026?

In this free Finance Magnates Intelligence masterclass, industry experts explore the latest data shaping the global FX & CFD market, how regulation and regional demand influence expansion planning, and how brokerages benchmark performance across 265 firms on the FM Intelligence Portal.

In this session you'll learn:

✔ Where the FX/CFD industry is heading in H2 2026

✔ Why compliance should guide regional expansion decisions

✔ How internal performance compares when benchmarked against 265 brokers

✔ Regional demand shifts across Europe, APAC, and LATAM

✔Broker volume rankings, verification, and FM Intelligence Portal data

Speakers:

• Ramzi Ahmad, Director of Intelligence, Finance Magnates

• Sylwester Majewski, Head of Insights & Reporting Hub, Finance Magnates

• Philios Petrides, Data & Business Intelligence Consultant

If you work in brokerage, fintech, compliance, business development or market strategy, this session offers practical insights backed by verified industry data.

Access the FM Intelligence Portal at: https://datalab.financemagnates.com/

🔔 Subscribe to Finance Magnates for more webinars, interviews and market intelligence covering the global online trading industry.

#FinanceMagnates #FX #CFD #Fintech #Trading #Brokerage #MarketIntelligence #RegTech #Compliance #Forex

Where is the FX & CFD industry really heading in 2026?

In this free Finance Magnates Intelligence masterclass, industry experts explore the latest data shaping the global FX & CFD market, how regulation and regional demand influence expansion planning, and how brokerages benchmark performance across 265 firms on the FM Intelligence Portal.

In this session you'll learn:

✔ Where the FX/CFD industry is heading in H2 2026

✔ Why compliance should guide regional expansion decisions

✔ How internal performance compares when benchmarked against 265 brokers

✔ Regional demand shifts across Europe, APAC, and LATAM

✔Broker volume rankings, verification, and FM Intelligence Portal data

Speakers:

• Ramzi Ahmad, Director of Intelligence, Finance Magnates

• Sylwester Majewski, Head of Insights & Reporting Hub, Finance Magnates

• Philios Petrides, Data & Business Intelligence Consultant

If you work in brokerage, fintech, compliance, business development or market strategy, this session offers practical insights backed by verified industry data.

Access the FM Intelligence Portal at: https://datalab.financemagnates.com/

🔔 Subscribe to Finance Magnates for more webinars, interviews and market intelligence covering the global online trading industry.

#FinanceMagnates #FX #CFD #Fintech #Trading #Brokerage #MarketIntelligence #RegTech #Compliance #Forex

Where is the FX & CFD industry really heading in 2026?

In this free Finance Magnates Intelligence masterclass, industry experts explore the latest data shaping the global FX & CFD market, how regulation and regional demand influence expansion planning, and how brokerages benchmark performance across 265 firms on the FM Intelligence Portal.

In this session you'll learn:

✔ Where the FX/CFD industry is heading in H2 2026

✔ Why compliance should guide regional expansion decisions

✔ How internal performance compares when benchmarked against 265 brokers

✔ Regional demand shifts across Europe, APAC, and LATAM

✔Broker volume rankings, verification, and FM Intelligence Portal data

Speakers:

• Ramzi Ahmad, Director of Intelligence, Finance Magnates

• Sylwester Majewski, Head of Insights & Reporting Hub, Finance Magnates

• Philios Petrides, Data & Business Intelligence Consultant

If you work in brokerage, fintech, compliance, business development or market strategy, this session offers practical insights backed by verified industry data.

Access the FM Intelligence Portal at: https://datalab.financemagnates.com/

🔔 Subscribe to Finance Magnates for more webinars, interviews and market intelligence covering the global online trading industry.

#FinanceMagnates #FX #CFD #Fintech #Trading #Brokerage #MarketIntelligence #RegTech #Compliance #Forex

Where is the FX & CFD industry really heading in 2026?

In this free Finance Magnates Intelligence masterclass, industry experts explore the latest data shaping the global FX & CFD market, how regulation and regional demand influence expansion planning, and how brokerages benchmark performance across 265 firms on the FM Intelligence Portal.

In this session you'll learn:

✔ Where the FX/CFD industry is heading in H2 2026

✔ Why compliance should guide regional expansion decisions

✔ How internal performance compares when benchmarked against 265 brokers

✔ Regional demand shifts across Europe, APAC, and LATAM

✔Broker volume rankings, verification, and FM Intelligence Portal data

Speakers:

• Ramzi Ahmad, Director of Intelligence, Finance Magnates

• Sylwester Majewski, Head of Insights & Reporting Hub, Finance Magnates

• Philios Petrides, Data & Business Intelligence Consultant

If you work in brokerage, fintech, compliance, business development or market strategy, this session offers practical insights backed by verified industry data.

Access the FM Intelligence Portal at: https://datalab.financemagnates.com/

🔔 Subscribe to Finance Magnates for more webinars, interviews and market intelligence covering the global online trading industry.

#FinanceMagnates #FX #CFD #Fintech #Trading #Brokerage #MarketIntelligence #RegTech #Compliance #Forex

Where is the FX & CFD industry really heading in 2026?

In this free Finance Magnates Intelligence masterclass, industry experts explore the latest data shaping the global FX & CFD market, how regulation and regional demand influence expansion planning, and how brokerages benchmark performance across 265 firms on the FM Intelligence Portal.

In this session you'll learn:

✔ Where the FX/CFD industry is heading in H2 2026

✔ Why compliance should guide regional expansion decisions

✔ How internal performance compares when benchmarked against 265 brokers

✔ Regional demand shifts across Europe, APAC, and LATAM

✔Broker volume rankings, verification, and FM Intelligence Portal data

Speakers:

• Ramzi Ahmad, Director of Intelligence, Finance Magnates

• Sylwester Majewski, Head of Insights & Reporting Hub, Finance Magnates

• Philios Petrides, Data & Business Intelligence Consultant

If you work in brokerage, fintech, compliance, business development or market strategy, this session offers practical insights backed by verified industry data.

Access the FM Intelligence Portal at: https://datalab.financemagnates.com/

🔔 Subscribe to Finance Magnates for more webinars, interviews and market intelligence covering the global online trading industry.

#FinanceMagnates #FX #CFD #Fintech #Trading #Brokerage #MarketIntelligence #RegTech #Compliance #Forex

How Finance Leaders Adapt to Change | iFX EXPO

How Finance Leaders Adapt to Change | iFX EXPO

How Finance Leaders Adapt to Change | iFX EXPO

How Finance Leaders Adapt to Change | iFX EXPO

How Finance Leaders Adapt to Change | iFX EXPO

How Finance Leaders Adapt to Change | iFX EXPO

Markets never stop changing.

We asked finance executives for their number one success tip, and many came back to the same idea: adapt, stay informed and keep looking ahead.

Featuring executives from Shift Markets, Letknow Pay, Base Markets and SPAYZ.io.

#FinanceMagnates #Leadership #BusinessStrategy #Fintech #Shorts

Markets never stop changing.

We asked finance executives for their number one success tip, and many came back to the same idea: adapt, stay informed and keep looking ahead.

Featuring executives from Shift Markets, Letknow Pay, Base Markets and SPAYZ.io.

#FinanceMagnates #Leadership #BusinessStrategy #Fintech #Shorts

Markets never stop changing.

We asked finance executives for their number one success tip, and many came back to the same idea: adapt, stay informed and keep looking ahead.

Featuring executives from Shift Markets, Letknow Pay, Base Markets and SPAYZ.io.

#FinanceMagnates #Leadership #BusinessStrategy #Fintech #Shorts

Markets never stop changing.

We asked finance executives for their number one success tip, and many came back to the same idea: adapt, stay informed and keep looking ahead.

Featuring executives from Shift Markets, Letknow Pay, Base Markets and SPAYZ.io.

#FinanceMagnates #Leadership #BusinessStrategy #Fintech #Shorts

Markets never stop changing.

We asked finance executives for their number one success tip, and many came back to the same idea: adapt, stay informed and keep looking ahead.

Featuring executives from Shift Markets, Letknow Pay, Base Markets and SPAYZ.io.

#FinanceMagnates #Leadership #BusinessStrategy #Fintech #Shorts

Markets never stop changing.

We asked finance executives for their number one success tip, and many came back to the same idea: adapt, stay informed and keep looking ahead.

Featuring executives from Shift Markets, Letknow Pay, Base Markets and SPAYZ.io.

#FinanceMagnates #Leadership #BusinessStrategy #Fintech #Shorts