Straying off the trading screen, Idan Levitov muses on how the banking industry will look within ten years.

Bloomberg

Today, major threats loom on the horizon for capital markets and the banking industry. Analysts remain as uncertain as ever about the future of this sector, but change is definitely coming. The question is how banks can survive and prosper in a world of disruptive technology.

Among the many forces challenging the banking industry are consolidated marketplace lending facilities, innovative payment systems, seamless trading, dynamic organisational functionality and digital-ready brands. This disruption poses serious challenges to the industry, and an in-depth understanding of these issues is required.

The forces of change are ever-present in all industries. However, the banking industry is particularly vulnerable in the sense that change comes from the proactive disruption of organisational business models. Important questions about the future of the banking industry need to be considered.

The banking industry is particularly vulnerable in the sense that change comes from the proactive disruption of organisational business models

These questions relate to the nature of the competition in the banking industry within the next decade. In other words, will market players be weaker and smaller, or stronger and larger? Another question that needs to be considered is the technology that will transform the banking industry. Finally, the question of how banks will strategically prepare for future realities must be answered.

How important is disruption in the banking industry?

There are many possible future scenarios that the banking industry could veer off into, including multiple choices without brands, security with no privacy, banking without bankers or branches, banking operations without any infrastructure, trading without the presence of traders, investing with no managers, and lending without deposits among others. The future of banking could take any shape or form, but what is certain is that change is coming.

The future of banking could take any shape or form, but what is certain is that change is coming

Complex banking institutions have been working rigorously to simplify their businesses and lower their reliance on traditional infrastructure, in favour of online banking and trading. The reasons for this are varied, and include cost-cutting and delayering of the organisational hierarchy. Banks have come to understand that it is not possible for them to prosper in every single business activity.

Therefore, a common practice that has developed is the outsourcing of non-essential activities. Banks in the next 10 years will be required to maintain an organisational entity comprised of employees and non-employees alike. Company unity will be tested with this new paradigm in a way never before seen. A greater awareness of multiculturalism is needed in this highly flexible organisational paradigm.

Non-core infrastructural activity will be outsourced to 3rd parties. And in much the same way, the interconnectedness between banks will be facilitated by third parties, an Internet of vendors, or a complex online network. While there are many risks inherent in this new banking ecosystem, there are also many available opportunities. Banks have been moving closer towards shaping and developing a far more customer-centric experience.

The global financial crisis of 2008/2009 forever changed the way that different banks are perceived and trusted by customers. The damage suffered by many banking institutions over the last decade has been immense. Market participants simply place little credibility in the banking and financial sector as a viable investment option. Personalised banking is the way of the future, available in the present.

The banking industry continues to tailor options to the needs of individual clients wherever they may be. Indeed, this is one of the only ways to generate the kind of brand loyalty that banks require to survive in the modern age.

How can Banks Differentiate Their Offerings?

There is no doubt that Wells Fargo, Bank of America, Citibank, JP Morgan Chase & Co and others have failed where Facebook, Google, Twitter and other tech companies have prospered. Building this type of brand equity takes time, trust and massive investment. But it is necessary if banks are to succeed as trusted operators. Two ways that banks can build brand equity with customers include the following: an immersive customer experience tailored to the needs of individual clients, and service differentiation among banks and financial institutions.

Technological innovations in the banking industry are going to change dramatically

A superblock chain industry could become a reality by 2025. There is no doubt that digital currencies (cryptocurrencies) will rapidly gain in popularity. Already the online gaming industry is switching to digital currencies to avoid repressive regulations with fiat currency.

When it comes to the human trader, this could well be a ‘dying art’. We are increasingly seeing trading taking place without the presence of traders. This is being done with algorithmic trading and electronic exchanges. The question of whether machine intelligence will ever completely replace humans appears to be a foregone conclusion: it will. Human beings in a tech-heavy banking industry will be in charge of overseeing these automated transactions.

Brighter days for human traders? (Photo: Bloomberg)

Humans will be the intellectual capital that is designing the algorithmic codes and managing things like advice, insight and oversight. But one of the most hyped themes in banking, particularly US banking, is disintermediation. Back in the day, banks loaned substantial sums of money to the corporate sector. But now, that accounts for just 30% of all corporate debt.

Increasing regulation of US banks is a problem. Another major problem is multi-year interest-rate lows. This erodes the profitability of banks in a big way. And, new entrants to the banking industry don’t need substantial sums of capital anymore. We are seeing a spike in marketplace lending companies at the expense of traditional banking institutions.

Increasing regulation of US banks is a problem

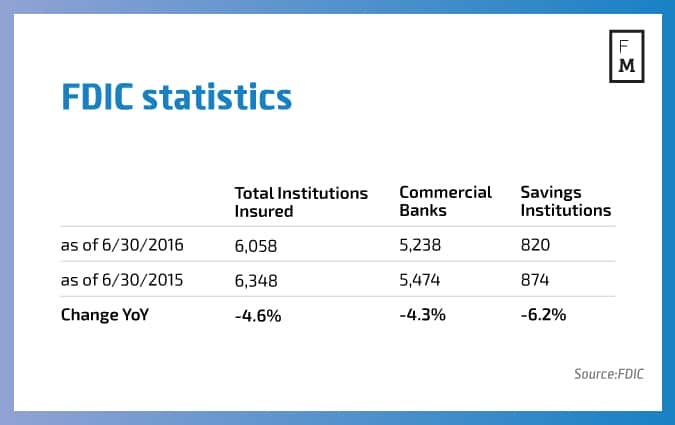

FDIC Statistics (June 30, 2016)

The number of insured institutions as at June 30, 2016 was 6,058. This included 5,238 commercial banks and 820 savings institutions. By contrast, the number of FDIC supervised institutions was 3,878. This is made up of 3,482 commercial banks and 396 savings institutions. These figures compare unfavourably to Q2 2015 figures. Back then, there were 6,348 insured institutions, comprised of 5,474 commercial banks and 874 savings tuitions. In terms of the asset concentration group, some 322 FDIC insured institutions are considered to have a net worth of less than $1 billion.

Why Is the Wells Fargo Case So Important for Banks?

The massive accounts scandal that took place at Wells Fargo will result in tens of thousands of dismissals in the banking sector. US consumer banks will be shedding employees at an unprecedented rate now that 2 million fake credit card accounts and other accounts have been discovered.

State regulators and federal regulators are expected to collect upwards of $185 million from Wells Fargo bank. Employee sales practices are now being questioned across the board – Wells Fargo, Citibank, JP Morgan Chase & Co, Bank of America Merrill Lynch and others. Banking services are now more likely than ever to be delivered online as opposed to physical delivery. Retail banking will suffer losses in the tens of thousands of personnel. Everything is about cost savings, and online banking satisfies this need in a big way.

Bloomberg

Online Banking Takes the Lead over Conventional Banking

Wells Fargo currently employs in excess of 200,000 people in its US branches. Therefore, it automatically ranks as one of the top 3 largest financial employees in the country. By contrast, JP Morgan features 180,000 employees. Automation is going to continue cutting numbers. In 2015, the worldwide banking industry had to let go of some 100,000 employees. In the same year, Bank of America reduced its payroll by 10,000 employees.

This year, analysts are expecting upwards of 8,000 job losses in its consumer banking group. The reason for this is clear: customers are switching to the digital platform and bypassing conventional methods. We also have to watch for regulation and how it impacts banks and other financial institutions. For now, it is clear that transformation and digitalization is running the show. The age of tellers and human interaction is fast disappearing, now that online banking has taken the lead.

Bloomberg

Idan Levitov

Idan Levtov is the anyoption.com's VP trading. He is a seasoned professional with years of experience trading and has a vast knowledge of the financial markets. An expert in the binary options hedging field - Idan provides insights, guidance and coordination in business planning, risk management and technology strategies.

Today, major threats loom on the horizon for capital markets and the banking industry. Analysts remain as uncertain as ever about the future of this sector, but change is definitely coming. The question is how banks can survive and prosper in a world of disruptive technology.

Among the many forces challenging the banking industry are consolidated marketplace lending facilities, innovative payment systems, seamless trading, dynamic organisational functionality and digital-ready brands. This disruption poses serious challenges to the industry, and an in-depth understanding of these issues is required.

The forces of change are ever-present in all industries. However, the banking industry is particularly vulnerable in the sense that change comes from the proactive disruption of organisational business models. Important questions about the future of the banking industry need to be considered.

The banking industry is particularly vulnerable in the sense that change comes from the proactive disruption of organisational business models

These questions relate to the nature of the competition in the banking industry within the next decade. In other words, will market players be weaker and smaller, or stronger and larger? Another question that needs to be considered is the technology that will transform the banking industry. Finally, the question of how banks will strategically prepare for future realities must be answered.

How important is disruption in the banking industry?

There are many possible future scenarios that the banking industry could veer off into, including multiple choices without brands, security with no privacy, banking without bankers or branches, banking operations without any infrastructure, trading without the presence of traders, investing with no managers, and lending without deposits among others. The future of banking could take any shape or form, but what is certain is that change is coming.

The future of banking could take any shape or form, but what is certain is that change is coming

Complex banking institutions have been working rigorously to simplify their businesses and lower their reliance on traditional infrastructure, in favour of online banking and trading. The reasons for this are varied, and include cost-cutting and delayering of the organisational hierarchy. Banks have come to understand that it is not possible for them to prosper in every single business activity.

Therefore, a common practice that has developed is the outsourcing of non-essential activities. Banks in the next 10 years will be required to maintain an organisational entity comprised of employees and non-employees alike. Company unity will be tested with this new paradigm in a way never before seen. A greater awareness of multiculturalism is needed in this highly flexible organisational paradigm.

Non-core infrastructural activity will be outsourced to 3rd parties. And in much the same way, the interconnectedness between banks will be facilitated by third parties, an Internet of vendors, or a complex online network. While there are many risks inherent in this new banking ecosystem, there are also many available opportunities. Banks have been moving closer towards shaping and developing a far more customer-centric experience.

The global financial crisis of 2008/2009 forever changed the way that different banks are perceived and trusted by customers. The damage suffered by many banking institutions over the last decade has been immense. Market participants simply place little credibility in the banking and financial sector as a viable investment option. Personalised banking is the way of the future, available in the present.

The banking industry continues to tailor options to the needs of individual clients wherever they may be. Indeed, this is one of the only ways to generate the kind of brand loyalty that banks require to survive in the modern age.

How can Banks Differentiate Their Offerings?

There is no doubt that Wells Fargo, Bank of America, Citibank, JP Morgan Chase & Co and others have failed where Facebook, Google, Twitter and other tech companies have prospered. Building this type of brand equity takes time, trust and massive investment. But it is necessary if banks are to succeed as trusted operators. Two ways that banks can build brand equity with customers include the following: an immersive customer experience tailored to the needs of individual clients, and service differentiation among banks and financial institutions.

Technological innovations in the banking industry are going to change dramatically

A superblock chain industry could become a reality by 2025. There is no doubt that digital currencies (cryptocurrencies) will rapidly gain in popularity. Already the online gaming industry is switching to digital currencies to avoid repressive regulations with fiat currency.

When it comes to the human trader, this could well be a ‘dying art’. We are increasingly seeing trading taking place without the presence of traders. This is being done with algorithmic trading and electronic exchanges. The question of whether machine intelligence will ever completely replace humans appears to be a foregone conclusion: it will. Human beings in a tech-heavy banking industry will be in charge of overseeing these automated transactions.

Brighter days for human traders? (Photo: Bloomberg)

Humans will be the intellectual capital that is designing the algorithmic codes and managing things like advice, insight and oversight. But one of the most hyped themes in banking, particularly US banking, is disintermediation. Back in the day, banks loaned substantial sums of money to the corporate sector. But now, that accounts for just 30% of all corporate debt.

Increasing regulation of US banks is a problem. Another major problem is multi-year interest-rate lows. This erodes the profitability of banks in a big way. And, new entrants to the banking industry don’t need substantial sums of capital anymore. We are seeing a spike in marketplace lending companies at the expense of traditional banking institutions.

Increasing regulation of US banks is a problem

FDIC Statistics (June 30, 2016)

The number of insured institutions as at June 30, 2016 was 6,058. This included 5,238 commercial banks and 820 savings institutions. By contrast, the number of FDIC supervised institutions was 3,878. This is made up of 3,482 commercial banks and 396 savings institutions. These figures compare unfavourably to Q2 2015 figures. Back then, there were 6,348 insured institutions, comprised of 5,474 commercial banks and 874 savings tuitions. In terms of the asset concentration group, some 322 FDIC insured institutions are considered to have a net worth of less than $1 billion.

Why Is the Wells Fargo Case So Important for Banks?

The massive accounts scandal that took place at Wells Fargo will result in tens of thousands of dismissals in the banking sector. US consumer banks will be shedding employees at an unprecedented rate now that 2 million fake credit card accounts and other accounts have been discovered.

State regulators and federal regulators are expected to collect upwards of $185 million from Wells Fargo bank. Employee sales practices are now being questioned across the board – Wells Fargo, Citibank, JP Morgan Chase & Co, Bank of America Merrill Lynch and others. Banking services are now more likely than ever to be delivered online as opposed to physical delivery. Retail banking will suffer losses in the tens of thousands of personnel. Everything is about cost savings, and online banking satisfies this need in a big way.

Bloomberg

Online Banking Takes the Lead over Conventional Banking

Wells Fargo currently employs in excess of 200,000 people in its US branches. Therefore, it automatically ranks as one of the top 3 largest financial employees in the country. By contrast, JP Morgan features 180,000 employees. Automation is going to continue cutting numbers. In 2015, the worldwide banking industry had to let go of some 100,000 employees. In the same year, Bank of America reduced its payroll by 10,000 employees.

This year, analysts are expecting upwards of 8,000 job losses in its consumer banking group. The reason for this is clear: customers are switching to the digital platform and bypassing conventional methods. We also have to watch for regulation and how it impacts banks and other financial institutions. For now, it is clear that transformation and digitalization is running the show. The age of tellers and human interaction is fast disappearing, now that online banking has taken the lead.

Bloomberg

Idan Levitov

Idan Levtov is the anyoption.com's VP trading. He is a seasoned professional with years of experience trading and has a vast knowledge of the financial markets. An expert in the binary options hedging field - Idan provides insights, guidance and coordination in business planning, risk management and technology strategies.

Idan is the VP trading for anyoption.com. He is a seasoned professional with years of experience trading and has a vast knowledge of the financial markets. An expert in the binary options hedging field - Idan provides insights, guidance and coordination in business planning, risk management and technology strategies. He holds a BA in Economics Management and is now busy finishing his MBA in Finance. Idan is the VP trading for anyoption.com. He is a seasoned professional with years of experience and a vast knowledge of the financial markets. An expert in the binary options hedging field - Idan provides insights, guidance and coordination in business planning, risk management and technology strategies. He holds a BA in Economics Management and is now busy finishing his MBA in Finance.

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.