BIS Releases Data on Effects of Intervention in Peru's $700 Million Per Day FX Market

Wednesday,18/09/2013|11:12GMTby

Andrew Saks McLeod

The Bank For International Settlements has today released the results of a study in which it extrapolated data from Peru's interbank FX market over a two year period to examine the effects of FX intervention.

South America is a relatively unknown quantity among many market participants, its own rapidly developing FX industry having remained in the shadow of its mainstream counterparts such as Europe, North America and the Far East – until now.

Today, the Bank for International Settlements (BIS), released a report in which the results of its examination of the asymmetric effects of FOREX intervention using intraday data are documented, using evidence from the Peruvian market.

Proprietary Platform Serves Domestic Market

Peru, according to the report, has a very domestic-oriented inter-bank FX market, being primarily a local market based on spot transactions. Although, there is a forwards and options market, it is very small compared to the nation’s spot FX market.

Exchange Rates And FX Intevention

Spot forex market transactions take place primarily on a private electronic Trading Platform, operated by the company DATATEC. The platform is based on a blind system in which the bidders are known only to those involved in the transaction, and become generally known only after the transaction is closed.

It operates between 9 am and 1:30 pm, Monday through Friday. The transactions are settled same day, under a real time gross settlement (RTGS) system, on a payment versus payment platform through each bank's account at the central bank.

The participants in the FX market are commercial banks. However, about five banks are the major players in terms of average amount traded. Currently, the average amount traded in the interbank spot forex market is around $700 million a day. The record amount for one day is approximately $1,700 million, representing almost 1 percent of GDP.

Central Bank Intervenes In Peruvian FX Market

FX operations are part of Peru’s open market operations to regulate daily Liquidity . Decisions on both forex operations and open market operations are made every day by a committee, that meets between 11:30 am and 1 pm. The BIS research paper covers the literature, and contributes to the literature on foreign exchange intervention in emerging market economies in three dimensions.

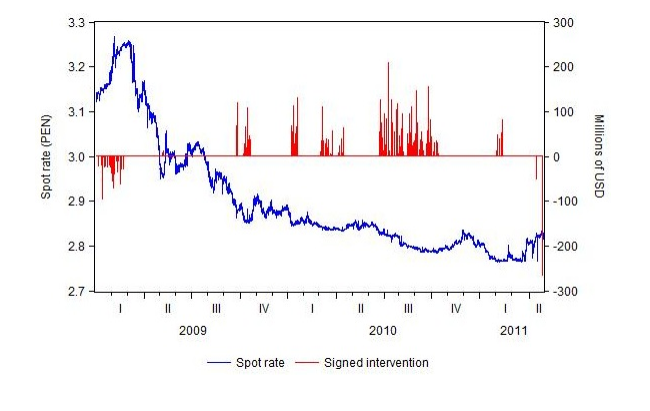

The initial point of interest is that this represents the first time, undisclosed and comprehensive intraday intervention data - minute by minute data points for all trading days between January 2009 and April 2011 - have been used for Peru.

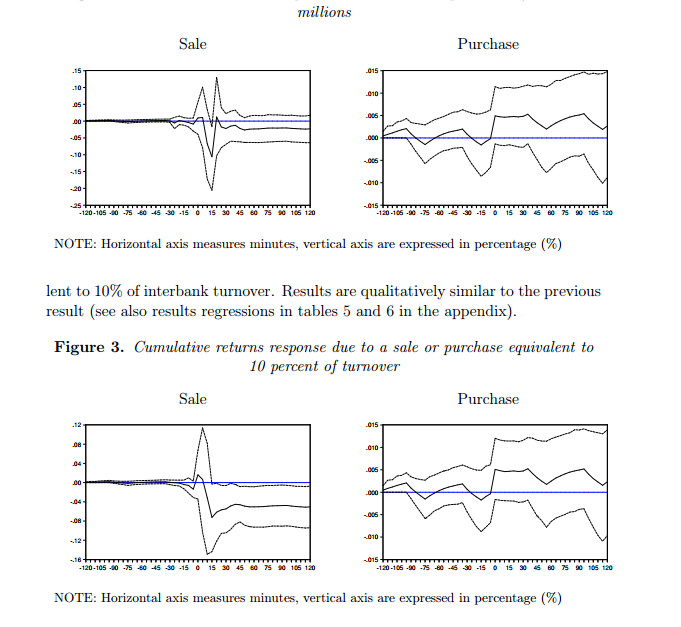

Secondly, the paper shows that Central Bank interventions in the foreign exchange market have asymmetric effects on the spot exchange rate.

In particular, sale interventions have a greater effect on exchange rate than purchase interventions. This result is robust to event study regressions, and to a SVAR identification proposed in the research paper.

Lastly, the paper provides a simple signaling framework which formalizes the asymmetric effect, whereby sale interventions are more effective than purchase interventions.

Asymmetric Loss Functions

For policy makers who participate in the forex market, the dangers of sharp exchange rate depreciations are markedly different from those of exchange rate appreciations. Exchange rate depreciations are linked to stress episodes associated with financial crises. Fear of floating entails, mostly a fear of depreciation. Large and abrupt depreciations trigger fears of financial distress. Such fears are particularly acute in emerging market economies whose financial markets are vulnerable - for example, as a result of financial dollarization.

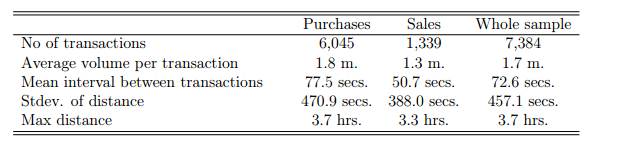

Descriptive Statistics From Transaction-Level Intervention Data

In contrast, exchange rate appreciations are not linked to short-run financial crises, but to capital flow bonanzas. Thus, fear of appreciation is more related to fear of misallocation of resources between tradeable and non-tradeable sectors, and fear of excessive credit booms.

The BIS considers that in this case, the asymmetry turns on the fact that large depreciations are avoided because they may imply financial crisis in the short run, while sharp or persistent appreciations are avoided, because these may harm growth prospects.

An asymmetric reaction function, in turn, implies that for a given pressure of appreciation or depreciation, the central bank intervenes differently, depending on whether it is purchasing or selling. This means that the features of purchase and sale interventions differ in terms of the volume of each transaction, daily aggregate volumes, dispersion of intervention transactions across market participants and intraday timing of intervention.

The data used to compile this particular report was extrapolated from trading activity between 2009 and 2011 in Peru’s FX markets. The paper shows that central bank interventions in the FX market have asymmetric effects on the spot exchange rate. In particular, sale interventions are more effective than purchase interventions. In addition, the conclusion reached by the BIS confirms a previous finding for Peru, which was documented in Flores in 2003.

Latin America in general, is fast becoming a region of interest among the institutional FX sector. For a full and detailed report on the entire dynamics of the FX landscape in Latin America, Forex Magnates research can be purchased here.

South America is a relatively unknown quantity among many market participants, its own rapidly developing FX industry having remained in the shadow of its mainstream counterparts such as Europe, North America and the Far East – until now.

Today, the Bank for International Settlements (BIS), released a report in which the results of its examination of the asymmetric effects of FOREX intervention using intraday data are documented, using evidence from the Peruvian market.

Proprietary Platform Serves Domestic Market

Peru, according to the report, has a very domestic-oriented inter-bank FX market, being primarily a local market based on spot transactions. Although, there is a forwards and options market, it is very small compared to the nation’s spot FX market.

Exchange Rates And FX Intevention

Spot forex market transactions take place primarily on a private electronic Trading Platform, operated by the company DATATEC. The platform is based on a blind system in which the bidders are known only to those involved in the transaction, and become generally known only after the transaction is closed.

It operates between 9 am and 1:30 pm, Monday through Friday. The transactions are settled same day, under a real time gross settlement (RTGS) system, on a payment versus payment platform through each bank's account at the central bank.

The participants in the FX market are commercial banks. However, about five banks are the major players in terms of average amount traded. Currently, the average amount traded in the interbank spot forex market is around $700 million a day. The record amount for one day is approximately $1,700 million, representing almost 1 percent of GDP.

Central Bank Intervenes In Peruvian FX Market

FX operations are part of Peru’s open market operations to regulate daily Liquidity . Decisions on both forex operations and open market operations are made every day by a committee, that meets between 11:30 am and 1 pm. The BIS research paper covers the literature, and contributes to the literature on foreign exchange intervention in emerging market economies in three dimensions.

The initial point of interest is that this represents the first time, undisclosed and comprehensive intraday intervention data - minute by minute data points for all trading days between January 2009 and April 2011 - have been used for Peru.

Secondly, the paper shows that Central Bank interventions in the foreign exchange market have asymmetric effects on the spot exchange rate.

In particular, sale interventions have a greater effect on exchange rate than purchase interventions. This result is robust to event study regressions, and to a SVAR identification proposed in the research paper.

Lastly, the paper provides a simple signaling framework which formalizes the asymmetric effect, whereby sale interventions are more effective than purchase interventions.

Asymmetric Loss Functions

For policy makers who participate in the forex market, the dangers of sharp exchange rate depreciations are markedly different from those of exchange rate appreciations. Exchange rate depreciations are linked to stress episodes associated with financial crises. Fear of floating entails, mostly a fear of depreciation. Large and abrupt depreciations trigger fears of financial distress. Such fears are particularly acute in emerging market economies whose financial markets are vulnerable - for example, as a result of financial dollarization.

Descriptive Statistics From Transaction-Level Intervention Data

In contrast, exchange rate appreciations are not linked to short-run financial crises, but to capital flow bonanzas. Thus, fear of appreciation is more related to fear of misallocation of resources between tradeable and non-tradeable sectors, and fear of excessive credit booms.

The BIS considers that in this case, the asymmetry turns on the fact that large depreciations are avoided because they may imply financial crisis in the short run, while sharp or persistent appreciations are avoided, because these may harm growth prospects.

An asymmetric reaction function, in turn, implies that for a given pressure of appreciation or depreciation, the central bank intervenes differently, depending on whether it is purchasing or selling. This means that the features of purchase and sale interventions differ in terms of the volume of each transaction, daily aggregate volumes, dispersion of intervention transactions across market participants and intraday timing of intervention.

The data used to compile this particular report was extrapolated from trading activity between 2009 and 2011 in Peru’s FX markets. The paper shows that central bank interventions in the FX market have asymmetric effects on the spot exchange rate. In particular, sale interventions are more effective than purchase interventions. In addition, the conclusion reached by the BIS confirms a previous finding for Peru, which was documented in Flores in 2003.

Latin America in general, is fast becoming a region of interest among the institutional FX sector. For a full and detailed report on the entire dynamics of the FX landscape in Latin America, Forex Magnates research can be purchased here.

CFTC Lets US Firms Keep Trading Swaps on Two More UK Platforms After Brexit

CMC Markets’ Artur Delijergijevs on Metals Demand, Volatility, & Stable Execution

CMC Markets’ Artur Delijergijevs on Metals Demand, Volatility, & Stable Execution

In this exclusive Executive Interview, Finance Magnates speaks with Artur Delijergijevs, Head of Systematic Market Making at CMC Markets, about the current state of metals demand and market volatility.

Delijergijevs offers a desk-level view on:

- Metals Demand: Why metals are seeing the strongest demand from both retail and institutional clients right now.

- The Safe-Haven Debate: Questioning whether gold still fits the classic safe-haven definition given large daily price movements.

- Volatile Market Prep: How a market-making desk prepares its systems and pricing for stressed market conditions and high-impact economic events.

- Hybrid Execution: Why the best execution model combines electronic speed with human relationship support, especially during volatility.

- AI in Workflow: Where CMC Markets is integrating machine learning for risk management and pricing, and the limitations of AI during stressed markets.

- Dubai's Role: The strategic importance of Dubai’s location for covering global trading sessions across Asia, Europe, and the US.

Watch to understand how CMC Markets maintains stable pricing and reliable execution quality in high-volatility environments.

#CMCmarkets #forex #metals #gold #trading #volatility #MarketMaking #iFXDubai #FinanceMagnates #Finance #Fintech #Execution #AlgorithmicTrading #RiskManagement

In this exclusive Executive Interview, Finance Magnates speaks with Artur Delijergijevs, Head of Systematic Market Making at CMC Markets, about the current state of metals demand and market volatility.

Delijergijevs offers a desk-level view on:

- Metals Demand: Why metals are seeing the strongest demand from both retail and institutional clients right now.

- The Safe-Haven Debate: Questioning whether gold still fits the classic safe-haven definition given large daily price movements.

- Volatile Market Prep: How a market-making desk prepares its systems and pricing for stressed market conditions and high-impact economic events.

- Hybrid Execution: Why the best execution model combines electronic speed with human relationship support, especially during volatility.

- AI in Workflow: Where CMC Markets is integrating machine learning for risk management and pricing, and the limitations of AI during stressed markets.

- Dubai's Role: The strategic importance of Dubai’s location for covering global trading sessions across Asia, Europe, and the US.

Watch to understand how CMC Markets maintains stable pricing and reliable execution quality in high-volatility environments.

#CMCmarkets #forex #metals #gold #trading #volatility #MarketMaking #iFXDubai #FinanceMagnates #Finance #Fintech #Execution #AlgorithmicTrading #RiskManagement

Finance Magnates Awards 2026 – Nominations Now Open

Finance Magnates Awards 2026 – Nominations Now Open

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech