Financial services firm Marex has created and sold a structured note linked to the outcome of a prediction market, offering investors a new way to structure event-based payoffs.

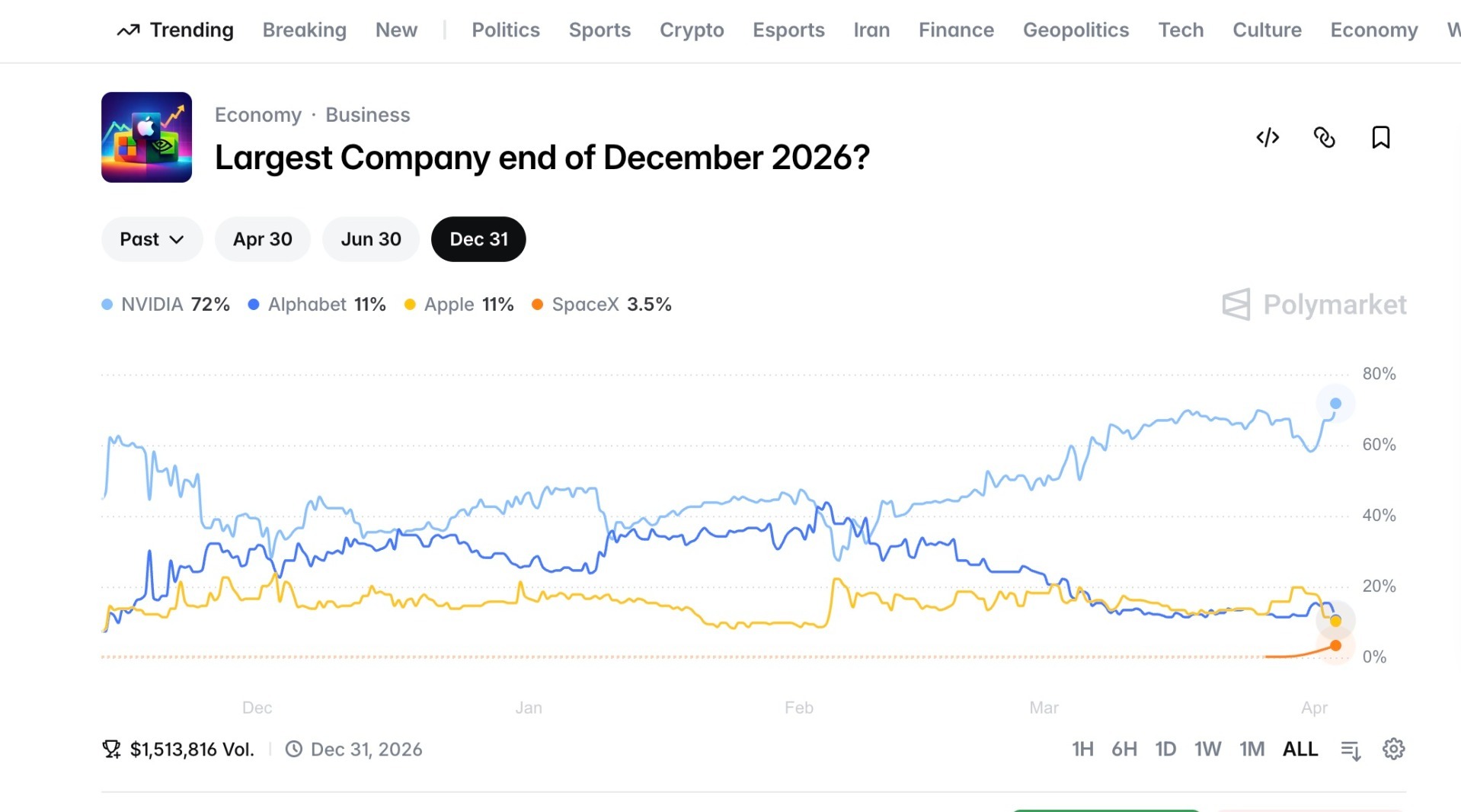

The product is a bond-like note that pays a 7% coupon depending on whether Nvidia Corp. remains the world’s largest company in a year. Instead of taking a direct binary position, investors receive a conditional payout, while their principal is protected, subject to Marex’s credit risk.

How the Structure Works

The note converts a binary outcome into a structured payoff. Rather than placing a direct trade on a prediction market, the investor receives a fixed coupon if the condition is met.

This allows exposure to the same underlying event in a format more familiar to institutional investors. The issuance, with a size of up to $10 million and sold to a Swiss client, serves as an early example of how such products can be structured.

“Marex is going to effectively build our own prediction market structured products, and then leverage Kalshi and other exchanges to replicate that,” said Nilesh Jethwa, CEO of Marex Solutions.

- Oil Traders Turn to Prediction Markets for Signals, Raising Integrity Concerns

- Match-Trader Enters Prediction Markets With White-Label Offering for Brokers

- Senator Warren Leads Push to Tighten Insider Trading Enforcement in Prediction Markets

Hedging Through Prediction Markets

The structure relies on prediction markets for risk management. Marex hedges its exposure by taking positions in underlying event contracts on platforms such as Kalshi, allowing it to offset the payout risk embedded in the note.

As a structured product provider, Marex does not retain directional exposure. Instead, it aims to capture the spread between the coupon offered to investors and the cost of hedging.

This approach depends on the availability and liquidity of prediction markets. Activity is often concentrated in a limited number of contracts, which can affect pricing and hedging efficiency. In less liquid markets, the cost of hedging may increase or become less reliable.

Related Developments

Other market participants have pointed to similar use cases. Structured products linked to event outcomes could be used to hedge tail risks or express views on specific scenarios.

Parallel efforts are also emerging. Roundhill Investments has filed with the SEC to launch ETFs tied to election outcomes, while Marex has indicated it may provide swaps on similar event-driven exposures

What It Means for the Market

For brokers and structured product providers, the Marex note shows how prediction market outcomes can be incorporated into existing financial products.

It introduces a way to translate event-based risk into structured payoffs that fit within established investment frameworks. At the same time, its broader adoption will depend on market depth, regulatory clarity, and the ability to manage hedging risk in practice.