The Chicago Mercantile Exchange filed its annual report to the Securities and Exchange Commission today. Average Daily Volume of FX contracts was 886,000 in 2013 at the CME, up 4.9% thanks to Yen and GBP.

The Chicago Mercantile Exchange has filed its annual report to the SEC today, containing some key currency trading metrics and shedding light on its evaluation of the markets and regulations.

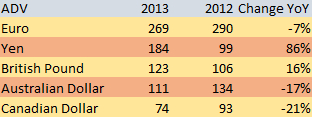

In 2013, the estimated percentage of clearing and transaction fees revenue contributed by foreign exchange trading was 8% of the total revenues of all the CME's products, up from 7% in the previous two years. Average Daily Volume of foreign exchange contracts was 886,000 in 2013, up 4.9% from 2012.

As a result of a decrease in demand for commodity resources in China because of an economic slowdown in the Chinese market, demand decreased for currencies from countries that heavily depend on raw material exports, such as the Australian and Canadian dollars.

Over-the-Counter (OTC) Clearing

Writing about the effort to globalize its business, the CME report mentions that the group applied for regulatory approval to create CME Europe Limited, a London-based FCA supervised derivatives exchange. Pending approval, product offerings will range across multiple-asset classes beginning with foreign exchange.

Regarding the US market, the CME will continue to focus on new customer onboarding for swaps clearing services, expanding OTC product offerings and working with the buy and sell-sides. In 2013, three phases of the clearing mandate of the Dodd-Frank Wall Street Reform Act were implemented in the United States. During the year, the CME cleared OTC transactions worth more than $15.3 trillion, and open interest as of December 31, 2013 was $9.1 trillion.

Despite all of the above, the CME report states that "There is no guarantee that our OTC initiatives will be successful." As the regulatory environment for trading and clearing remains uncertain the group cannot be certain that it will be able to operate profitably under the new legislation.

The example given in the report, provisions within Dodd-Frank include changes to the CFTC's core principles, which could require modifications to the way certain contracts trade or require that such products be de-listed as futures and re-listed as swaps. Also, numerous capital changes and provisions in Basel III may result in uncleared, bilateral OTC derivatives being less expensive than cleared derivatives.

In addition, a number of market participants and exchanges have developed competing platforms and products, including new swap execution facilities. The group concludes that it cannot be certain it will be able to compete effectively or that its initiatives will be successful.

The Chicago Mercantile Exchange has filed its annual report to the SEC today, containing some key currency trading metrics and shedding light on its evaluation of the markets and regulations.

In 2013, the estimated percentage of clearing and transaction fees revenue contributed by foreign exchange trading was 8% of the total revenues of all the CME's products, up from 7% in the previous two years. Average Daily Volume of foreign exchange contracts was 886,000 in 2013, up 4.9% from 2012.

As a result of a decrease in demand for commodity resources in China because of an economic slowdown in the Chinese market, demand decreased for currencies from countries that heavily depend on raw material exports, such as the Australian and Canadian dollars.

Over-the-Counter (OTC) Clearing

Writing about the effort to globalize its business, the CME report mentions that the group applied for regulatory approval to create CME Europe Limited, a London-based FCA supervised derivatives exchange. Pending approval, product offerings will range across multiple-asset classes beginning with foreign exchange.

Regarding the US market, the CME will continue to focus on new customer onboarding for swaps clearing services, expanding OTC product offerings and working with the buy and sell-sides. In 2013, three phases of the clearing mandate of the Dodd-Frank Wall Street Reform Act were implemented in the United States. During the year, the CME cleared OTC transactions worth more than $15.3 trillion, and open interest as of December 31, 2013 was $9.1 trillion.

Despite all of the above, the CME report states that "There is no guarantee that our OTC initiatives will be successful." As the regulatory environment for trading and clearing remains uncertain the group cannot be certain that it will be able to operate profitably under the new legislation.

The example given in the report, provisions within Dodd-Frank include changes to the CFTC's core principles, which could require modifications to the way certain contracts trade or require that such products be de-listed as futures and re-listed as swaps. Also, numerous capital changes and provisions in Basel III may result in uncleared, bilateral OTC derivatives being less expensive than cleared derivatives.

In addition, a number of market participants and exchanges have developed competing platforms and products, including new swap execution facilities. The group concludes that it cannot be certain it will be able to compete effectively or that its initiatives will be successful.

Opetek Launches ARIUS, Pilots AI Reasoning Platform at Tier 1 Investment Bank

Featured Videos

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.