According to minutes from the December meeting, the board of the bank appears to have gone through an intense debating session over bank policy.

(Photo: Bloomberg)

The bank's minutes shed light on the board split over the December measures

The minutes of the December policy formulated by the Bank of Japan were released on Wednesday. They helped to shed additional light on the internal split over the supplementary measures that were decided at that meeting. However, the skeptics warned about possible drawbacks.

At the December 17-18 meeting, the policy board of the central bank voted 6-3 to enable them to undertake a series of steps aimed at supplementing the massive asset purchase program. The board included an extension of average maturities of the bonds of the Japanese government being bought by the bank for 7-12 years. An extension of the Exchange -traded stock funds purchases of the Bank of Japan by Y300 billion per annum.

Some of the board members indicated that measures were required to smooth the asset purchases and dispel fears concerning the sustainability of purchase programs. The minutes indicated that such steps would empower the BOJ to undertake measures of additional easing in a fairly timely manner should that become necessary.

However, one member disagreed, indicating that such a move would cause a misunderstanding among the market participants as the asset purchase program nears its limit.

The central bank avoids identifying board members by name in the minutes customarily.

Since the Halloween easing that took place in October 2014 when Governor Haruhiko Kuroda scraped by with a 5-4 thin margin, the board of the bank has become sharply divided. Shinzo Abe, the Japanese Prime Minister, has tried to tip the balance of a section of the board in favor of the policies formulated by Mr. Kuroda to replace two of the retired board members with those who vehemently support aggressive easing.

The board of the bank appears to have gone through an intense debating session over details of supplementary measures. The majority of the members indicated that the maturity extension of debt purchases was quite necessary for ensuring smooth and flexible conduct of the JGB buying. A few of the members indicated that the bank could manage purchases without making the change.

Some of the members spurned the idea of creating an ETF purchase framework worth Y300 billion in addition to the major ETF buying scheme of Y3 trillion. This was designed to support the companies that were eager to invest and raise employee wages. One member indicated that the BOJ should avoid engaging in measures with features like those of industrial policies as the major characteristic.

At the most recent policy meeting that was held last week, the board of the central bank undertook a clear-cut measure of easing by setting the key interest rate below the zero mark to spur borrowing and lending. Beginning at the middle of this month, the Bank of Japan is expected to impose a negative 0.1% interest rate on a section of yen deposits that are parked by commercial banks at the central bank.

According to Richard Koo, negative rates are an act of desperation that are born out of despair

The negative interest rate policy formulated by the Bank of Japan will not solve the problems of Japan.

The Nomura Research Institute’s chief economist, Richard Koo, says that adoption of negative interest rates by the BOJ is a sign of despair because of the inability of inflation and quantitative easing measures to produce desired results. Lowering the bank’s interest rates is expected to have little effect in the country because many Japanese companies are trying to minimize the level of debt despite them having great balance sheets as a result of dearth of the domestic investment opportunities and debt trauma.

Mr. Koo also points out the fact that the private sector has managed to save a GDP net of 6.7% in 12 months through 2015’s third quarter despite the zero interest rates. Mr. Koo adds that major incentives for driving capital investment will be required to encourage the companies to spend again.

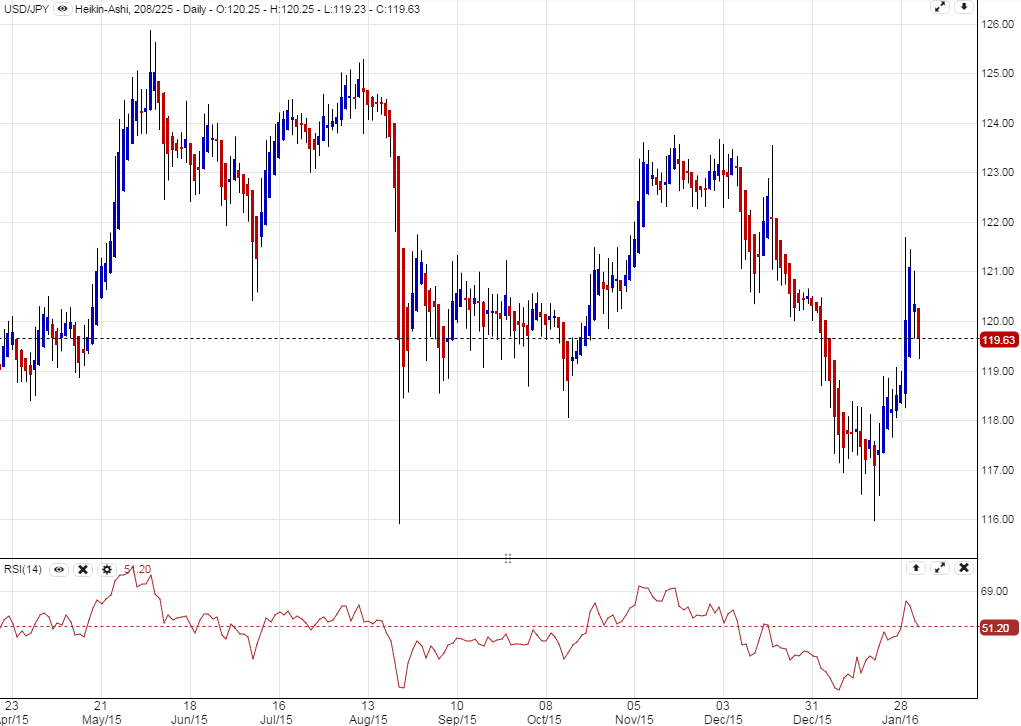

The USD/JPY shows a muted reaction

The USD/JPY is currently showing a somewhat muted reaction to the speech made by Governor Haruhiko Kuroda of the Bank of Japan.

Before the event, the currency was 119.66 but it has since dropped to 119.62. On Friday, the BOJ decided to adopt a negative interest rate to push the reserve rate into the negative territory. The steps taken by the BOJ appear helpless due to pressure from the Chinese economy’s slowdown and the tumble of commodity prices.

Mizuho Bank’s chief economist, Daisuke Karakama, said that they don’t want to welcome extra easing as had been previously experienced in October 2014. This was attributed to the confusion of using negative rates on a section of the yen deposits of commercial banks to the central bank.

The bank's minutes shed light on the board split over the December measures

The minutes of the December policy formulated by the Bank of Japan were released on Wednesday. They helped to shed additional light on the internal split over the supplementary measures that were decided at that meeting. However, the skeptics warned about possible drawbacks.

At the December 17-18 meeting, the policy board of the central bank voted 6-3 to enable them to undertake a series of steps aimed at supplementing the massive asset purchase program. The board included an extension of average maturities of the bonds of the Japanese government being bought by the bank for 7-12 years. An extension of the Exchange -traded stock funds purchases of the Bank of Japan by Y300 billion per annum.

Some of the board members indicated that measures were required to smooth the asset purchases and dispel fears concerning the sustainability of purchase programs. The minutes indicated that such steps would empower the BOJ to undertake measures of additional easing in a fairly timely manner should that become necessary.

However, one member disagreed, indicating that such a move would cause a misunderstanding among the market participants as the asset purchase program nears its limit.

The central bank avoids identifying board members by name in the minutes customarily.

Since the Halloween easing that took place in October 2014 when Governor Haruhiko Kuroda scraped by with a 5-4 thin margin, the board of the bank has become sharply divided. Shinzo Abe, the Japanese Prime Minister, has tried to tip the balance of a section of the board in favor of the policies formulated by Mr. Kuroda to replace two of the retired board members with those who vehemently support aggressive easing.

The board of the bank appears to have gone through an intense debating session over details of supplementary measures. The majority of the members indicated that the maturity extension of debt purchases was quite necessary for ensuring smooth and flexible conduct of the JGB buying. A few of the members indicated that the bank could manage purchases without making the change.

Some of the members spurned the idea of creating an ETF purchase framework worth Y300 billion in addition to the major ETF buying scheme of Y3 trillion. This was designed to support the companies that were eager to invest and raise employee wages. One member indicated that the BOJ should avoid engaging in measures with features like those of industrial policies as the major characteristic.

At the most recent policy meeting that was held last week, the board of the central bank undertook a clear-cut measure of easing by setting the key interest rate below the zero mark to spur borrowing and lending. Beginning at the middle of this month, the Bank of Japan is expected to impose a negative 0.1% interest rate on a section of yen deposits that are parked by commercial banks at the central bank.

According to Richard Koo, negative rates are an act of desperation that are born out of despair

The negative interest rate policy formulated by the Bank of Japan will not solve the problems of Japan.

The Nomura Research Institute’s chief economist, Richard Koo, says that adoption of negative interest rates by the BOJ is a sign of despair because of the inability of inflation and quantitative easing measures to produce desired results. Lowering the bank’s interest rates is expected to have little effect in the country because many Japanese companies are trying to minimize the level of debt despite them having great balance sheets as a result of dearth of the domestic investment opportunities and debt trauma.

Mr. Koo also points out the fact that the private sector has managed to save a GDP net of 6.7% in 12 months through 2015’s third quarter despite the zero interest rates. Mr. Koo adds that major incentives for driving capital investment will be required to encourage the companies to spend again.

The USD/JPY shows a muted reaction

The USD/JPY is currently showing a somewhat muted reaction to the speech made by Governor Haruhiko Kuroda of the Bank of Japan.

Before the event, the currency was 119.66 but it has since dropped to 119.62. On Friday, the BOJ decided to adopt a negative interest rate to push the reserve rate into the negative territory. The steps taken by the BOJ appear helpless due to pressure from the Chinese economy’s slowdown and the tumble of commodity prices.

Mizuho Bank’s chief economist, Daisuke Karakama, said that they don’t want to welcome extra easing as had been previously experienced in October 2014. This was attributed to the confusion of using negative rates on a section of the yen deposits of commercial banks to the central bank.

Cyprus Diaspora Forum and REALTYon Launch Strategic Collaboration to Connect Global Investors with Cyprus Real Estate Opportunities

CMC Markets’ Artur Delijergijevs on Metals Demand, Volatility, & Stable Execution

CMC Markets’ Artur Delijergijevs on Metals Demand, Volatility, & Stable Execution

In this exclusive Executive Interview, Finance Magnates speaks with Artur Delijergijevs, Head of Systematic Market Making at CMC Markets, about the current state of metals demand and market volatility.

Delijergijevs offers a desk-level view on:

- Metals Demand: Why metals are seeing the strongest demand from both retail and institutional clients right now.

- The Safe-Haven Debate: Questioning whether gold still fits the classic safe-haven definition given large daily price movements.

- Volatile Market Prep: How a market-making desk prepares its systems and pricing for stressed market conditions and high-impact economic events.

- Hybrid Execution: Why the best execution model combines electronic speed with human relationship support, especially during volatility.

- AI in Workflow: Where CMC Markets is integrating machine learning for risk management and pricing, and the limitations of AI during stressed markets.

- Dubai's Role: The strategic importance of Dubai’s location for covering global trading sessions across Asia, Europe, and the US.

Watch to understand how CMC Markets maintains stable pricing and reliable execution quality in high-volatility environments.

#CMCmarkets #forex #metals #gold #trading #volatility #MarketMaking #iFXDubai #FinanceMagnates #Finance #Fintech #Execution #AlgorithmicTrading #RiskManagement

In this exclusive Executive Interview, Finance Magnates speaks with Artur Delijergijevs, Head of Systematic Market Making at CMC Markets, about the current state of metals demand and market volatility.

Delijergijevs offers a desk-level view on:

- Metals Demand: Why metals are seeing the strongest demand from both retail and institutional clients right now.

- The Safe-Haven Debate: Questioning whether gold still fits the classic safe-haven definition given large daily price movements.

- Volatile Market Prep: How a market-making desk prepares its systems and pricing for stressed market conditions and high-impact economic events.

- Hybrid Execution: Why the best execution model combines electronic speed with human relationship support, especially during volatility.

- AI in Workflow: Where CMC Markets is integrating machine learning for risk management and pricing, and the limitations of AI during stressed markets.

- Dubai's Role: The strategic importance of Dubai’s location for covering global trading sessions across Asia, Europe, and the US.

Watch to understand how CMC Markets maintains stable pricing and reliable execution quality in high-volatility environments.

#CMCmarkets #forex #metals #gold #trading #volatility #MarketMaking #iFXDubai #FinanceMagnates #Finance #Fintech #Execution #AlgorithmicTrading #RiskManagement

Finance Magnates Awards 2026 – Nominations Now Open

Finance Magnates Awards 2026 – Nominations Now Open

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech